To get out of debt with a low income, create a budget, cut expenses, increase income, and consider debt consolidation or negotiation. Debt can cause huge financial stress, especially when you have a low income.

However, there are practical steps you can take to regain control of your finances and work towards becoming debt-free. By implementing a few key strategies, such as creating a budget, cutting unnecessary expenses, boosting your income, and exploring options like debt consolidation or negotiation, you can start making significant progress in your journey towards becoming debt-free.

We will explore effective approaches and actionable tips that will help you escape the debt trap and bring lasting financial stability into your life. Let’s dive in and discover how to get out of debt with a low income.

Credit: sylvesterknox.medium.com

Setting A Budget

Setting a budget is a crucial step in getting out of debt, especially when you have a low income. It allows you to take control of your finances, track your expenses, and prioritize your spending. By following these steps, you can create a budget that is tailored to your income and helps you work towards a debt-free future.

Tracking Expenses

One of the first things you should do when setting a budget is to track your expenses. This will give you a clear picture of where your money is going and help you identify areas where you can cut back. Start by collecting your receipts, bank statements, and credit card statements for the past few months. Categorize your expenses into different categories like rent/mortgage, utilities, groceries, transportation, and entertainment. You can use a spreadsheet or a budgeting app to keep track of your expenses. This will allow you to see how much you are spending in each category and identify any areas where you may be overspending.

Identifying Priorities

Once you have a clear understanding of your expenses, the next step is to identify your priorities. Determine which expenses are essential and which ones you can cut back on. For example, your rent or mortgage payment and utilities are essential expenses that you cannot eliminate. However, you may be able to reduce your grocery bill by buying generic brands or shopping for sale items. Look for areas where you can make small changes that will add up over time. It’s important to prioritize your debt repayment in your budget. Allocate a portion of your income towards paying off your debts, even if it means making sacrifices in other areas. By prioritizing your debts, you can start chipping away at them and work towards becoming debt-free.

Credit: www.ramseysolutions.com

Reducing Monthly Expenses

One of the most effective ways to get out of debt with a low income is by reducing monthly expenses. By cutting unnecessary costs and negotiating bills, you can free up more money to put towards paying off your debts. Let’s explore these strategies in detail.

Cutting Unnecessary Costs

When it comes to cutting unnecessary costs, it’s important to carefully evaluate your monthly expenses and identify areas where you can make adjustments. Here are some practical ways to cut costs:

- Start by creating a budget to track your income and expenses. This will provide you with a clear understanding of where your money is going each month.

- Eliminate or reduce expenses that are not essential. For example, consider canceling unused subscriptions or memberships.

- Shop smart by comparing prices and finding the best deals. Look for sales, discounts, and coupons before making any purchases.

- Save on groceries by planning meals in advance, buying generic brands, and avoiding impulse purchases. Consider buying in bulk for frequently used items.

- Reduce energy costs by turning off lights when not in use, using energy-efficient appliances, and lowering the thermostat.

- Limit eating out and pack your lunch for work or school instead. Cooking at home not only saves money but also allows you to make healthier choices.

- Consider downsizing your living arrangement or finding a roommate to share expenses.

Negotiating Bills

Negotiating bills can yield significant savings and help you allocate more money towards debt repayment. Here are some tips for negotiating bills:

- Contact your service providers such as internet, cable, and phone companies to inquire about any promotions, discounts, or lower-priced plans they may offer.

- Research competitive rates and use that information as leverage during negotiations.

- If you have a good payment history, mention it to your service provider to strengthen your negotiation position.

- Consider bundling services from a single provider to get a discounted rate.

- Be persistent and don’t be afraid to ask for a supervisor or manager if the initial representative is unable to meet your negotiation requests.

Reducing monthly expenses through cutting unnecessary costs and negotiating bills can make a significant difference in your ability to get out of debt, even with a low income. By implementing these strategies, you’ll be able to free up more money to put towards debt repayment and ultimately achieve financial freedom.

Increasing Income

Learn how to increase your income and get out of debt even with a low income. Discover effective strategies to improve your financial situation and start building a better future.

Increasing your income when you have a low income is an essential step to get out of debt. By finding additional sources of income and negotiating a raise, you can begin to generate more money to put towards paying off your debts. Let’s explore these strategies in more detail.Finding Additional Sources Of Income

One effective way to increase your income is to find additional sources of income. This could involve taking on a second job or pursuing freelance work in your spare time. By diversifying your income streams, you can create additional revenue that can be used to pay off your debts more quickly.Negotiating A Raise

Another way to boost your income is by negotiating a raise at your current job. Start by researching the average salaries for your position in your industry. Then, gather evidence of your value to the company, such as successful projects or positive feedback from clients or colleagues. Present this information to your employer during a performance review or one-on-one meeting, and confidently express your desire for a raise. Remember to focus on your accomplishments and the value you bring to the company, rather than solely emphasizing your financial needs. By increasing your income through finding additional sources of income and negotiating a raise, you can take significant strides towards getting out of debt with a low income. Remember, the key is to be proactive and persistent in your efforts to generate more money. Stay focused on your goal of becoming debt-free, and the additional income you generate can become a powerful tool in achieving financial freedom.

Credit: www.bankrate.com

Managing Debt

If you’re struggling with debt on a low income, there are strategies you can implement to get back on track. Explore options like budgeting, negotiating with creditors, and seeking financial assistance to effectively manage your debt and improve your financial situation.

Consolidating Loans

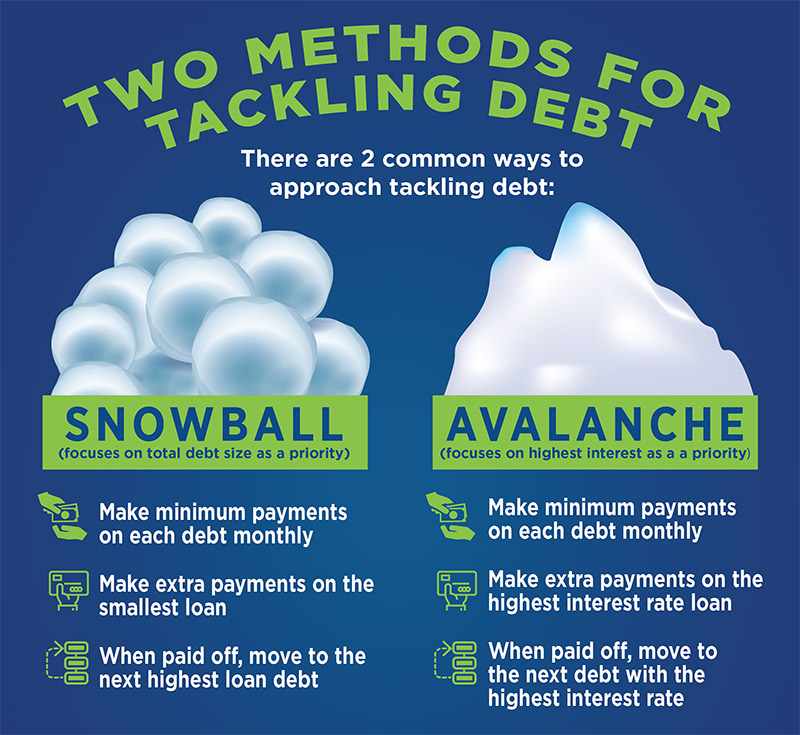

If you’re struggling with debt on a low income, consolidating your loans can be an effective way to manage and reduce your debt. Consolidation involves combining multiple loans into one, typically with a lower interest rate. This not only simplifies your monthly payments but also helps you save money in the long run. Instead of juggling different due dates and interest rates, you’ll have a single payment to focus on. Here are a few options to consider: 1. Balance Transfer Credit Cards: Look for credit cards that offer a low or zero percent introductory APR on balance transfers. Transferring high-interest debt to a card with a lower rate can help you pay off your debt faster and save on interest charges. 2. Debt Consolidation Loans: Talk to your bank or credit union about getting a debt consolidation loan. These loans are specifically designed to help you pay off your existing debts and consolidate them into one monthly payment with a fixed interest rate. 3. Home Equity Loans: If you own a home, you may have the option to use a home equity loan to consolidate your debt. This allows you to borrow against the equity you’ve built in your home and use the funds to pay off your debts. However, be cautious as using your home as collateral puts it at risk. 4. Debt Management Plans: Consider enrolling in a debt management plan offered by a reputable credit counseling agency. They will negotiate with your creditors to lower your interest rates and develop a personalized repayment plan. Through consolidation, you can simplify your debt repayment, save on interest, and ultimately work towards becoming debt-free.Negotiating With Creditors

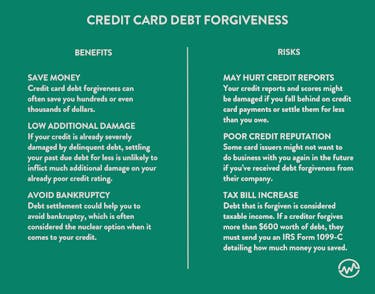

When dealing with debt on a low income, negotiating with creditors can be a valuable strategy. Creditors often understand the challenges faced by individuals with limited financial resources and may be willing to work with you. Here are some steps to take when negotiating with creditors: 1. Contact Your Creditors: Reach out to your creditors directly and explain your situation. Be honest about your financial struggles and emphasize your commitment to repaying your debts. By initiating the conversation, you show your willingness to find a solution and demonstrate responsibility. 2. Propose a Repayment Plan: Create a realistic budget that outlines how much you can afford to pay each month. Present this plan to your creditors and explain how it aligns with your financial situation. By offering a specific repayment proposal, you present yourself as proactive and committed to resolving your debts. 3. Ask for Lower Interest Rates: High-interest rates can significantly increase your debt burden. Politely ask your creditors if they would consider lowering the interest rates on your debts. Highlight any positive changes in your financial circumstances or any hardship you may be experiencing. Lower rates can help you repay your debts faster and more affordably. 4. Consider Settlement Offers: In some cases, creditors may be open to accepting a lump-sum payment that is less than the total amount owed. This is known as a debt settlement. If you have a significant amount of debt and are unable to pay it off in full, negotiating a settlement may provide some relief. However, be aware that this can have long-term consequences and should be carefully considered. Remember, communication is key when negotiating with creditors. Be respectful, honest, and persistent in your efforts to find a workable solution. By taking the initiative to address your debts head-on, you can pave the way to a debt-free future.Frequently Asked Questions Of How To Get Out Of Debt With A Low Income

What Can I Do If I Can’t Afford To Pay My Debts?

If you can’t afford to pay your debts, there are a few options you can consider. You can contact your creditors to negotiate a payment plan or to lower interest rates. Also, consider seeking assistance from credit counseling agencies or exploring debt consolidation loans.

How Do You Get Out Of Debt On A Low Budget?

To get out of debt on a low budget, you can prioritize essential expenses, cut back on non-essential items, and create a realistic budget. Look for ways to increase income and consider debt consolidation or negotiation with creditors. Seek financial assistance and explore financial education resources to help you manage your finances effectively.

How Can I Get Out Of Debt With Low Income And Bad Credit?

To get out of debt with low income and bad credit, consider budgeting, trimming expenses, increasing income, and seeking professional help. Cut unnecessary spending, find ways to earn extra money, and explore debt relief options such as debt consolidation or negotiating with creditors.

Seek guidance from credit counseling agencies for personalized solutions.

How Do I Get Out Of Debt When I Live Paycheck To Paycheck?

To break free from debt while living paycheck to paycheck: 1. Create a budget and track all expenses. 2. Cut unnecessary spending and look for ways to save money. 3. Increase income through additional part-time work or freelancing. 4. Prioritize debts and make regular payments.

5. Consider debt consolidation or negotiation for lower interest rates.

Conclusion

Overcoming debt with a low income requires dedication, discipline, and smart financial strategies. By creating a budget, reducing expenses, and increasing income through side hustles or freelancing, it is possible to regain control of your finances. Additionally, seeking professional advice from credit counselors or financial coaches can provide valuable guidance and support throughout your journey to financial freedom.

Remember, small steps can lead to big results in the long run. So, stay committed and persistent, and eventually, you’ll be able to leave debt behind and enjoy a brighter financial future.

:max_bytes(150000):strip_icc()/Primary-Image-best-debt-consolidation-loans-for-bad-credit-5075582-a8a538cf537f4a67966703ba7d3c18a1.jpg)

:max_bytes(150000):strip_icc()/debt-avalanche-vs-debt-snowball-which-best-you.asp_v1-b62b7fef4c6949aa96550aa2c33b391e.png)