In a landmark move to revolutionize cross-border trade, the Bangladesh Bank (BB) has introduced a new Business-to-Business-to-Consumer (B2B2C) framework to significantly boost online exports. This major policy step, announced via a foreign exchange circular on November 24, 2025, represents the first time online exports have been formally allowed through this structure.

The initiative is designed to expand the country’s export channels and integrate Bangladeshi products more effectively into the global digital retail chain, aligning regulations with practices widely used in global e-commerce supply chains.

Understanding the B2B2C Framework

Under this new policy, Bangladeshi products can now be sold directly to global buyers (the ‘Consumer’) through reputable international online platforms and marketplaces. This model officially allows shipments under the B2B2C structure.

Crucially, the export process involves an intermediary (the ‘Business’). Exports are completed through entities such as international e-commerce platforms, third-party warehouses, logistics providers, or fulfillment centers, rather than shipping directly to the final customer. This enables Bangladeshi exporters to sell through globally recognized platforms like Amazon, eBay, Walmart, Alibaba, and Etsy.

For instance, a Bangladeshi leather goods manufacturer can ship a batch of handbags to an Amazon FBA (Fulfilment by Amazon) warehouse in the United States. In this scenario, Amazon acts as the consignee, even though it is not the final purchaser of the goods.

Major Procedural Breakthroughs for Exporters

The central bank’s policy relaxation has addressed several long-standing obstacles that previously hindered small and medium-sized businesses (SMEs) from entering global digital retail.

Simplified Documentation

The B2B2C framework often lacks traditional sales contracts between the exporter and the consignee/intermediary. The new rules accommodate this global practice through key changes:

Proof of Registration: To execute exports under this framework, exporters must provide the Authorized Dealer (AD) bank with documented proof of their registration with the recognized international online platform or overseas warehouse.

Proforma Invoices: Exporters can now declare the consignment value based on a proforma invoice, eliminating the necessity of a conventional sales contract.

Consignee Acceptance: AD banks are now authorized to accept shipping documents prepared in the name of the intermediary providing the warehousing or facilitating services.

Flexible Payment Realization and Reconciliation

The policy also streamlines the realization of export proceeds, which is often complex in platform-based sales:

Payment Channels: Export proceeds can be repatriated through normal banking channels, including payments routed via legitimate international payment service operators.

Relaxed Matching: Since export receipts under platform sales often cover multiple shipments and correspond to multiple invoices, the central bank has relaxed the requirement for one-to-one payment matching.

FIFO Settlement: Dealer banks can now reconcile these pooled receipts using the First-in, First-out (FIFO) method, meaning earlier shipments will be settled first. Furthermore, ADs may permit the realization of proceeds that exceed the declared value, provided due diligence and appropriate documentation are supplied.

A Game-Changer for SMEs and Diversification

Industry stakeholders have overwhelmingly welcomed this reform, calling it a “game-changer for Bangladesh’s cross-border e-commerce”. The new framework is expected to deliver substantial benefits to the national economy and small businesses:

Formalization: The official channel will formalize hundreds of millions of dollars in online exports that were previously shipped through informal routes, personal accounts, or third-party methods because banks couldn’t process the documentation properly.

Wider Market Access: The policy lowers entry barriers for SMEs and individual entrepreneurs, providing wider market access and opening new markets. Now, businesses can operate like exporters from countries such as China, Vietnam, or India.

Diversified Growth: This framework is expected to accelerate diversified export growth and supports the export of new product categories, including light consumer goods, lifestyle items, crafts, and niche products.

Global Visibility: By strengthening Bangladesh’s footprint in the international online marketplace, the policy is expected to increase the country’s visibility on global e-commerce platforms.

By embracing the B2B2C model, the policy is set to unlock an important new export stream, helping to diversify earnings beyond the traditional garment sector as digital commerce continues its worldwide expansion.

Think of the B2B2C policy like building a dedicated, official express lane onto the global digital highway. Previously, small exporters were forced to use informal side roads or confusing documentation paths because their destination (the consumer) was different from their drop-off point (the warehouse). Now, the BB has officially recognized the drop-off point as a legitimate stop, creating a fast, formal, and organized route for goods to reach millions of international customers.

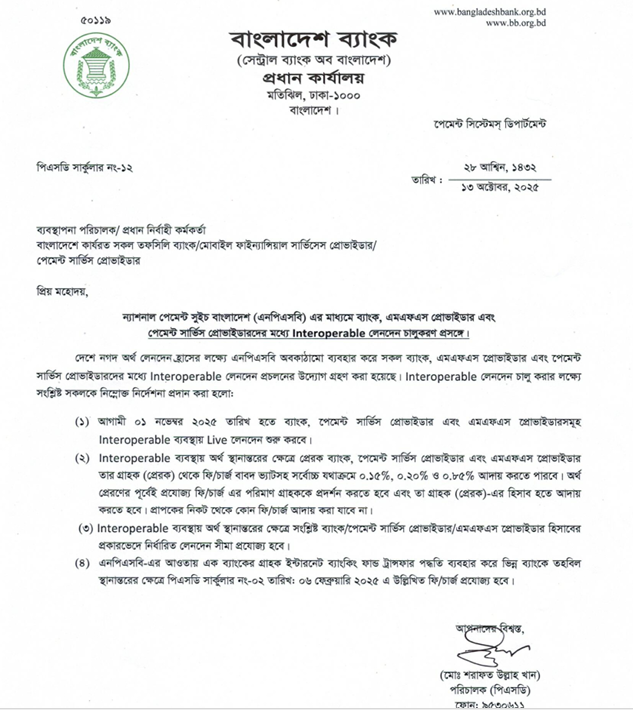

১৩/১০/২০২৫ তারিখে পিএসডি সার্কুলার নং-১২ এর মাধ্যমে আগামী ০১ নভেম্বর ২০২৫ তারিখ হতে ন্যাশনাল পেমেন্ট সুইচ বাংলাদেশ (এনপিএসবি) এর মাধ্যমে ব্যাংক, এমএফএস প্রোভাইডার এবং পেমেন্ট সার্ভিস প্রোভাইডারদের মধ্য interoperable লেনদেন চালু করতে যাচ্ছে বাংলাদেশ ব্যাংক। এতে গ্রাহকের খরচ কমবে এবং সহজে সেবা পাওয়া সম্ভব হবে।

বছরের পর বছর ধরে বিকাশ থেকে ব্যাংক অ্যাকাউন্টে, কিংবা এক মোবাইল ওয়ালেট থেকে অন্যটিতে টাকা পাঠানোটা যেন সুরক্ষিত সীমান্ত পার হওয়ার মতো ছিল। কিন্তু আগামী ১ নভেম্বর, ২০২৫ থেকে সেই অদৃশ্য সীমান্তগুলো উঠে যাচ্ছে। বাংলাদেশ ব্যাংক একটি নতুন আন্তঃলেনদেন (interoperable) ব্যবস্থা চালু করতে যাচ্ছে, যা নিয়ে অনেকের মনেই খরচসহ নানা বিষয়ে প্রশ্ন তৈরি হয়েছে। এই আর্টিকেলে আমরা নতুন এই সিস্টেমের সবচেয়ে গুরুত্বপূর্ণ এবং চমকপ্রদ দিকগুলো সহজ ভাষায় তুলে ধরব।

আন্ত:লেনদেন ব্যবস্থা

আগামী ১ নভেম্বর, ২০২৫ থেকে বাংলাদেশ ব্যাংক একটি নতুন ডিজিটাল লেনদেন ব্যবস্থা চালু করতে যাচ্ছে, যার মূল উদ্দেশ্য হলো দেশের বিভিন্ন ব্যাংক, মোবাইল ফিন্যান্সিয়াল সার্ভিস (এমএফএস) এবং পেমেন্ট সার্ভিস প্রোভাইডারদের (পিএসপি) মধ্যে টাকা পাঠানোকে আরও সহজ করা এবং গ্রাহকদের জন্য খরচ কমিয়ে আনা।

এই ব্যবস্থাটি ভালোভাবে বুঝতে হলে, চলুন প্রথমে কিছু জরুরি শব্দ ও তাদের অর্থ জেনে নিই।

কিছু গুরুত্বপূর্ণ শব্দের সংজ্ঞা

• এমএফএস (MFS): এমএফএস (MFS) হলো মোবাইলের একটি ডিজিটাল ওয়ালেট সেবা, যেখানে এজেন্ট পয়েন্ট থেকে টাকা জমা বা তোলা যায়। যেমন, আমরা সবাই বিকাশ, রকেট বা নগদ ব্যবহার করি।

• পিএসপি (PSP): পিএসপি (PSP) অনেকটা MFS-এর মতোই একটি ডিজিটাল ওয়ালেট, কিন্তু এর কোনো এজেন্ট পয়েন্ট থাকে না। পাঠাও পে বা টালি পে হলো এর উদাহরণ।

• এনপিএসবি (NPSB): এনপিএসবি (NPSB) হলো বাংলাদেশ ব্যাংকের একটি কেন্দ্রীয় প্ল্যাটফর্ম, যা দেশের সব ব্যাংক, MFS এবং PSP-কে একসাথে যুক্ত করে দেয়, যাতে আমরা মুহূর্তের মধ্যে নিজেদের মধ্যে টাকা লেনদেন করতে পারি।

• Cost of Fund: বলতে এসকল আর্থিক প্রতিষ্ঠান কর্তৃক ফান্ড সংগ্রহের গড় খরচ বা ব্যয়কে বোঝায়। উদাহরণস্বরূপ এমএফএস এর ক্ষেত্রে cost of fund হলো নগদ অর্থ মোবাইল ওয়ালেটে ই-মানি হিসাবে ডিজিটাইজ করা সংশ্লিষ্ট ব্যয়। এক্ষেত্রে এজেন্ট ও ডিস্ট্রিবিউটর কমিশন, USSD/এ্যাপ ও SMS খরচ, ভ্যাট ও প্রমোশনাল ব্যয় ইত্যাদি অন্তর্ভুক্ত। উল্লেখ্য যে, এমএফএসসমূহ এ ব্যয় cash in এর সময় না কর্তন করে, একেবারে cash out এর সময় কর্তন করে।

এখন যেহেতু আমরা এই প্রতিষ্ঠানগুলোকে চিনি, চলুন দেখে নেওয়া যাক এদের মধ্যে টাকা লেনদেনের নতুন খরচ কেমন হবে।

নতুন নিয়মে টাকা পাঠানোর খরচ কেমন হবে?

এই ব্যবস্থার সবচেয়ে গুরুত্বপূর্ণ নিয়মটি হলো: যিনি টাকা পাঠাবেন, শুধু তাকেই চার্জ দিতে হবে; যিনি টাকা গ্রহণ করবেন তার কোনো খরচ নেই। টাকা পাঠানোর আগে প্রেরককে অবশ্যই খরচের পরিমাণ দেখানো হবে এবং তার সম্মতিতেই লেনদেন সম্পন্ন হবে।

নিচের টেবিলে নতুন সর্বোচ্চ খরচের তালিকা দেওয়া হলো:

আপনি পাঠাচ্ছেন (Sender)

টাকা যেখানে যাচ্ছে (Receiver)

খরচ (প্রতি হাজারে)

ব্যাংক (Bank)

অন্য যেকোনো MFS বা PSP-তে

১.৫ টাকা

পিএসপি (PSP)

অন্য যেকোনো ব্যাংক, MFS বা PSP-তে

২ টাকা

এমএফএস (MFS)

অন্য যেকোনো ব্যাংক, MFS বা PSP-তে

৮.৫ টাকা

• বিশেষ দ্রষ্টব্য: এক ব্যাংক থেকে অন্য ব্যাংকে টাকা পাঠানোর সর্বোচ্চ খরচ আগের মতোই লেনদেন প্রতি ১০ টাকা থাকবে। অর্থাৎ এক ব্যাংক হতে অন্য ব্যাংকে ১ লক্ষ টাকা প্রেরণ করলে প্রেরকের খরচ সর্বোচ্চ ১০ টাকা।

এই নতুন খরচের তালিকা দেখে আপনার মনে কিছু প্রশ্ন আসতেই পারে, চলুন সেগুলোর উত্তর খোঁজা যাক।

সত্যিই কি ‘অ্যাড মানি’র খরচ বাড়ছে?

অনেকের প্রধান উদ্বেগ হলো, ব্যাংক থেকে মোবাইল ফিন্যান্সিয়াল সার্ভিস (MFS) যেমন বিকাশ বা নগদে টাকা আনার খরচ বা ‘অ্যাড মানি’র খরচ বাড়বে কিনা।

বর্তমানে MFS সমূহ ব্যাংক থেকে এড মানি করার ক্ষেত্রে তিনটি পদ্ধতি ব্যবহৃত হয়:

ক) NPSB প্ল্যাটফর্ম ব্যবহার করে

খ) বিভিন্ন আন্তর্জাতিক প্ল্যাটফর্ম (Visa, Mastercard ইত্যাদি) ব্যবহার করে ক্রেডিট/ডেবিট কার্ড থেকে; এবং

গ) ব্যাংক ও MFS এর নিজস্ব দ্বিপাক্ষিক চুক্তি ও সংযোগ (API Connectivity) এর মাধ্যমে ব্যাংক একাউন্ট থেকে।

বর্তমানে অনেক MFS গ্রাহকদের জন্য ‘অ্যাড মানি’ সেবাটি বিনামূল্যে দিয়ে থাকে। এর কারণ হলো, ব্যাংক ও MFS প্রতিষ্ঠানগুলো নিজেদের মধ্যে দ্বিপাক্ষিক চুক্তির মাধ্যমে এই খরচটি (যা ক্ষেত্রবিশেষে ০.৪% পর্যন্ত হয়) নিজেরাই বহন করে।

বাংলাদেশ ব্যাংকের নতুন সার্কুলার অনুযায়ী, ন্যাশনাল পেমেন্ট সুইচ বাংলাদেশ (NPSB) প্ল্যাটফর্ম ব্যবহার করে ‘অ্যাড মানি’ করলে প্রেরক ব্যাংক গ্রাহকের কাছ থেকে প্রতি হাজারে সর্বোচ্চ ১.৫ টাকা (০.১৫%) ফি নিতে পারবে। তবে স্বস্তির বিষয় হলো, টাকা পাঠানোর আগেই অ্যাপের স্ক্রিনে আপনাকে এই চার্জের পরিমাণ স্পষ্টভাবে দেখানো হবে, ফলে কোনো লুকানো খরচ থাকবে না।

উল্লেখ্য যে ব্যাংকসমূহ তাদের cost of fund এবং ব্যবসায়িক কৌশল বিবেচনায় তাদের গ্রাহকদের ০.১৫% এর কম খরচে এমনকি ০% হারে NPSB ব্যবস্থায় এমএফএস ও পিএসপিসমূহে ফান্ড ট্রান্সফারের সুবিধা প্রদান করতে পারবে। একইভাবে NPSB ব্যবস্থায় এমএফএস ও পিএসপিসমূহের খরচ হ্রাস পাবে বিধায় তাদের গ্রাহকের ওয়ালেটে (প্রাপক) বোনাস প্রদানের মাধ্যমেও উক্ত ফি পুর্নভরণ করতে পারবে। আর্থিক প্রতিষ্ঠানসমূহের cost of fund এবং কারিগরি দক্ষতা প্রতিষ্ঠানভেদে ভিন্ন হওয়ায় বাংলাদেশ ব্যাংক কোন নির্দিষ্ট ফি এর পরিবর্তে সর্বোচ্চ ফি নির্ধারণ করেছে। এতে প্রতিষ্ঠানসমূহ তার ব্যবসায়িক কৌশলের নিরিখে ফি নির্ধারণ করতে পারবে বিধায় আর্থিক প্রতিষ্ঠানসমূহের মধ্যে প্রতিযোগিতা ও গ্রাহক সেবার মান বৃদ্ধি পাবে মর্মে আশা করা যায়।

একই সাথে MFS সমূহ চাইলে NPSB প্ল্যাটফর্ম ব্যবহার না করে আগের মতো নিজস্ব দ্বিপাক্ষিক সংযোগ ও আন্তর্জাতিক প্ল্যাটফর্ম (Visa, Mastercard ইত্যাদি) ব্যবহার করেও গ্রাহকদের এড মানির সেবা প্রদান করতে পারে এবং পূর্বের মতো প্রেরক ব্যাংক বা আন্তর্জাতিক প্ল্যাটফর্মের আরোপিত ফি নিজে বহন করে বিনামূল্যে তার গ্রাহকদের এড মানির সেবা প্রদান করতে পারবে। পাশাপাশি আর্থিক প্রতিষ্ঠানসমূহ দ্রুততম সময়ে তাদের এ্যাপে প্রয়োজনীয় আপগ্রেডেশন করবে যার ফলে গ্রাহকের নিকট NPSB প্ল্যাটফর্মের পাশাপাশি দ্বিপাক্ষিক সংযোগ বা আন্তর্জাতিক প্লাটফর্মের মাধ্যমে অর্থ স্থানান্তরের অপশনও থাকবে এবং গ্রাহক তাঁর পছন্দমতো পদ্ধতি বাছাই করতে পারবে।

কিন্তু এর মানে এই নয় যে ‘অ্যাড মানি’তে খরচ হচ্ছেই। এখানে কয়েকটি গুরুত্বপূর্ণ বিষয় রয়েছে:

১. বিকল্প পথ খোলা: MFS প্রতিষ্ঠানগুলোর জন্য NPSB-ই একমাত্র পথ নয়। তারা আগের মতোই তাদের নিজস্ব দ্বিপাক্ষিক সংযোগ বা ভিসা, মাস্টারকার্ডের মতো আন্তর্জাতিক প্ল্যাটফর্ম ব্যবহার করে গ্রাহকদের বিনামূল্যে ‘অ্যাড মানি’ সেবা দেওয়া অব্যাহত রাখতে পারবে।

২. খরচ কমানোর সুযোগ: MFS প্রতিষ্ঠানগুলো NPSB ব্যবহার করলেও গ্রাহকের খরচ পুষিয়ে দিতে পারবে। যেহেতু এই নতুন ব্যবস্থায় তাদের নিজেদের খরচও কমবে, তাই তারা গ্রাহকের ওয়ালেটে (প্রাপক) বোনাস প্রদানের মাধ্যমে প্রেরকের দেওয়া ফি ফেরত দিতে পারবে। অর্থাৎ, ব্যাংক আপনার কাছ থেকে ১.৫ টাকা নিলেও MFS আপনাকে সমপরিমাণ বোনাস দিয়ে লেনদেনটি কার্যত বিনামূল্যেই করে দিতে পারে।

৩. ব্যাংকের প্রতিযোগিতা: ব্যাংকগুলোকেও সর্বোচ্চ ফি নিতেই হবে এমন কোনো বাধ্যবাধকতা নেই।

উল্লেখ্য যে ব্যাংকসমূহ তাদের cost of fund এবং ব্যবসায়িক কৌশল বিবেচনায় তাদের গ্রাহকদের ০.১৫% এর কম খরচে এমনকি ০% হারে NPSB ব্যবস্থায় এমএফএস ও পিএসপিসমূহে ফান্ড ট্রান্সফারের সুবিধা প্রদান করতে পারবে।

সুতরাং, ‘অ্যাড মানি’র খরচ বাড়বে কিনা, তা নির্ভর করবে ব্যাংক ও MFS প্রতিষ্ঠানগুলোর প্রতিযোগিতামূলক কৌশলের ওপর।

কিছু লেনদেন এখন আগের চেয়ে সস্তা হবে

যদিও ‘অ্যাড মানি’র বিষয়টি বেশ nuanced, নতুন নিয়মে অন্য একটি সাধারণ লেনদেনে দ্ব্যর্থহীনভাবে দারুণ সুখবর রয়েছে। MFS ওয়ালেট (যেমন: বিকাশ, নগদ) থেকে সরাসরি ব্যাংক অ্যাকাউন্টে টাকা পাঠানোর খরচ এখন উল্লেখযোগ্যভাবে কমবে।

বর্তমানে এই ধরনের লেনদেনে প্রতি হাজারে খরচ হয় ১০.৫ টাকা থেকে ১২.৫ টাকা। নতুন নিয়ম কার্যকর হলে এই খরচ কমে প্রতি হাজারে সর্বোচ্চ ৮.৫ টাকায় নেমে আসবে। এই পরিবর্তনটি সরাসরি ফ্রিল্যান্সার, ছোট অনলাইন ব্যবসায়ী এবং এমন প্রত্যেকের জন্য সুবিধাজনক, যারা মোবাইল ওয়ালেটে পেমেন্ট গ্রহণ করেন কিন্তু মূলধন একত্র করার জন্য ব্যাংকে টাকা জমা রাখতে চান।

ভেঙে যাচ্ছে অদৃশ্য দেয়াল

আগে এক আর্থিক প্রতিষ্ঠান থেকে অন্য প্রতিষ্ঠানে টাকা পাঠানোর সুযোগ ছিল সীমিত। কেবল যেসব ব্যাংক, MFS বা PSP-এর মধ্যে সরাসরি “দ্বিপাক্ষিক চুক্তি” ছিল, তাদের গ্রাহকরাই একে অপরের সাথে লেনদেন করতে পারতেন। এর ফলে নতুন বা ছোট প্রতিষ্ঠানগুলোর গ্রাহকরা আন্তঃলেনদেন সুবিধা থেকে বঞ্চিত হতো।

নতুন NPSB সিস্টেমটি অংশগ্রহণকারী সকল ব্যাংক, MFS এবং পেমেন্ট সার্ভিস প্রোভাইডারকে (PSP) একটি অভিন্ন নেটওয়ার্কে যুক্ত করবে। (PSP বা পেমেন্ট সার্ভিস প্রোভাইডার হলো এমন প্রতিষ্ঠান যারা ডিজিটাল ওয়ালেট সেবা দেয়, কিন্তু MFS-এর মতো এজেন্টের মাধ্যমে টাকা তোলা বা জমা দেওয়ার সুবিধা দেয় না। যেমন: পাঠাও পে, টালি পে ইত্যাদি।)

এতে আর্থিক প্রতিষ্ঠানগুলোর মধ্যকার অদৃশ্য দেয়াল ভেঙে যাবে এবং গ্রাহকদের জন্য বিকল্প বাড়বে। এটি বিশেষ করে PSP-গুলোর জন্য বড় সুযোগ তৈরি করবে, যা দেশের ডিজিটাল পেমেন্ট ব্যবস্থা শক্তিশালী করতে এবং “ক্যাশলেস বাংলাদেশ” গঠনে সহায়তা করবে।

‘সর্বোচ্চ ফি’ বেঁধে দেওয়া হলো কেন?

এই নতুন নিয়মে বাংলাদেশ ব্যাংক কোনো নির্দিষ্ট ফি নির্ধারণ না করে একটি ‘সর্বোচ্চ ফি’ বেঁধে দিয়েছে। এর পেছনের মূল যুক্তি হলো প্রতিষ্ঠানগুলোর মধ্যে একটি সুস্থ প্রতিযোগিতা তৈরি করা।

এই ব্যবস্থার ফলে প্রতিটি ব্যাংক, MFS বা PSP তাদের নিজস্ব “cost of fund” (তহবিল সংগ্রহের খরচ) এবং ব্যবসায়িক কৌশল অনুযায়ী গ্রাহকদের জন্য ফি নির্ধারণ করতে পারবে। এখানে “cost of fund” বলতে বোঝায় একটি প্রতিষ্ঠানের তহবিল সংগ্রহের গড় খরচ। যেমন, MFS-এর ক্ষেত্রে এর মধ্যে অন্তর্ভুক্ত থাকে এজেন্ট ও ডিস্ট্রিবিউটর কমিশন, USSD/অ্যাপ ও SMS খরচ, ভ্যাট এবং প্রচারণামূলক ব্যয়।

যেহেতু প্রতিটি প্রতিষ্ঠানের খরচ এবং কারিগরি দক্ষতা ভিন্ন, তাই সর্বোচ্চ ফি নির্ধারণ করে দেওয়ায় তারা নিজেদের মধ্যে প্রতিযোগিতা করে গ্রাহকদের আকৃষ্ট করতে পারবে। আশা করা হচ্ছে, এর ফলে সেবার মান বাড়বে এবং দীর্ঘমেয়াদে গ্রাহকদের জন্য খরচও কমে আসবে।

এই লেনদেনে বাংলাদেশ ব্যাংকের কোনো লাভ নেই

অনেকের মনে প্রশ্ন জাগতে পারে যে, এই লেনদেনের ফি থেকে বাংলাদেশ ব্যাংক বা NPSB প্ল্যাটফর্ম কোনো মুনাফা করছে কি না। এর সরাসরি উত্তর হলো—না। গ্রাহকদের লেনদেন থেকে বাংলাদেশ ব্যাংক কোনো প্রকার চার্জ বা ফি গ্রহণ করছে না। ডিজিটাল লেনদেনকে উৎসাহিত করা এবং জনস্বার্থ নিশ্চিত করাই এই প্ল্যাটফর্মের মূল উদ্দেশ্য।

ডিজিটাল লেনদেনের প্রসার ও জনস্বার্থে NPSB প্ল্যাটফর্ম তথা বাংলাদেশ ব্যাংক আন্তঃলেনদেনে কোনো প্রকার চার্জ/ফি গ্রহণ করছে না।

আপনার জন্য সুবিধাগুলো কী?

1. বেশি স্বাধীনতা: এখন আপনি আপনার ব্যাংক অ্যাকাউন্ট বা এমএফএস ওয়ালেট থেকে দেশের প্রায় যেকোনো আর্থিক প্রতিষ্ঠানের অ্যাকাউন্টে সহজেই টাকা পাঠাতে পারবেন, তা যে কোম্পানিরই হোক না কেন।

2. স্বচ্ছ খরচ: টাকা পাঠানোর আগেই আপনি পরিষ্কারভাবে জানতে পারবেন কত টাকা খরচ হচ্ছে। এছাড়া, এমএফএস থেকে ব্যাংকে টাকা পাঠানোর মতো কিছু ক্ষেত্রে খরচ আগের চেয়ে কমে আসবে।

3. সহজ লেনদেন: সব আর্থিক সেবা একটি প্ল্যাটফর্মে যুক্ত হওয়ায় আপনার টাকা ব্যবস্থাপনা অনেক সহজ হবে। যেমন, আপনার রকেট অ্যাকাউন্ট থেকে সরাসরি বন্ধুর পাঠাও পে ওয়ালেটে টাকা পাঠানো যাবে, যা আগে সম্ভব ছিল না।

উপসংহার

শেষ পর্যন্ত, এটি কেবল একটি নীতিমালা পরিবর্তন নয়; এটি বাংলাদেশে পরবর্তী প্রজন্মের আর্থিক পণ্য তৈরির ভিত্তি স্থাপন। প্রতিষ্ঠানগুলোর মধ্যেকার দরজা জোর করে খুলে দিয়ে বাংলাদেশ ব্যাংক এমন সব উদ্ভাবনী ফিনটেক সমাধানের পথ তৈরি করছে, যা আমরা হয়তো এখনো কল্পনাও করতে পারছি না। এই উদ্যোগ বাংলাদেশের ডিজিটাল আর্থিক ব্যবস্থাকে আরও উন্মুক্ত, প্রতিযোগিতামূলক এবং পরস্পরের সাথে সংযুক্ত করবে।

এই নতুন আন্তঃলেনদেন ব্যবস্থা আপনার দৈনন্দিন টাকা পয়সার ব্যবস্থাপনায় কী পরিবর্তন আনবে বলে আপনি মনে করেন?

In the dynamic landscape of Bangladesh’s economic policies, the recent shifts in the monetary domain have captured the attention of key players. The Bangladesh Bank’s unveiling of its monetary policy for the second half of the fiscal year 2023-24 has triggered reactions, discussions, and raised expectations. Let’s delve into the intricacies of this significant development, exploring various facets under distinct headings.

In Short

Bangladesh Bank (BB) confronts a multifaceted economic landscape in the latter half of Fiscal Year 2024, addressing internal challenges of stabilizing the exchange rate, managing inflation, and tackling high non-performing loans. Externally, global geopolitical tensions and trade uncertainties further complicate the situation. BB’s strategy involves tightening monetary controls to curb inflation while ensuring sufficient liquidity for growth sectors.

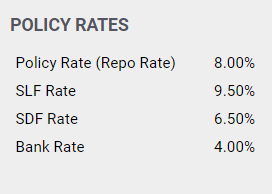

To navigate these challenges, BB adopts a prudent monetary stance, increasing the policy rate by 25 basis points to 8.00 percent. Liquidity management is refined, with adjustments to the Standing Lending Facility (SLF) and Standing Deposit Facility (SDF) rates, narrowing the policy rate corridor. The potential shift to a market-based exchange rate system, such as a crawling peg, is considered to stabilize the exchange rate amid Taka depreciation.

BB’s efforts align with global energy price expectations and internal production outlook, aiming to achieve the government’s revised inflation target of 7.50 percent by June FY24. The introduction of a crawling peg exchange rate system is anticipated to enhance foreign exchange stability.

Strategic directives for H2 FY24 focus on vigilant monetary policy, potential adoption of a crawling peg system, and robust non-performing loans management. Despite challenges, the economic outlook for end-FY24 remains positive, targeting 6.5 percent real GDP growth and moderated 7.5 percent inflation, with a focus on stability in the foreign exchange market and improved governance.

1. Policy Rate Hike

The Bangladesh Bank increased the policy rate, or repo rate, by 25 basis points to 8 percent, marking the eighth such increase since May 2022. This move aims to curb inflation by making borrowing costlier for banks. However, leaders express concerns about the potential repercussions on businesses and the available banking liquidity for private credit.

2. Leaders’ Perspectives on Inflation and Rate Hike

Kamran T Rahman, President of the Metropolitan Chamber of Commerce and Industry (MCCI), emphasizes the critical need to contain inflation to avoid widespread consequences. On the other hand, Ashraf Ahmed, President of the Dhaka Chamber of Commerce and Industry (DCCI), acknowledges the rate hike’s potential impact on money supply and banking liquidity, calling for a careful balance with supporting fiscal policies.

3. Private Sector Credit

The DCCI points out the disparities between the public and private sector credit growth targets. While the public sector’s credit growth target is set at 27.8 percent, the actual realization stands at 18 percent for the July-December period. In contrast, the private sector credit growth target is reduced to 10 percent, urging the central bank to explore options for increased liquidity.

4. Strategic Measures for Liquidity and Credit Flow

To address liquidity concerns and enhance credit flow, Ashraf Ahmed advocates for strategic measures. These include increasing public sector borrowing cautiously, avoiding crowding out the private sector, and exploring options like trade credit and factoring to boost liquidity.

5. Crawling Peg System

The DCCI recommends the introduction of a crawling peg system to stabilize the exchange rate. This system involves a balanced approach, allowing the local currency to fluctuate within a specified range. This, they believe, could address balance of payment challenges and ensure stability.

The Bangladesh Bank’s (BB) recent introduction of a crawling peg exchange rate system has sent ripples through the economic landscape. While the broad outlines are captured in other summaries, let’s delve deeper into the details in BB’s Policy Statement to understand its nuances and potential implications.

Key Insights from the Policy Statement:

Rationale for the Crawling Peg: The BB acknowledges the volatile exchange rate and its detrimental impact on foreign exchange reserves, inflation, and investor confidence. It views the crawling peg as a way to:

Dampen volatility: The pre-defined band around the peg aims to smooth out sharp fluctuations, providing predictability and stability for businesses and individuals.

Manage inflation: Gradual depreciation within the band can help moderate imported inflation by mitigating the impact of rising global commodity prices.

Enhance investor confidence: Predictable exchange rate movements can attract foreign investment and encourage international trade by reducing uncertainty.

Technical Details of the System:

The peg: While the specific currency and initial peg level aren’t explicitly mentioned in the document, the policy statement emphasizes linking the taka to a “carefully selected basket of currencies” to reduce reliance on any single currency.

The band: The policy statement proposes a “pre-determined narrow band,” but the specific width and adjustment mechanism remain somewhat ambiguous.

Adjustment frequency: The frequency of crawling adjustments (depreciation within the band) is also unspecified, leaving room for flexibility based on economic data and market conditions.

Policy Considerations:

Macroeconomic stability: The success of the crawling peg hinges on maintaining macro-economic stability through effective monetary and fiscal policies. Continued inflationary pressures could necessitate faster depreciation within the band, potentially negating the intended stability.

Export competitiveness: Overvaluation of the taka within the band needs to be avoided to safeguard export competitiveness. The BB highlights its commitment to export-oriented policies and close monitoring of the exchange rate to ensure optimal balance.

Transparency and communication: The BB emphasizes the importance of transparent communication with stakeholders to maintain trust and ensure smooth implementation of the crawling peg system.

Beyond the Policy Statement:

Historical context: Analyzing past experiences of crawling peg implementations in other countries, particularly those facing similar economic challenges, can offer valuable insights and potential pitfalls to avoid.

Market response: Monitoring market reactions and business sentiments following the announcement of the crawling peg can reveal its initial impact and provide early indications of its effectiveness.

Impact on specific sectors: Analyzing the potential impact of the crawling peg on various sectors like import-dependent industries, export-oriented businesses, and financial institutions can provide a more granular understanding of its economic consequences.

Staying Informed and Engaged:

The crawling peg represents a significant shift in Bangladesh’s exchange rate policy. By exploring the details outlined in the BB’s policy statement, considering other relevant factors, and remaining engaged in ongoing discussions, we can gain a deeper understanding of its potential impact and contribute to ensuring its successful implementation for a sound and stable Bangladeshi economy.

6. Challenges and Expectations

Despite high expectations, the Monetary Policy Statement falls short on concrete measures. The shift from monetary targeting to interest rate targeting raises questions, with adjustments in the policy rate, Interest Rate Corridor, and mixed messages creating uncertainty. The SMART-based lending rate policy remains untouched, limiting the transmission of the increased policy rate to lending rates.

7. Exchange Rate Regime: Unresolved Questions

The elephant in the room for monetary policy is the exchange rate regime. The commitment to switch to a market-based regime faces uncertainties, with considerations for a crawling peg exchange rate. However, details on design and implementation timelines remain unspecified.

8. GDP Growth and Inflation Targets: A Revised Outlook

The Bangladesh Bank revises GDP growth and inflation targets, reducing the former to 6.5 percent and increasing the latter to 7.5 percent. This adjustment acknowledges economic challenges and aligns with projections from international institutions. The central bank aims to strike a balance between growth and inflation control.

9. Cautious Optimism: Bangladesh Bank’s Stance

The Bangladesh Bank’s contractionary policy stance aims to tighten money supply and control inflation. The implementation of a crawling peg and adjustments in policy rates demonstrate a commitment to addressing economic challenges. The central bank anticipates a gradual reduction in inflation to 6 percent by June 2024.

10. Future Directions and Considerations

As Bangladesh navigates through economic uncertainties, the effectiveness of the monetary policy will unfold over the coming months. Addressing challenges related to inflation, liquidity, and credit flow requires a holistic approach. The evolving exchange rate regime and unresolved questions demand careful consideration and transparent communication.

Conclusion

Bangladesh’s monetary policy for the second half of FY24 sets the stage for a complex interplay of economic factors. The intricate balance between inflation control, liquidity management, and growth aspirations underscores the challenges and opportunities that lie ahead. As stakeholders closely monitor developments, the effectiveness of the strategic measures outlined in the policy will shape the trajectory of Bangladesh’s economic journey.

In the vast world of finance, interest rates play a pivotal role in determining the cost of borrowing and the return on investment. However, arriving at an appropriate interest rate for financial transactions can be complex. This is where the reference interest rate comes into play. In this blog post, we will delve into the concept of interest rate reference rates, their significance, and their impact on financial markets.

What is an Interest Rate Reference Rate?

An interest rate reference rate, also known as a benchmark rate or base rate, is a standardized interest rate that serves as a basis for determining the interest rates charged on various financial products and transactions. It acts as a common point of reference for lenders and borrowers, providing a transparent and consistent benchmark that reflects prevailing market conditions.

Importance and Applications:

Interest rate reference rates are integral to financial markets, fulfilling several crucial functions:

Pricing Loans: Banks and financial institutions use reference rates to determine interest rates on loans, mortgages, and other credit products. Lenders typically add a margin or spread to the reference rate based on factors such as credit risk, market conditions, and the borrower’s creditworthiness.

Valuing Fixed-Income Securities: Reference rates are essential in pricing and valuing fixed-income securities such as bonds, notes, and debentures. The interest rates on these securities often depend on a spread over a benchmark rate, allowing investors to assess their relative attractiveness.

Derivatives Pricing: Interest rate reference rates form a basis for pricing various interest rate derivatives such as interest rate swaps, options, and futures. These derivative contracts derive their value from fluctuations in reference rates, enabling market participants to manage interest rate risks.

Commonly Used Reference Rates:

A reference rate, or benchmark rate, is an interest rate that is used as the basis for setting other interest rates. Different types of transactions use different reference rate benchmarks, but some of the most common include:

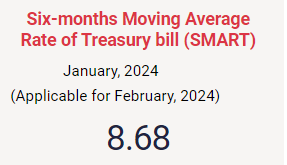

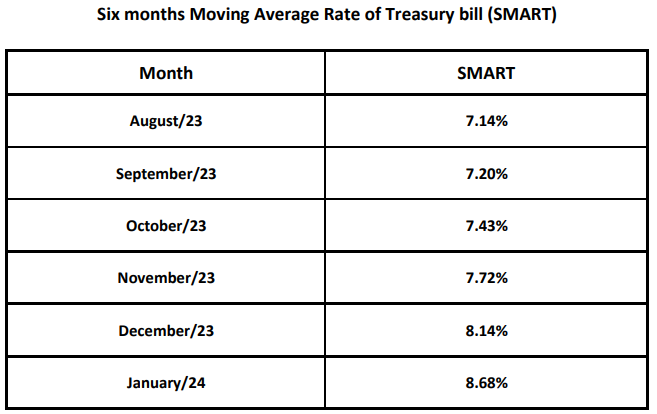

SMART (Six-month Moving Average Rate of Treasury Bills) by Bangladesh Bank (BB): The SMART is a six-month moving average of the interest rates on treasury bills issued by the Bangladesh Bank. It is used as a benchmark rate for short-term loans and other financial products. The current SMART rate is 7.10%, which is almost unchanged from the previous month(7,13% for May 2023).

London Interbank Offered Rate (LIBOR): Historically, LIBOR was one of the most widely used reference rates, serving as a benchmark for short-term interbank lending. However, due to concerns about its integrity, it is being phased out and replaced by alternative reference rates.

Euro Interbank Offered Rate (EURIBOR): Similar to LIBOR, EURIBOR serves as the benchmark rate for euro-denominated loans and financial products within the Eurozone.

US Treasury Yield Curve: The US Treasury Yield Curve represents the interest rates on US government bonds with different maturities. It provides a reference for pricing various fixed-income securities and serves as a key indicator of market sentiment.

The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate used in the United States to reference short-term U.S. dollar-denominated loans. It is based on the interest rates on overnight repurchase agreements (repos) that are collateralized by U.S. Treasury securities.

Regulatory Oversight and Reforms:

In recent years, there has been a significant shift in the landscape of interest rate reference rates due to regulatory reforms and the need for more robust and reliable benchmarks. Authorities around the world have been working on transitioning from existing reference rates like LIBOR to alternative rates based on more transactional data and stronger governance.

Conclusion:

Interest rate reference rates are vital components of the financial ecosystem, providing a standardized benchmark for pricing various financial products. They contribute to transparent and efficient markets, enabling lenders, borrowers, and investors to make informed decisions based on prevailing market conditions. As the financial landscape continues to evolve, the transition to alternative reference rates ensures the integrity and stability of interest rate benchmarks, reinforcing the foundation of global finance.

The “six-month moving average rate of treasury bills (SMART)” is a new monthly reference lending rate formula introduced by Bangladesh Bank on June 19, 2023, to be implemented in July 2023. It replaced the single-digit 6%-9% interest cap regime. The rate is fixed based on the weighted average rate of a six-month treasury bill plus a premium/margin.

The current margin is a maximum of 3.75%for banks and 5,75% for non-banking financial institutions since the last week of November.

The margin was up to 3% for banks and 5% for non-banking financial institutions at first when declared in June. Later, in October, it was increased to 3.50% for banks and 5,50% for financial institutions

Existing SMART Rate by BB

The Rate is from the Bangladesh Bank Website:

If we want to understand the SMART framework, we may take an example.

The prevailing Short-term Moving Average Rate of the Treasury Bill (SMART) is 8.68% as declared by BB applicable for February 2024. According to this framework, Banks can charge a maximum of 12.43% while FIs will be able to charge a 14.43% maximum on their credits. In the case of CMSMEs and consumer Loans, Banks can charge a maximum of 13.43% while Agricultural and Pre-Shipment Export Loans will be charged an 11.43% maximum.The below table may help with the calculation:

Particular

Lending Rates

Banks

SMART+ max 3.75% margin (Max 12.43%)

CMSMEs & Consumer Loans

An additional fee of up to 1% may be charged. (Max 13.43%)

Agricultural and Pre-Shipment Export Loans

SMART+ max 2.75% margin (Max 11.43%)

FIs

SMART+ max 5.75% margin ( Max 14.43%) CMSMEs & Consumer Loans (Max 15.43% including 1% charge)

Credit card loans

20% as before (not tagged with SMART)

The previous rate was as follows:

The smart rate will be reviewed every six months, and it may be adjusted up or down depending on market conditions.

SMART Reference Lending Rate in Bangladesh

The smart rate is very different from the previous single-digit lending rate cap, which was set in 2019. The Bangladesh Bank has said that the new rate is necessary to control inflation and ensure the stability of the financial system.

The SMART Reference Lending Rate is a new lending rate mechanism introduced by the Bangladesh Bank in July 2023. It is based on the six-month moving average rate of treasury bills (T-bills). Banks can add up to 3.75 percentage points to the SMART rate to fix their lending rates.

The current SMART rate for February 2024 is 8.68%. This means that banks can lend at a maximum rate of 13.43%, including the addition of a 1% supervision fee. The lending rate for agricultural and rural loans is 11.43%, and the lending rate for credit cards remains unchanged at 20%.

The SMART rate is reviewed every month, and it is expected to be adjusted in line with market conditions.

The SMART Reference Lending Rate is a more market-based and transparent lending rate mechanism than the previous system, which was based on the repo rate. It is expected to help reduce the spread between lending and deposit rates, and it provides banks with more flexibility in setting their lending rates.

Bangladesh Bank, in its Monetary Policy Statement for the July-December 2023 period, focuses more on being market-driven in both interest rate and exchange rate. As a step towards removing restrictions on banks’ lending and investment activities and setting up market-oriented interest rates, BB has introduced a new method of reference rate called SMART (Short-term Moving Average Rate of Treasury-Bill). The prevailing lending interest rate cap at 9% will be lifted from the beginning of July. The new interest rate framework is said to be market-driven in the sense that the offers for the yield on 182-Day T-bills usually come from participating financial institutions/individuals through primary dealers and the yield is not set by BB. Banks will have space to add margin depending on their different factors.

In this method, BB publishes the rate on the first day of every month on its website. The calculation methodology will take into account the yield of the 182-day Treasury bill. This reference rate will be active on 01-July-2023 and the lending interest cap will be set in the following manner.

SMART Reference lending rate calculation

The calculation of the smart rate by BB is a 3-step process shown as follows:

Weighted average rate of a six-month treasury bill

Firstly, BB will calculate the weighted average yield of the 182-Days T-bills on a weekly basis. The weighted average rate of a six-month treasury bill is the average interest rate that commercial banks pay when they borrow money from the Bangladesh Bank through treasury bill auctions. The weighted average rate is calculated by taking the total amount of money borrowed by commercial banks and dividing it by the total interest paid. It is done by the Debt Management Department, BB.

Premium

In the following step, BB will calculate a simple average of the four weeks’ weighted average yields every month. The premium is a margin that is added to the weighted average rate to determine the smart rate for loans and advances. The premium is intended to compensate commercial banks for the risks associated with lending money.

The premiums to be added are:

3.75% for banks (3.75% + 1% supervision fee can be added to personal, car, and consumer loans)

2.75% for Agricultural and Pre-Shipment Export Loans

5.75% for FIs

Lending rate

In the final stage, BB will compute the moving average of the yields over the past six months and this rate will be made public on the first working day of each month through the BB website. The lending rate is the rate of interest that commercial banks charge their customers when they borrow money. The lending rate is calculated by adding the weighted average rate and the premium.

Here are some of the factors that will be considered when setting the smart rate:

The inflation rate

The interest rate environment in other countries

The demand for and supply of credit in the domestic market

The stability of the financial system

The smart rate is reviewed every six months, and it may be adjusted up or down depending on market conditions. The Bangladesh Bank will consider several factors when setting the smart rate, including the inflation rate, the interest rate environment in other countries, the demand for and supply of credit in the domestic market, and the stability of the financial system.

Reference rates worldwide

All over the world, there are reference rates that commercial banks follow as a base rate for their lending operation. They may add the required premium or several premium factors to finalize their domestic lending rate. The rates may vary from entity to entity, individual to individual depending on various factors. In some countries, the central bank policy rate acts as the reference rate for commercial banks. For example, the Fed Funds Rate, the policy rate in the USA, is the reference rate in the USA.

For international lending operations, the LIBOR rate used to be the popular one. As the LIBOR phase-out is in transition, SOFR (Secured Overnight Financing Rate) for USD lending, SONIA (Sterling Overnight Index Average) for GBP lending, EONIA (Euro Overnight Index Average) for EUR loans, TONAR (Tokyo Overnight Average Rate) for JPY lending are becoming popular nowadays in replacement for LIBOR rate of different currencies.

The Story and History of SMART

Banks can charge a maximum of 12.43 percent interest on loans for now (a 1% charge can be added for CMSME and Consumer loans). The rate will be 14.43 percent (a 1% charge can be added for CMSME and Consumer loans) for non-bank financial institutions, meaning the spread between the lending and deposit interest rates will be a maximum of 3.75 percentage points.

SMART Launched

To trace the history, the Banking Regulation and Policy Department of Bangladesh Bank published a circular for the banks on June 19, 2023, about the interest rate with a special focus on the market-based rate with a new concept of SMART. It was applicable from July 2023. The prevailing lending interest rate cap at 9% is to be lifted from the beginning of July 2023.

Soon after the circular for banks, on June 20, 2023, the Department of Financial Institutions and Markets, Bangladesh Bank published another circular regarding interest rates for the FIs.

FIs can let their depositors enjoy interests of up to 2% above the SMART reference rate on deposits, and 5% above the SMART rate for loans and advances.

On November 27, 2023, the Banking Regulation and Policy Department of Bangladesh Bank published another circular for the banks allowing more 25 basis points on margin. So, banks now can add 3.75% margins to the existing SMART rate. So, the maximum rate now maybe 8.68% + 3.75%=12.43%. (11.43% for Agricultural and Pre-Shipment Export Loans whereas 13.43% for CMSMEs and Consumer loans as a 1% supervision charge can be applied)

Consequently, on November 29, 2023, the Department of Financial Institutions and Markets, Bangladesh Bank published another circular regarding interest rates for the FIs.

FIs can let their clients enjoy interests of up to 2.75% above the SMART reference rate on deposits, and charge 5.75% above the SMART rate for loans and advances.

As MPS mentioned, this new interest rate framework will act as a catalyst to make the interest rate dynamics in the market act freely as banks will be able to adjust the lending rate depending on market variations and other considerations. This will help efficient credit allocation of banks’ funds and expedite the competitiveness among banks. The interest rate will also be able to capture inflation expectations which will be incorporated while calculating SMART and it is said to have an impact to hold the rein of inflation.

It is mention-worthy that the SMART is more complicated than the previous single interest rate cap and it is variable in nature. The rate will vary every month. This might make some complications in calculating the end lending interest rate of commercial credits.

However, as per the circular, the interest rate cannot be changed within six months of its imposition. This means that even if the interest rate increases, the bank cannot raise it for existing customers.

The band or the corridor is too narrow to consider as market-aligned. Nonetheless, this move to make the interest rate free from the cage and to pave the way to have a rein on runaway inflation is appreciable.

Why did BB introduce a SMART Rate?

Bangladesh Bank recently introduced a SMART lending reference rate (SLRR) for banks to set their lending rates based on market conditions. This new system replaces the traditional base rate system. In this article, we will discuss the ten reasons why Bangladesh Bank introduced the SLRR system to list some of the potential advantages of the smart rate:

1. To Encourage Banks to Offer Competitive Rates

Under the traditional base rate system, banks set their lending rates based on their cost of funds and overheads. This led to high-interest rates, making it difficult for borrowers to obtain loans. By introducing the SLRR system, Bangladesh Bank hopes to reduce lending rates and make loans more affordable for businesses and individuals.

2. To Promote Financial Inclusion

By reducing lending rates, the SLRR system aims to encourage more people to take out loans, promoting financial inclusion across the country. Small and medium enterprises (SMEs) and low-income individuals, who previously struggled to access loans due to high-interest rates, will now be able to obtain credit at more affordable rates.

3. To Improve the Transparency of Lending Rates

The SLRR system is based on market conditions, which means that lending rates will be transparent and visible to borrowers. This increased transparency will help borrowers make better-informed decisions about their borrowing requirements.

4. To Support Economic Growth

By making loans more affordable, the SLRR system will encourage businesses to invest in new projects and expand existing ones, leading to job creation and economic growth.

5. To Reduce the Dependence on Informal Sources of Credit

Many low-income individuals and small businesses in Bangladesh have no choice but to turn to informal lenders for credit, as they cannot access formal loans due to high-interest rates. The SLRR system aims to reduce the dependence on these informal sources of credit by making formal loans more affordable.

6. To Encourage Banks to Adopt Good Lending Practices

The SLRR system takes into account the risk profile of borrowers, encouraging banks to adopt good lending practices and assess the creditworthiness of borrowers before granting loans.

7. To Increase Competition in the Banking Sector

The SLRR system aims to promote competition among banks by encouraging them to offer lower lending rates. This increased competition will benefit borrowers and promote innovation in the banking sector.

8. To Align Lending Rates with Market Conditions

Under the traditional base rate system, lending rates were not always aligned with market conditions, leading to high-interest rates even when market rates were low. The SLRR system aims to correct this by setting lending rates based on market conditions.

9. To Promote Financial Stability

The SLRR system takes into account the risks associated with lending, promoting financial stability by encouraging banks to adopt prudent lending practices.

10. To Align with International Best Practices

The SLRR system aligns with international best practices, making it easier for Bangladesh to attract foreign investment and integrate with the global economy.

11. To tame inflation.

The Bangladesh Bank believes that the smart rate will help to control inflation by making it more expensive for businesses to borrow money. This will discourage businesses from borrowing money and investing, which will help to slow down the economy and bring down inflation.

12. To ensure the stability of the financial system.

The Bangladesh Bank believes that the smart rate will help to ensure the stability of the financial system by making it more difficult for banks to make risky loans. This will help to prevent a financial crisis, which could have a devastating impact on the economy.

13. To make the lending rate more market-driven.

The previous lending rate cap was set by the Bangladesh Bank, which meant that commercial banks were not free to set their own lending rates. The smart rate will be based on market conditions, which will give commercial banks more flexibility in setting their lending rates. This could lead to more competition among banks, which could benefit consumers by lowering the cost of credit.

The introduction of the SMART lending reference rate system by Bangladesh Bank is a positive step towards promoting financial inclusion, encouraging good lending practices, and supporting economic growth. The system aims to reduce lending rates, increase transparency, and align with international best practices, making it easier for borrowers to access credit and encouraging banks to compete on rates.

Impacts of the SMART Rate

The smart rate is a new tool that the Bangladesh Bank will use to manage the country’s monetary policy. It remains to be seen how effective the rate will be in achieving its objectives. However, it is a significant departure from the previous lending rate cap, and it could have a major impact on the availability and cost of credit in Bangladesh.

The cost of credit could increase, which could make it more difficult for businesses to borrow money and invest. This could slow down the economy and lead to job losses.

The availability of credit could decrease, as banks may be less willing to lend money at higher interest rates. This could make it more difficult for businesses and consumers to access credit, which could hurt the economy.

The smart rate could lead to more competition among banks, as they will be trying to attract customers by offering lower interest rates. This could benefit consumers by lowering the cost of credit.

More market-based and transparent lending rate mechanism. The SMART rate is based on the six-month moving average rate of treasury bills, which is a more market-based indicator than the previous lending rate regime, which was based on the repo rate. This means that the SMART rate is more responsive to changes in market conditions, and it is also more transparent, as it is based on an observable market rate.

Reduced spread between lending and deposit rates. The SMART rate is expected to help reduce the spread between lending and deposit rates. This is because the SMART rate is more market-based, which means that it is more likely to reflect the true cost of funds for banks. As a result, banks will be less likely to mark up their lending rates above the cost of funds, which will help to narrow the spread between lending and deposit rates.

More flexibility for banks in setting lending rates. The SMART rate provides banks with more flexibility in setting their lending rates. This is because banks can add up to 3 percentage points to the SMART rate to fix their lending rates. This flexibility will allow banks to better compete for customers and to offer more competitive lending rates.

Improved efficiency of the lending market. The SMART rate is expected to improve the efficiency of the lending market. This is because the SMART rate is more market-based and transparent, which will make it easier for borrowers and lenders to find each other. As a result, the SMART rate is expected to help to reduce the cost of credit for borrowers and to improve the efficiency of the lending market.

Improved risk management by banks. The SMART rate is based on the six-month moving average rate of treasury bills, which is a more stable indicator than the repo rate. This means that the SMART rate is less likely to fluctuate sharply, which will make it easier for banks to manage their risk. As a result, banks will be less likely to suffer losses due to unexpected changes in interest rates.

Overall, the impact of the smart rate is uncertain. It could have both positive and negative effects on the economy. Only time will tell how effective the rate will be in achieving its objectives. Reference rates are constantly evolving as the financial markets change. For example, the LIBOR is being phased out and replaced by new reference rates, such as the Secured Overnight Financing Rate (SOFR). This is because LIBOR has been criticized for being manipulated by banks and for not being a reliable indicator of the true cost of borrowing money.

Challenges of the SMART Rate

The smart rate is a new monetary policy tool that has the potential to both benefit and challenge the Bangladeshi economy. Some of the potential challenges of the smart rate include:

Increased cost of credit: The smart rate is based on the weighted average rate of a six-month treasury bill, which is currently at 7.72%. This means that the smart rate is likely to be higher than the previous lending rate cap of 9%. This could make it more expensive for businesses and consumers to borrow money, which could slow down economic growth.

Decreased availability of credit: If the smart rate is too high, banks may be less willing to lend money. This could make it more difficult for businesses and consumers to access credit, which could also slow down economic growth.

Increased volatility in the financial markets: The smart rate is a market-based tool, which means that it is subject to change based on market conditions. This could lead to increased volatility in the financial markets, which could make it more difficult for businesses and investors to plan for the future.

Difficulties in managing the tool: A SMART rate is a new tool, and it is not yet clear how the Bangladesh Bank will be able to effectively manage it. If the Bangladesh Bank is not able to manage the tool effectively, it could lead to unintended consequences for the economy.

In addition to the challenges mentioned above, there are a few other potential challenges that could arise from the implementation of the smart rate. These include:

Lack of transparency: The smart rate is a complex calculation, and it is not clear how the Bangladesh Bank will calculate it. This lack of transparency could make it difficult for businesses and consumers to understand how the smart rate will affect them.

Inflationary pressures: If the smart rate is too high, it could lead to inflationary pressures. This is because businesses may pass on the higher interest costs to consumers in the form of higher prices.

Negative impact on the financial sector: The smart rate could hurt the financial sector. This is because banks may be less willing to lend money if the smart rate is too high. This could lead to a decrease in lending, which could hurt economic growth.

It is important to note that these are just potential challenges. The actual impact of the smart rate will depend on several factors, including how the Bangladesh Bank manages the tool and how the market reacts to it.

Is SMART really smart?

There are several reasons why the SMART Reference Lending Rate (SRLR) is considered to be “smart.” First, the SRLR is based on a weighted average of the lending rates of commercial banks. This means that it is more reflective of the actual cost of lending in the market, as opposed to the previous lending rate, which was set by the Bangladesh Bank.

Second, the SRLR is reviewed every month, which means that it can be adjusted more quickly to changes in market conditions. This can help to ensure that the SRLR remains a fair and competitive lending rate.

Third, the SRLR is transparent and publicly available. This means that businesses and consumers can easily see what the SRL is, and they can use this information to make informed decisions about their borrowing.

Overall, the SMART Reference Lending Rate is a positive development for the Bangladeshi economy. It is expected to help to reduce lending costs, improve the efficiency of the financial system, and promote economic growth.

However, some argue that the SRLR is not really “smart” after all. They also argue that the SRL is not responsive enough to changes in market conditions.

Only time will tell whether the SRLR is truly a “smart” lending rate. However, the early signs are promising, and the SRLR will likely have a positive impact on the Bangladeshi economy.

Last Lines

The SMART Reference Lending Rate is a new lending rate mechanism in Bangladesh that is based on the six-month moving average rate of treasury bills. It is more market-based and transparent than the previous lending rate regime, and it is expected to help reduce the spread between lending and deposit rates. The current SMART rate for February 2024 is 8.68%, and banks can add up to 3.75% points to this rate to fix their lending rates whereas FIs can add 5.75%.

Bancassurance is a term used to describe a business model in which a bank and an insurance company cooperate to offer products to their customers. The goal of Bancassurance is to provide customers with a one-stop-shop for all their financial needs. In addition to providing convenience, it also offers customers the opportunity to save money on fees.

BB issued a circular to launch bancassurance on December 12, 2023, on the same day.

Bancassurance in Bangladesh

Bancassurance is a term used to cooperate between a bank and an insurance company. The bank sells insurance products to its customers, and the insurance company uses the bank’s distribution channels and customer base to sell its products. In Bangladesh, Bancassurance is about to start. Banks in Bangladesh are going to expand their product offerings to include more insurance products.

Bancassurance is a combination of banking and insurance services offered by a single institution.

Bangladesh is a rapidly growing country with a large population. To build a strong economy, the government is interested heavily in Bancassurance. The government can keep its finances safe and ensure that its citizens are not at risk by providing insurance.

Learning more about how Bancassurance can help you in your business and personal life.

How Bancassurance Can Benefit Businesses?

To create a safe and secure environment for their customers, the government of Bangladesh is investing in Bancassurance.

This partnership allows the bank to offer insurance products to their customers.

The two businesses offer life insurance, health insurance, and property insurance to their customers. Bancassurance can benefit companies in Bangladesh by providing a way to provide their customers with various products, including insurance products. This can help the businesses attract and keep customers.

The product is usually marketed through the bank’s branches and provides customers with an easy way to buy insurance products.

The bank typically sells the insurance products, while the insurance company provides underwriting and claims processing. This type of arrangement can benefit businesses in Bangladesh in several ways.

The main benefits of Bancassurance for businesses in Bangladesh include:

1. Increased sales and revenue: Businesses can increase their sales and revenue by offering bancassurance products.

2. Increased customer acquisition: By offering bancassurance products, businesses can increase their customer acquisition and retention.

3. Decreased cost: Businesses can decrease their costs by offering bancassurance products.

4. Increased credit availability: By offering bancassurance products, businesses can increase the amount of credit.

5. Increased market reach: By offering bancassurance products, businesses can expand the market they serve and gain access to new customers and markets.

Bancassurance can benefit businesses in Bangladesh in a few more ways.

First, it can help businesses grow by providing them with an opportunity to sell insurance products to their customers.

Second, it can help businesses to save money by allowing them to bundle their insurance products with their banking products.

Third, Bancassurance can help businesses to save money on their insurance premiums.

Fourth, Bancassurance can help businesses save money on the costs associated with underwriting and claims processing.

Fifth, customers may avail of additional services.

Sixth, Bancassurance can help reduce the risk of fraud or financial crimes.

How Does Bancassurance Benefit Banks?

There are many reasons why Bancassurance is lucrative to banks. The company has provided this insurance for many years because it has been able to keep its finances safe. The government can keep its finances safe and ensure that its citizens are not at risk by providing this insurance.

Bancassurance can help to ensure that your business is there when times are tough, and you require support. You can have a team to help you through these times, and Bancassurance can help you keep your financial stability.

Bancassurance is a business model that allows banks to offer their customers life insurance and other financial products. Banks can benefit from this arrangement by earning commissions on the sales of the insurance products and by earning interest on the deposits used to fund the policies. The bank can also benefit because it is the only institution that the customer deals with when buying insurance, leading to increased loyalty and repeat business.

It provides customers with a wide variety range of products. By offering insurance products through the bank, the bank can benefit from increased customer loyalty, cross-sell opportunities, and an expanded customer base. In addition, the insurance company can benefit from the bank’s distribution network and reach a more extensive customer base.

So, the benefits for banks incorporate:

Increased customer base

Increased profits

Reduced costs

Improved customer service

Improved Customer Satisfaction

Improved fraud prevention

Increased cross-selling opportunities

Increased Efficiency

Enhanced Risk Management

How Does Bancassurance Benefit Insurance Companies?

Bancassurance, the collaboration between banks and insurance companies, offers several benefits in the context of Bangladesh. Here are specific advantages for insurance companies in the Bangladeshi market:

Enhanced Market Penetration:

Bancassurance provides insurance companies in Bangladesh with a valuable opportunity to expand their market reach. By leveraging the extensive branch network of banks, insurers can access a larger customer base.

Cost-Effective Distribution:

Establishing separate distribution channels can be expensive. Bancassurance allows insurance companies to utilize the existing infrastructure of partnering banks, resulting in cost savings related to setup and maintenance.

Customer Trust and Credibility:

Banks are often regarded as trustworthy financial institutions by the Bangladeshi population. Partnering with banks enhances the credibility of insurance products, instilling trust among customers.

Financial Inclusion:

In a country like Bangladesh, where segments of the population may be underserved or financially excluded, Bancassurance can contribute to financial inclusion. Access to insurance products through banks brings financial services to a broader demographic.

Cross-Selling Opportunities:

Bancassurance partnerships facilitate cross-selling opportunities. Insurance companies can collaborate with banks to bundle insurance products with other financial services, providing customers with comprehensive financial solutions.

Regulatory Compliance:

Bangladesh has specific regulations governing the financial services sector. Bancassurance ensures that insurance products comply with these regulations, as banks are well-versed in regulatory requirements and can assist in adherence.

Tailored Product Development:

Working closely with banks allows insurance companies to tailor their products to the specific needs and preferences of the Bangladeshi market. This customization can result in more relevant and attractive offerings for customers.

Technology Integration:

Many banks in Bangladesh are adopting digital technologies. Bancassurance partnerships enable insurance companies to leverage these technological advancements for streamlined processes, efficient customer service, and digital distribution.

Risk Diversification:

For insurance companies in Bangladesh, diversifying distribution channels is a risk mitigation strategy. Relying on Bancassurance alongside other channels provides a diversified approach to market exposure.

Increased Awareness and Education:

Banks, being key financial touchpoints, can play a crucial role in increasing awareness about insurance products. Bancassurance allows for collaborative efforts to educate customers on the importance and benefits of insurance.

Localized Marketing:

Banks have a deep understanding of local markets and customer preferences. Through Bancassurance, insurance companies can benefit from the localized marketing expertise of their banking partners.

Long-Term Strategic Partnerships:

Bancassurance partnerships in Bangladesh can foster long-term relationships between banks and insurance companies. Building strong partnerships contributes to stability and continuity in the distribution of insurance products.

What are the types of Bancassurance?

Bancassurance refers to the distribution of insurance products through banks. It is a partnership between a bank and an insurance company to provide a wide range of insurance products to the bank’s customers. There are several types of Bancassurance models, each with its own characteristics. Here are some common types:

Pure Distribution Model:

In this model, the bank acts as a distribution channel for insurance products.

The bank’s role is limited to selling insurance products, and it does not get involved in the underwriting or policy management.

Referral Model:

Under the referral model, the bank refers its customers to the insurance company, and the insurance company takes care of the sales process.

The bank earns a commission or fee for every successful referral.

Co-Branding Model:

In a co-branding Bancassurance model, both the bank and the insurance company share their brand names on the insurance products.

This model leverages the trust and credibility associated with both the bank and the insurance provider.

Joint Venture Model:

Some banks and insurance companies form a joint venture to create a separate entity that exclusively handles Bancassurance activities.

This model allows for a more integrated approach, with both partners actively participating in the management and operations.

Integrated Model:

In an integrated Bancassurance model, insurance products are integrated with other banking products and services.

Customers may, for example, have insurance coverage linked to their bank accounts, loans, or credit cards.

Product bundling Model:

This model involves bundling insurance products with other financial products offered by the bank.

Customers may receive a package deal that includes banking services, loans, and insurance coverage.

Online Bancassurance:

With the rise of digital banking, many Bancassurance activities have moved online.

Customers can purchase insurance products through the bank’s online platform or mobile banking app.

Micro Bancassurance:

This model focuses on offering insurance products with lower premiums and coverage tailored to specific customer segments.

It is particularly relevant for reaching the underbanked or those with limited insurance coverage.

The choice of Bancassurance model depends on the strategic goals of both the bank and the insurance company, the regulatory environment, and the preferences of the target market. Each model has its advantages and challenges, and successful Bancassurance partnerships often involve a deep understanding of customer needs and effective collaboration between the bank and the insurance provider.

What are the products of Bancassurance?

The products offered by bancassurance companies vary but often include banking products such as checking and savings accounts, credit cards, mortgages, and insurance products such as auto, home, and health insurance.

Bancassurance is a practice where banks and insurance companies offer products from both industries to their customers. The products available through Bancassurance can include anything from car insurance to life insurance, and banks often promote these products to get customers to buy multiple services from the same institution. Proponents of Bancassurance argue that it offers customers convenience and simplicity, while critics say that it can lead to higher prices and reduced competition.

Who started Bancassurance?

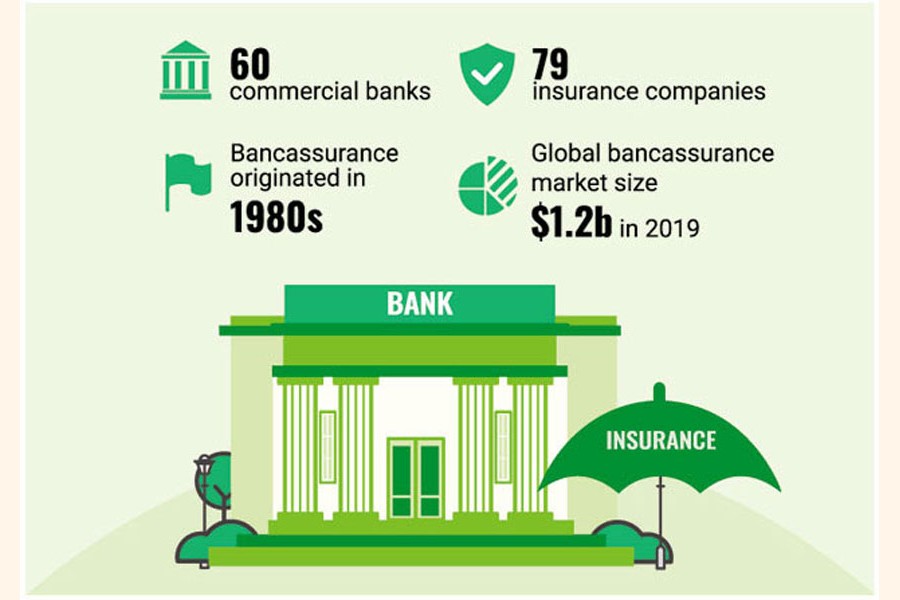

Bancassurance started in the 1980s in French and developed both in France and Spain. Some credits Barclay’s Life, an insurance subsidiary, formed in 1965 in the UK for pioneering of Bancassurance.

In Bangladesh, this sector will be overgrowing due to the increasing demand for insurance services from the people. The leading players in the bancassurance market are the banks and the insurance companies. The banks provide the products and services of the insurance companies to their customers, while the insurance companies use the bank’s network to reach a more extensive customer base.

Banks and insurance companies will play in the bancassurance field under the FID, IDRA, and Bangladesh Bank.

Chief Bancassurance Officer (CBO)

The role of the Chief Bancassurance Officer (CBO) is to lead the development and execution of the bank’s bancassurance strategy. In addition, the CBO works with the CEO and senior management to identify and assess opportunities for Bancassurance, develop product and distribution plans, and manage the relationship with the insurance company. In Bangladesh, the CBO is a new position that is being created in response to the growth of Bancassurance.

Eligibility to lead the wing as CBO

A Master’s degree and 12 years of experience in banking or insurance

will lead the wing as CBO. His grade will be within the five but below the CEO of the banks.

The wing, however, can not force the customer to take the insurance policy. It can offer retail and SME insurance products but not corporate customers. In addition, the officers cannot provide misleading information to the bank clients to sell the products.

Bancassurance is a business model banks and insurance companies use to offer products from both industries to their customers. It has become popular in recent years as a way for banks to grow their profits, and many countries have seen an increase in bancassurance businesses. Bangladesh is one of those countries, and the bancassurance industry is increasing.