After filing bankruptcy, your credit score is likely to be significantly affected and will generally lower your credit score. Bankruptcy has a negative impact on your creditworthiness and can stay on your credit report for several years, making it difficult to secure new credit or loans.

However, with time and responsible financial behavior, it is possible to rebuild your credit score. Rebuilding credit after bankruptcy requires consistent and on-time payments, keeping credit utilization low, and gradually adding positive credit history to your report. By following these steps, you can improve your credit score over time.

Credit: www.debt.org

Factors Affecting Your Credit Score After Filing Bankruptcy

Filing for bankruptcy can have a significant impact on your credit score. After filing, factors such as payment history, debt-to-income ratio, and credit utilization play a crucial role in rebuilding your creditworthiness. It’s important to establish positive financial habits to improve your score over time.

Impact Of Bankruptcy On Your Credit Score

Declaring bankruptcy can have a significant impact on your credit score. It is a negative mark that stays on your credit report for several years, making it more challenging to obtain credit in the future. Bankruptcy can lower your credit score substantially, often plummeting it by 100 or more points. This reduction can make it difficult to secure loans, credit cards, or even rent an apartment. However, it’s important to understand that this is not the end of the road for your credit score.

Despite the challenges, it is possible to rebuild your credit score after bankruptcy. By taking positive steps and implementing responsible financial strategies, you can gradually improve your creditworthiness. Here are some crucial steps to help you rebuild your credit:

Importance of Timely Payments: Paying your bills on time is critical in rebuilding your credit score. Establishing a history of making on-time payments demonstrates financial responsibility to lenders and shows your commitment to meeting your financial obligations.

Managing Your Finances Wisely: Take control of your finances by creating a budget and sticking to it. This will help you avoid unnecessary spending and ensure that you have enough money to cover your essential expenses and debt payments.

Managing Your Finances Wisely

Avoid new debt: While seeking to rebuild your credit, it’s crucial to avoid accumulating new debt that you may struggle to repay. Focus on managing existing debt responsibly, rather than taking on additional financial obligations.

Establish an emergency fund: Building an emergency fund can provide a safety net during unforeseen circumstances. This fund can help you avoid relying on credit cards or loans for unexpected expenses and prevent future financial setbacks.

By implementing these steps and creating responsible financial habits, you can slowly but surely improve your credit score after bankruptcy. Remember, rebuilding your credit takes time and patience, but with dedication and discipline, you can regain your financial footing.

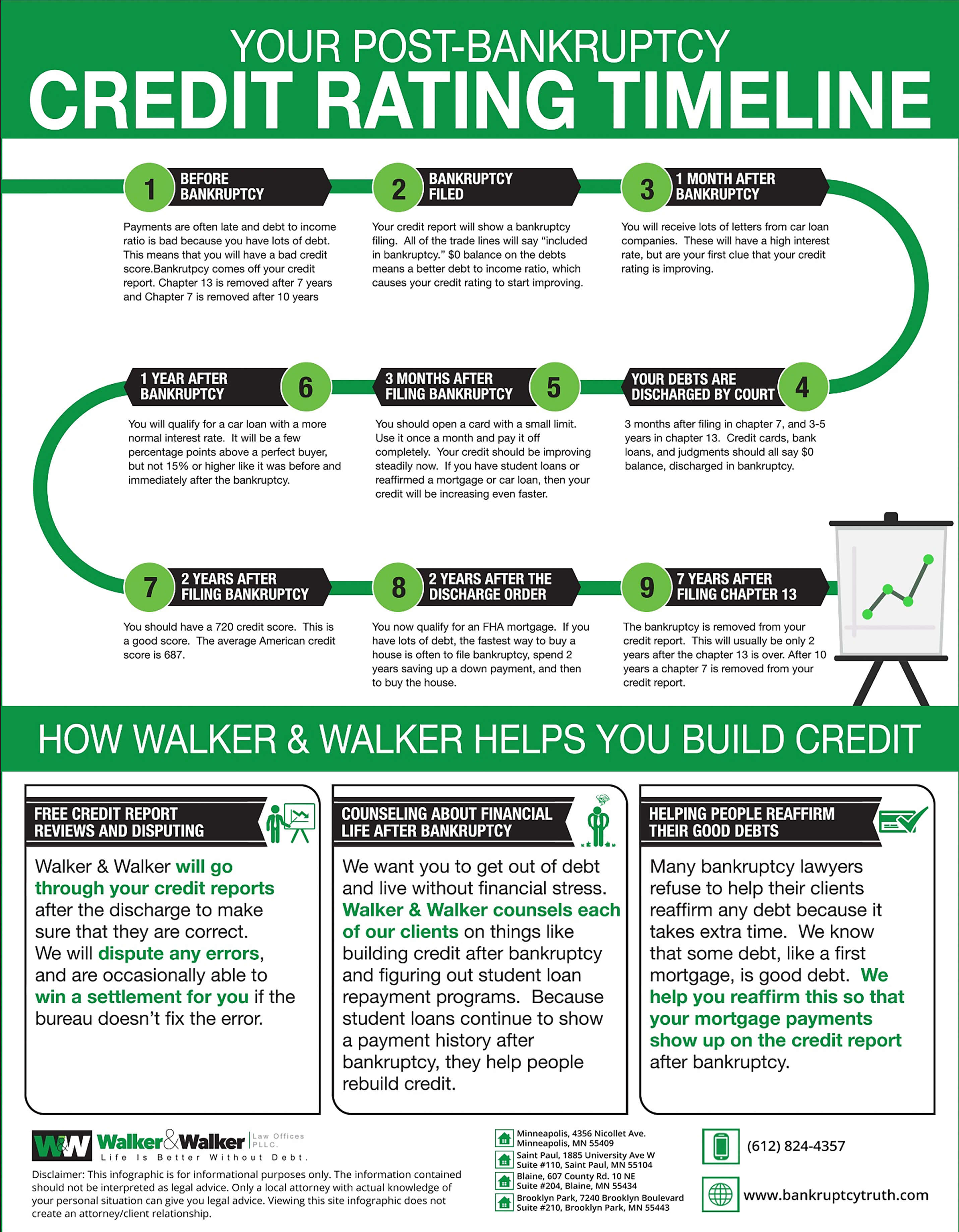

Credit: www.bankruptcytruth.com

Credit: www.harmonandgorove.com

Frequently Asked Questions Of After Filing Bankruptcy What Is Your Credit Score

What Is The Average Credit Score After Bankruptcy?

The average credit score after bankruptcy varies. It depends on various factors, such as your financial behavior post-bankruptcy and how you manage your debts. Building credit from scratch is possible, and with responsible financial decisions, you can improve your credit score over time.

Does My Credit Score Start Again After Bankruptcy?

Your credit score does not start again after bankruptcy. It takes time to rebuild your credit history and improve your score. Successfully managing your finances and making on-time payments can help you rebuild your credit over time.

How Much Will My Credit Score Go Up When Bankruptcy Falls Off?

Your credit score will likely increase when bankruptcy is removed, but the exact amount is hard to determine. It depends on other factors like your credit history, payment behavior, and current financial situation. Be patient, practice responsible borrowing, and eventually, your score will improve.

What Would Your Credit Rating Be If You Are Declare Bankruptcy?

If you declare bankruptcy, your credit rating will be negatively impacted.

Conclusion

Ultimately, filing for bankruptcy will have an impact on your credit score. However, it is not the end of the road. With time and responsible financial behavior, you can start rebuilding your credit. Stay diligent in making timely payments, keeping your debt levels low, and regularly checking your credit report.

Remember, the key is perseverance and patience as your credit score will gradually improve over time. Stay committed to your financial goals, and you will be on the path to a healthier credit future.

The best personal loan to consolidate credit card debt is one that offers a low interest rate and flexible repayment terms. Consolidating credit card debt with a personal loan can help you pay off your debt faster and save money on interest.

By combining multiple credit card balances into one loan, you can streamline your monthly payments and simplify your financial management. With a lower interest rate, you can also reduce the overall cost of your debt.

Credit: www.creditkarma.com

Benefits Of Personal Loan For Credit Card Debt Consolidation

Are your credit card debts piling up and causing you financial stress? Are you finding it difficult to manage multiple monthly credit card payments? If so, a personal loan for credit card debt consolidation may be the solution you’re looking for. Consolidating your credit card debts into a single personal loan can offer you a range of benefits, including lower interest rates and a single monthly payment. In this article, we’ll explore these two key benefits in more detail, helping you understand why a personal loan could be the perfect tool to regain control of your financial situation.

Lower Interest Rates

If you’re struggling to manage high credit card interest rates, a personal loan can provide much-needed relief. Personal loans generally come with lower interest rates compared to credit cards, helping you save money in the long run. With a lower interest rate, a significant portion of your monthly payment goes towards paying down the principal and reducing your debt. This means you’ll be able to clear your credit card debt faster and save on interest charges. Imagine the peace of mind that comes with making progress on your debt while paying less interest each month!

Single Monthly Payment

Keeping track of multiple credit card payments can be overwhelming. With a personal loan for credit card debt consolidation, you can simplify your financial life by combining all your credit card debts into a single monthly payment. This means no more juggling due dates, ensuring you never miss a payment again. By consolidating your debts, you’ll have a clear overview of your finances, making it easier to budget and manage your monthly obligations effectively. Plus, a single monthly payment can help improve your credit score by showcasing your ability to handle your financial commitments responsibly.

Don’t wait any longer to take control of your credit card debt and relieve financial stress. Consider the benefits of a personal loan for credit card debt consolidation, and confidently embark on your journey towards a debt-free future.

Credit: www.cnbc.com

Factors To Consider When Choosing A Personal Loan For Credit Card Debt Consolidation

When it comes to consolidating credit card debt, a personal loan can be a smart option. However, not all personal loans are created equal. It’s important to carefully consider several factors before choosing the best personal loan for credit card debt consolidation. By taking these factors into account, you can ensure that you’re making a well-informed decision that will ultimately save you money and help you regain control over your finances.

Interest Rates

One of the most crucial factors to consider when selecting a personal loan for credit card debt consolidation is the interest rate. The interest rate plays a significant role in determining the overall cost of the loan. A lower interest rate can save you money in the long run, so it’s important to shop around and compare rates from different lenders. Remember to look for fixed interest rates that won’t fluctuate over time.

Loan Term

The loan term is another important consideration when choosing a personal loan for credit card debt consolidation. The loan term refers to the length of time you have to repay the loan. It’s worth noting that a longer loan term may result in lower monthly payments, but it also means you’ll end up paying more in interest over the life of the loan. On the other hand, a shorter loan term may mean higher monthly payments, but it could save you money on interest in the long run. Consider your financial situation and choose a loan term that aligns with your goals and ability to repay.

Origination Fees

In addition to interest rates and loan terms, it’s essential to consider any origination fees associated with the personal loan. Origination fees are charges that lenders may impose to cover the costs of processing and underwriting the loan. These fees can vary widely between lenders, so it’s crucial to compare them and factor them into your decision-making process. Keep in mind that while a loan with no origination fees may seem like the best choice, it’s important to consider the overall cost of the loan, including interest rates and other fees.

Steps To Apply For A Personal Loan For Credit Card Debt Consolidation

Applying for a personal loan to consolidate credit card debt is a simple process that can help you manage your finances more effectively. By following a few steps, you can find the best loan option for your needs and start working towards reducing your debt.

Check Your Credit Score

Before applying for a personal loan to consolidate credit card debt, it’s important to check your credit score. Your credit score plays a crucial role in determining whether you will qualify for a loan and what interest rate you will be offered. You can check your credit score for free using various online platforms.

Once you have your credit score, make sure it falls within a reputable range. Generally, a higher credit score will increase your chances of getting a loan with a lower interest rate. If your score is lower than expected, take some time to improve it by paying off your existing debt and making all your payments on time.

Compare Loan Offers

When searching for the best personal loan to consolidate your credit card debt, it’s essential to compare loan offers from different lenders. This will help you find the most favorable terms, interest rates, and repayment options.

Start by researching reputable lenders and checking their loan products. Look for lenders that specialize in debt consolidation loans and have positive customer reviews. Once you have a list of potential lenders, request loan quotes from each one, focusing on important factors like interest rates, loan terms, and any fees or penalties involved.

Gather Required Documentation

Before applying for a personal loan for credit card debt consolidation, gather all the required documentation. Having these documents ready will accelerate the loan application process and increase your chances of getting approved.

Required Documentation:

Proof of identity (e.g., driver’s license, passport)

Proof of income (e.g., pay stubs, tax returns)

Proof of residence (e.g., utility bills, rental agreement)

Recent credit card statements

Bank statements

Having these documents readily available will demonstrate your preparedness to potential lenders and speed up the application process. Remember to double-check the specific requirements of your chosen lender, as documentation may vary slightly.

Tips For Successful Credit Card Debt Consolidation With A Personal Loan

Consolidating credit card debt with a personal loan can be a smart decision to regain control of your finances. By combining multiple high-interest credit card balances into one lower-interest loan, you can reduce your overall debt, lower your monthly payments, and simplify your financial life. However, it’s important to approach debt consolidation with a strategic plan to ensure its success. Here are some essential tips to consider when consolidating credit card debt with a personal loan:

Create A Budget And Stick To It

One of the key factors in successful credit card debt consolidation is creating a realistic budget and diligently sticking to it. A budget helps you understand your income, expenses, and how much you can afford to allocate towards debt repayment each month. It allows you to prioritize your financial goals and track your progress effectively. To create a budget:

List all your sources of income.

Make a comprehensive list of all your monthly expenses.

Identify areas where you can cut back on spending.

Determine how much you can comfortably allocate towards your debt consolidation loan.

Avoid Taking On More Debt

When consolidating credit card debt with a personal loan, it’s crucial to resist the temptation of taking on more debt. Without the burden of multiple credit card balances, you may feel a sense of relief and an urge to spend again. However, this defeats the purpose of consolidating debt and can lead to a vicious cycle of continuously accumulating debt. To avoid taking on more debt:

Leave your credit cards at home when going shopping.

Only use your credit cards for emergencies.

Track your spending and be mindful of impulse purchases.

Focus on paying off your debt consolidation loan instead of accruing new debt.

Consider Debt Counseling

If you find yourself overwhelmed with credit card debt and struggling to manage your finances effectively, seeking professional debt counseling can be immensely beneficial. Debt counselors are experts who can provide guidance on budgeting, debt management, and financial strategies tailored to your specific situation. They can help you:

Create a personalized debt repayment plan.

Negotiate with creditors to lower interest rates or reduce fees.

Provide education on financial management and responsible credit card usage.

Offer emotional support and motivation throughout your debt consolidation journey.

By following these tips for successful credit card debt consolidation, you can improve your financial footing and pave the way towards a debt-free future. Remember, debt consolidation is just one step in the journey towards financial freedom, and it takes discipline and commitment to achieve long-term financial stability.

Credit: www.cnbc.com

Frequently Asked Questions On Best Personal Loan To Consolidate Credit Card Debt

Can You Consolidate Credit Card Debt With A Personal Loan?

Yes, you can consolidate credit card debt using a personal loan. It helps combine multiple debts into one loan with a lower interest rate. This simplifies repayment and can save money on interest charges.

What Type Of Loan Should I Get To Pay Off Credit Card Debt?

To pay off credit card debt, consider getting a debt consolidation loan. It combines all your debts into one loan with a lower interest rate, making it easier to manage and pay off.

What Is The Best Credit Card Debt Consolidation Program?

The best credit card debt consolidation program is subjective, as it depends on individual needs. Explore reputable programs with low interest rates, flexible repayment terms, and good customer reviews. Compare options and choose a program that aligns with your specific financial goals.

Do Consolidation Loans Hurt Your Credit Score?

Consolidation loans can affect your credit score. By applying for a new loan, your credit report may show a hard inquiry, which can temporarily lower your score. However, if you make timely payments on the consolidation loan, it can ultimately improve your credit by reducing your overall debt.

Conclusion

Consolidating your credit card debt with a personal loan can be a smart move to regain control of your finances. By choosing the best personal loan option for debt consolidation, you can simplify your monthly payments and potentially save on interest charges.

Remember to carefully consider factors like interest rates, terms, and fees before making a decision. Don’t let credit card debt weigh you down any longer – take action and find the best personal loan for your needs today.

Tricks to pay off credit cards faster include making extra payments and prioritizing high-interest debt. Paying off credit cards quickly can help save money on interest charges and improve overall financial well-being.

We will explore a variety of strategies and tips that can help individuals pay off their credit card debt more efficiently. By implementing these tricks, individuals can take control of their finances and achieve their goal of becoming debt-free. Whether it’s creating a budget, using balance transfer cards, or seeking professional help, there are numerous approaches to pay off credit card debt faster.

Let’s dive in and explore these strategies in detail.

Credit: www.linkedin.com

1. Prioritize High-interest Debt

Pay off your credit cards faster by prioritizing high-interest debt. Start by paying off the cards with the highest interest rates first to save money and become debt-free sooner.

When it comes to paying off credit card debt, it’s important to have a strategy in place. One of the most effective tricks is to prioritize high-interest debt. By tackling your high-interest cards first, you can save a significant amount of money on interest payments in the long run. Here are some practical steps to help you get started:

Pay Off High-interest Cards First

Start by identifying the credit cards with the highest interest rates. These are the ones that are costing you the most money in interest charges each month. By focusing on paying off these high-interest cards first, you can make a significant dent in your overall debt.

To do this, carefully examine your credit card statements and make a list of the interest rates associated with each card. Once you have this information, prioritize your payments accordingly. Allocate the majority of your available funds towards paying off the card with the highest interest rate while making minimum payments on the others.

Consider Balance Transfers

In addition to prioritizing high-interest debt, another trick to pay off credit cards faster is by considering balance transfers. A balance transfer involves moving the balance from one credit card to another with a lower interest rate. This can be a savvy move if you can secure a promotional interest rate and if the new card offers favorable terms.

When considering a balance transfer, be sure to read the fine print and understand any fees or charges associated with the transfer. Additionally, pay attention to the promotional interest rate period to ensure you can realistically pay off the debt within that timeframe.

It’s important to note that a balance transfer alone won’t solve your debt problem. It’s merely a tool to help you save money on interest charges. Once you transfer the balance, make a plan to pay off the debt as quickly as possible.

By prioritizing high-interest debt and considering balance transfers, you can accelerate your journey towards becoming debt-free. These tricks can help you save money on interest payments and provide a clear roadmap for paying off credit cards faster. Remember to stay disciplined in your approach, stick to your repayment plan, and celebrate each milestone along the way.

2. Create A Budget And Stick To It

Creating a budget is a crucial step towards paying off your credit cards faster. It helps you gain control of your finances and enables you to allocate your money wisely. A budget ensures that you are aware of your expenses, income, and debt obligations, making it easier to track your progress and stay on top of your financial goals.

Track Your Expenses

Tracking your expenses is the first step to creating an effective budget. It allows you to understand where your money is going and identify areas where you can cut back. By keeping a record of every purchase you make, whether it’s a cup of coffee or a monthly subscription, you can pinpoint patterns and habits that might be draining your funds unnecessarily.

Identify Areas To Cut Back

Once you have a clear picture of your expenses, it’s time to identify areas where you can make cuts. Look for non-essential expenditures that you can minimize or eliminate. For example, consider packing your lunch instead of eating out every day or cancelling unused memberships or subscriptions. These small adjustments can add up over time and free up more money to put towards paying off your credit card debt.

Allocate Extra Funds Towards Debt

Now that you have identified areas to cut back, it’s time to allocate the extra funds towards your credit card debt. Create a separate category in your budget specifically for debt repayment. Calculate how much extra money you have available each month and allocate a portion of it towards paying off your credit cards. By prioritizing debt repayment and sticking to this plan, you can accelerate your progress and become debt-free sooner.

Remember, creating a budget is just the first step. To effectively pay off your credit cards faster, you need to stick to your budget consistently. Avoid unnecessary expenses, stay disciplined, and remain focused on your goal of becoming debt-free. With proper planning and dedication, you can regain control of your finances and achieve financial freedom.

3. Increase Your Income

Pay off your credit cards faster and increase your income with these proven tricks. Boost your financial stability and minimize debt by implementing effective strategies that will help you achieve your goals sooner.

One effective way to pay off your credit cards faster is to increase your income. By earning more money, you’ll have more funds to dedicate towards paying down your credit card balances. Here are three strategies you can implement:

Take On Additional Work

If you’re looking for a quick way to boost your income, consider taking on additional work. This could involve picking up extra shifts at your current job, freelancing, or finding part-time employment. By putting in extra hours, you’ll be able to earn more money, which can be used to make larger payments towards your credit cards.

Start A Side Hustle

An alternative option is to start a side hustle. This could involve turning a hobby or passion into a profitable venture. For example, if you’re skilled at crafting, you could sell your handmade items online. Starting a side hustle not only provides an extra income stream but can also be a fulfilling way to explore your interests and talents.

Negotiate A Raise

Don’t underestimate the power of a negotiation. If you believe you deserve a raise at your current job, take the initiative and discuss the possibility with your employer. Prepare a compelling case that highlights your accomplishments, contributions, and the value you bring to the company. Remember, a higher salary means more money you can allocate towards your credit card payments.

Incorporating one or more of these strategies can significantly accelerate your journey towards becoming debt-free. By taking steps to increase your income, you’ll have the financial means to pay off your credit cards faster.

Credit: www.marketwatch.com

4. Use Strategies To Reduce Interest

Reduce the interest on your credit cards and pay them off faster with these effective strategies. By employing smart techniques, you can save money and accelerate your debt repayment journey.

Negotiate Lower Interest Rates

One effective strategy to reduce the interest on your credit cards is to negotiate with your credit card company for lower interest rates. Many people are unaware that this is a possibility, but it can make a significant difference in the amount you end up paying in interest.

You can start by calling your credit card company and asking to speak with a representative who can help you with lowering your interest rate. Be prepared to explain your situation and provide reasons why you believe you deserve a lower rate. Perhaps you have been a loyal customer for many years, or you have consistently made timely payments.

It’s important to note that this strategy may not always be successful, but it’s definitely worth a try. If you are able to negotiate a lower interest rate, it can save you a substantial amount of money over time.

Consolidate Debt

Another strategy to consider when trying to reduce interest on your credit cards is to consolidate your debt. Debt consolidation involves combining multiple credit card balances into one loan or credit line with a lower interest rate.

This can be done through various methods, such as transferring your balances to a new credit card with a lower interest rate or taking out a personal loan to pay off your credit card debts. The goal is to secure a loan or credit line with a lower interest rate than what you are currently paying.

By consolidating your debt, you simplify your financial situation and potentially save money on interest charges. However, it’s crucial to be disciplined and avoid incurring additional debt after consolidating.

Summary

Reducing the interest on your credit cards is an essential step in paying them off faster. Negotiating with your credit card company for lower interest rates and consolidating your debt are two popular strategies that can help you achieve this goal.

If you are successful in negotiating lower interest rates or consolidating your debt, make sure to continue making regular payments and avoid falling into the same debt trap again. With dedication and perseverance, you can become debt-free faster and save money in the long run.

Credit: bowaterecu.org

Frequently Asked Questions Of Tricks To Pay Off Credit Cards Faster

What Are 3 Ways To Pay Off Credit Card Debt Fast?

To pay off credit card debt fast, consider these three strategies:

1. Increase your monthly payments to tackle the debt quicker. 2. Prioritize high-interest cards and pay them off first. 3. Seek a balance transfer card or personal loan with lower interest rates to consolidate and manage the debt efficiently.

How To Pay Off $3 000 In 6 Months?

To pay off $3,000 in 6 months, follow these steps:

1. Create a budget to track your income and expenses. 2. Cut back on unnecessary expenses and save as much as you can. 3. Consider picking up a side hustle to increase your income.

4. Use the extra money to make larger payments towards your debt. 5. Stay committed and remain disciplined to reach your goal within the timeframe.

What’s The Smartest Way To Pay Off A Credit Card?

The smartest way to pay off a credit card is by creating a budget, reducing expenses, and allocating extra funds towards the highest interest rate card first. Make regular payments and consider transferring balances to a card with a lower interest rate if possible.

What Is The Fastest Way To Pay Credit Card Bill?

The fastest way to pay your credit card bill is by making an online payment through your bank’s website or mobile app. Just log in, select your credit card account, and make a one-time payment. This method is quick, convenient, and secure.

Conclusion

Paying off credit card debt can feel like a daunting task, but with the right tricks and strategies, it is possible to achieve financial freedom faster. By implementing these tips such as creating a budget, prioritizing high-interest cards, and considering balance transfers, you can take control of your debt and work towards a debt-free future.

Remember, consistency and discipline are key in this journey towards financial wellness. Start now and watch your debt decrease as you pave the way for a brighter financial future.

To get out of debt with no money, focus on increasing income and reducing expenses. Here’s how you can take control of your finances and improve your financial situation.

Dealing with debt can be overwhelming, especially if you don’t have much money to spare. However, there are strategies you can implement to regain control of your financial situation. The first step is to increase your income by exploring additional sources of revenue.

Consider taking on a side job or freelancing to boost your earnings. Next, reduce your expenses by creating a budget and identifying areas where you can cut back. Prioritize essential expenses and eliminate non-essential ones. Additionally, negotiate with creditors to lower your interest rates or establish a payment plan. By taking proactive steps and making smart financial choices, you can gradually work towards getting out of debt even without a significant amount of money.

Credit: www.warriortrading.com

Evaluate Your Financial Situation

Evaluate your financial situation to find a way out of debt, even if you have no money to start with. Take a close look at your income, expenses, and prioritize debt payments to create a plan that works for you.

Assess Your Debts

Debt Type

Amount Owed

Interest Rate

Credit Card 1

$5,000

15%

Credit Card 2

$3,000

18%

Student Loan

$20,000

5%

Car Loan

$10,000

8%

Before you can effectively tackle your debt, it’s important to evaluate your financial situation. This involves assessing your debts and understanding the amount owed, interest rates, and payment terms. Here’s a breakdown of the debts you may have:

Credit Card 1: You owe $5,000 on this credit card with an interest rate of 15%.

Credit Card 2: Another credit card debt of $3,000 with a higher interest rate of 18%.

Student Loan: If you have a student loan, the amount owed may be substantial. For example, let’s say you owe $20,000 at an interest rate of 5%.

Car Loan: If you have a car loan, it’s crucial to include it in your assessment. Suppose you owe $10,000 at an interest rate of 8%.

Calculate Your Income And Expenses

Once you’ve assessed your debts, the next step is to calculate your income and expenses. Understanding your financial inflows and outflows will help you determine how much money you can allocate towards debt repayment.

Income: Include all sources of income, such as your monthly salary, freelance work, or rental income.

Expenses: Make a detailed list of your essential expenses like rent/mortgage, utilities, groceries, and transportation. Don’t forget to include any recurring payments or subscriptions.

With this information, you can subtract your total expenses from your income to determine your disposable income. This is the amount of money you have available to put towards paying off your debts. Remember, every dollar counts, so even a small surplus can make a difference in your debt repayment journey.

Create A Budget And Stick To It

One of the first steps to getting out of debt when you have no money is to create a budget and, most importantly, stick to it. A budget is a powerful tool that helps you track your income and expenses, allowing you to allocate your money strategically. By creating a budget and committing to it, you can take control of your financial situation and start making progress towards becoming debt-free.

Cutting Expenses

To create a budget, you must first take a close look at your expenses. Identify areas where you can cut back and eliminate unnecessary costs. By reducing your expenses, you can redirect that money towards paying off your debt. Consider these strategies to cut expenses:

Evaluate your monthly subscriptions: Cancel any subscriptions or memberships that you don’t need or use frequently. This can include streaming services, gym memberships, or magazine subscriptions.

Limit eating out: Cooking meals at home can significantly reduce your food expenses. Plan your meals, make grocery lists, and stick to them to avoid impulse buying.

Reduce utility costs: Look for ways to save on electricity, water, and gas. Turn off lights when not in use, use energy-efficient appliances, and implement water-saving techniques.

Shop smart: Before making a purchase, compare prices from different stores or online platforms. Look for sales, discounts, and coupons to get the best deals.

Increasing Income

While cutting expenses is essential for getting out of debt, increasing your income can also accelerate the process. Here are some ways to boost your income:

Take on a part-time job: Consider finding a part-time job or freelancing opportunities to supplement your current income. This additional source of income can be dedicated towards paying off your debt.

Utilize your skills: If you have marketable skills, offer your services on platforms like Fiverr or Upwork. By utilizing your skills, you can earn extra income in your spare time.

Create a side hustle: Turn your hobbies or talents into a profitable side business. Whether it’s selling handmade crafts, offering tutoring services, or starting a small online business, a side hustle can generate extra income.

Rent out unused space: If you have an extra room or a parking space, you can consider renting it out to earn additional income.

By incorporating both expense-cutting and income-increasing strategies into your budget, you can start making a significant dent in your debt. Remember, the key is to stick to your budget consistently while finding ways to save and earn more money. Over time, your dedication and smart financial choices will help you achieve your goal of getting out of debt, even when you initially have little or no money.

Explore Debt Repayment Strategies

In this section, we will explore effective debt repayment strategies that can help you get out of debt, even if you don’t have much money to spare. By understanding these strategies and implementing them wisely, you can take control of your financial situation and work towards a debt-free future.

Prioritize Your Debts

When you are dealing with multiple debts, it is crucial to prioritize and focus on the ones that require immediate attention. By creating a clear picture of your outstanding debts, you can identify which ones are more urgent and need to be addressed first.

One way to do this is by listing your debts in order of interest rates, starting from the highest to the lowest. By tackling the debts with the highest interest rates first, you can minimize the amount of interest accumulating over time and potentially save money in the long run.

Another approach is to prioritize debts based on their sizes. This method involves paying off the smaller debts first and then moving on to the larger ones. By achieving small victories early on, you can build momentum and stay motivated to tackle the larger debts down the line.

Negotiate With Creditors

In some cases, it may be possible to negotiate with your creditors to reduce the amount you owe or renegotiate the terms of your debt repayment. This can be particularly beneficial if you are struggling to meet your financial obligations due to limited funds.

Start by contacting your creditors and explaining your situation. Be honest about your financial limitations and express your willingness to repay the debt. In some cases, creditors may be willing to offer a repayment plan with reduced monthly payments or even a settlement amount lower than your total debt.

Proactively reaching out to your creditors demonstrates your commitment to resolving the debt and can potentially lead to more flexible arrangements. However, it’s important to remember that not all creditors will be open to negotiations, so it’s crucial to be prepared for different outcomes.

By prioritizing your debts and negotiating with creditors, you can begin to take proactive steps towards getting out of debt, even if you have limited financial resources. Remember, every little effort counts, and by staying committed to your goal, you can make significant progress towards achieving financial freedom.

Credit: www.ericwilsonlaw.com

Consider Debt Consolidation Or Settlement

Consider debt consolidation or settlement as a viable option for getting out of debt when you have little to no money. These solutions can help you consolidate your debts into one manageable payment or negotiate lower settlements with your creditors.

If you find yourself overwhelmed by debt and have no money to spare, debt consolidation or settlement may be viable options to consider. These strategies can help you regain control of your finances and pave the way towards a debt-free future. Let’s take a closer look at both options:

Consolidate Your Debts

Debt consolidation involves combining multiple debts into one manageable payment. This can simplify your financial situation by reducing the number of creditors and monthly payments you need to juggle. When you consolidate your debts, you essentially take out a new loan to pay off your existing debts. This allows you to focus on just one monthly payment, making it easier to stay organized and keep on top of your financial obligations.

To consolidate your debts, you can explore a few different options:

Personal Loan: You might qualify for a personal loan from a bank, credit union, or online lender. This loan can be used to pay off your outstanding debts, consolidating them into one loan with a single interest rate and payment plan.

Balance Transfer: If you have credit card debts, you can transfer the balances to a new credit card with a lower interest rate or even a 0% introductory APR. This way, you can save on interest and focus on repaying the consolidated balance.

Home Equity Loan or Line of Credit: If you own a home, you may be able to leverage the equity you have built to secure a loan or line of credit. This can help you consolidate your debts into one manageable payment, typically at a lower interest rate.

It’s important to carefully consider the terms, interest rates, and fees associated with each option. Determine which choice aligns best with your financial circumstances and goals. Debt consolidation can be an effective way to simplify your debt load and potentially save money on interest payments.

Work With A Debt Settlement Company

If your financial situation is dire and you are unable to make payments on your debts, working with a debt settlement company might be a suitable alternative. These companies negotiate with your creditors on your behalf to reach a settlement, typically for a reduced amount. The idea is to pay a lump sum or a series of agreed-upon payments to clear your debt. Debt settlement can help you avoid bankruptcy and provide much-needed debt relief.

When considering a debt settlement company, it’s essential to do thorough research and choose a reputable organization. Look for companies that are accredited and have a track record of successful settlements. Additionally, carefully review any fees associated with their services and ensure they are transparent and reasonable.

Keep in mind that debt settlement can have negative impacts on your credit score, as it involves not paying the full amount owed. However, if you’re already struggling to make payments and facing potential bankruptcy, settling your debts may be the more favorable option.

Be sure to weigh the benefits and drawbacks of debt consolidation and settlement carefully. Consider consulting with a financial advisor or credit counselor to determine which approach is best suited to your specific circumstances. Remember, taking action is the first step towards reclaiming your financial freedom.

Credit: www.credit.com

Frequently Asked Questions Of Getting Out Of Debt With No Money

How Can I Pay Off My Debt If I Have No Money?

To pay off debt with no money, start by creating a budget to track expenses. Cut down on non-essential spending and consider increasing your income through side jobs or selling unused items. Reach out to your creditors to negotiate a payment plan or seek assistance from credit counseling agencies.

Stay committed and disciplined to gradually eliminate your debt.

How Can I Escape My Debt Without Paying?

To escape debt without paying, it is important to take responsibility for your financial obligations. Avoiding payment is not a viable solution and typically leads to legal consequences. Instead, consider options like budgeting, negotiating with creditors, or seeking professional debt counseling to create a plan for repayment and financial freedom.

How Can I Get Rid Of My Debt Without Paying?

The only way to get rid of debt is by paying it off. There are no legal loopholes or shortcuts to avoid paying what you owe. Make a budget, cut expenses, increase income, and put all extra money towards your debt for a quicker payoff.

What Happens If You Can’t Afford To Pay Your Debt?

If you can’t afford to pay your debt, there are several options available. You can negotiate with your creditors for a payment plan or settlement. You can also consider credit counseling or debt consolidation programs. Bankruptcy may be a last resort.

Seek professional advice to find the best solution for your situation.

Conclusion

To sum it up, conquering debt when you’re strapped for cash may seem impossible, but it’s not. By prioritizing your expenses, creating a realistic budget, exploring additional sources of income, and seeking professional guidance, you can successfully navigate your way to financial independence.

Remember, financial freedom is within reach, and with determination and discipline, you can conquer debt and pave the way for a brighter financial future. So, take charge of your finances today and start your journey towards a debt-free life.

To become debt-free, focus on creating a budget and reducing expenses. Achieving financial freedom is a goal for many individuals, and one significant step towards attaining this is to become debt-free.

Debts can accumulate quickly and hinder your ability to live a comfortable and stress-free life. However, by implementing effective strategies, you can work towards eliminating debt and gaining control over your finances. This article will provide essential tips on how to become debt-free, including creating a budget, reducing expenses, and developing a repayment plan.

Incorporating these strategies into your financial management can ultimately lead to a debt-free future and a stronger financial foundation. So, let’s get started on the journey towards financial freedom!

Create A Budget

Creating a budget is a crucial step towards financial stability and becoming debt-free. A budget helps you track your income and expenses, identify areas where you can cut back on spending, and have better control over your financial situation. By analyzing your financial habits and making conscious decisions about your money, you can take charge of your debt and work towards a debt-free future.

Track Your Income And Expenses

Tracking your income and expenses is the foundation of creating a successful budget. Start by making a list or a spreadsheet of all your income sources, such as your salary, side hustle earnings, or any other form of income. Next, gather all your bills, receipts, and financial records to determine your monthly expenses.

To track your expenses effectively, categorize them into essential and non-essential expenditures. Essential expenses include items like rent or mortgage payments, utilities, groceries, and transportation costs. Non-essential expenses are things like entertainment, dining out, or impulse purchases.

Once you have a clear overview of your income and expenses, you can calculate your monthly surplus or deficit. This will give you an idea of how much money you have left after covering your essential expenses and how much you need to cut back in other areas.

Identify Areas To Cut Back On Spending

Identifying areas where you can cut back on spending is an essential step toward becoming debt-free. It may require some honest evaluation and lifestyle adjustments, but it’s worth it in the long run. Take a close look at your non-essential expenses and ask yourself if you can live without certain luxuries or find cheaper alternatives.

To identify areas for potential cutbacks, consider the following strategies:

Evaluate your subscriptions and memberships. Cancel those you don’t use or find cheaper alternatives.

Review your grocery shopping habits. Plan meals, buy in bulk, and avoid unnecessary food waste.

Cut down on entertainment expenses. Look for free or low-cost activities, take advantage of community resources, and limit dining out.

Reduce transportation costs. Explore carpooling, public transportation, or walking/cycling for short distances.

Lower utility bills. Practice energy-saving habits, such as turning off lights when not in use, adjusting thermostat settings, and minimizing water consumption.

Remember that every small cutback adds up and can make a significant difference in your budget. It’s important to stay consistent and disciplined in your spending habits to accelerate your journey towards becoming debt-free.

Credit: www.solution-loans.co.uk

Develop A Repayment Plan

Developing a repayment plan is essential for anyone looking to become debt-free. By strategizing how to distribute payments and prioritize debts, individuals can take control of their finances and make progress towards financial freedom.

Developing a repayment plan is a crucial step towards becoming debt-free. By creating a well-defined strategy, you can effectively manage your debts and work towards eliminating them. Follow these steps to develop a repayment plan that suits your financial situation.

List Your Debts

To begin with, it is essential to make a comprehensive list of all your debts. This includes credit card bills, student loans, personal loans, and any other outstanding amounts you owe. Listing your debts allows you to have a clear overview of your financial obligations and serves as a starting point for developing your repayment plan.

Prioritize And Strategize

Once you have listed your debts, the next step is to prioritize and strategize your repayment plan. Start by categorizing your debts into high-interest and low-interest ones. High-interest debts, such as credit card bills, should be given top priority as they tend to accumulate more interest over time. By allocating more funds towards these debts, you can effectively reduce the overall interest burden.

After prioritizing, consider the repayment strategies you can adopt. Two popular methods include the snowball method and the avalanche method. The snowball method involves paying off the smallest debts first, while the avalanche method focuses on repaying debts with the highest interest rates. Analyze your financial capabilities and choose the strategy that best suits your circumstances.

Consider Debt Consolidation or Refinancing

If you are struggling to manage multiple debts, debt consolidation or refinancing might be worth considering. Debt consolidation involves combining several debts into a single loan, usually with a lower interest rate. This can make your repayments more manageable and simplify the overall debt repayment process.

On the other hand, refinancing involves negotiating with your creditors or finding a new lender to obtain a lower interest rate on your existing loans. This can help reduce your monthly payments and save money in the long run.

In conclusion, developing a repayment plan is a crucial step towards achieving a debt-free life. By listing your debts, prioritizing and strategizing, and considering debt consolidation or refinancing options, you can effectively work towards eliminating your debts and gaining financial freedom. Take control of your finances today and set yourself on the path to becoming debt-free.

Increase Your Income

Discover proven strategies to become debt-free and increase your income. Unlock financial freedom through smart money management and effective debt repayment techniques. Take control of your finances and create a secure future for yourself.

When it comes to getting out of debt, increasing your income can be a game changer. By finding ways to earn more money, you will have extra funds to put towards paying off your debt faster. Here are two strategies to help you increase your income:

Explore Side Hustles

If you’re looking to generate additional income, exploring side hustles is a fantastic option. Side hustles are small jobs or projects that you can take on alongside your regular job. These can include freelance work, selling handmade crafts online, or offering services like tutoring or pet sitting.

Here are some ideas for side hustles to consider:

Side Hustle

Description

E-commerce Store

Set up an online store and sell products that you are passionate about.

Rideshare Driver

Drive for a ridesharing platform and make money in your spare time.

Freelance Writing

Offer your writing skills to businesses or individuals who need content.

Photography

Take up photography as a side gig and sell your photos online or to clients.

By exploring side hustles, you can not only give your income a boost, but also tap into your skills and passions to make extra money.

Request A Raise Or Promotion

If you’ve been working hard and feel that you deserve it, requesting a raise or promotion can be a great way to increase your income. Here are some tips to help you navigate this process:

Research: Familiarize yourself with industry salary standards and gather evidence of your accomplishments to support your case.

Prepare: Schedule a meeting with your supervisor and come prepared with a list of reasons why you deserve a raise or promotion.

Communicate: Clearly articulate your achievements, skills, and contributions to the company during the meeting.

Be flexible: If a raise or promotion isn’t feasible at the moment, consider negotiating for other benefits like additional vacation time or professional development opportunities.

Follow up: Regardless of the outcome, follow up with a thank-you note expressing your appreciation for the opportunity to discuss your progress and goals.

Remember, requesting a raise or promotion requires confidence and a well-prepared approach. Don’t be afraid to advocate for yourself and the value you bring to your organization.

Credit: www.self.inc

Reduce Your Expenses

Reducing your expenses is a key step in becoming debt-free. By lowering your monthly bills and cutting unnecessary costs, you can free up more money to put towards paying off your debts. Let’s explore some strategies for achieving this:

Lower Monthly Bills

Lowering your monthly bills can have a significant impact on your overall expenses. Here are a few ways you can achieve this:

Review your service providers: Consider shopping around for new providers to potentially get better deals on your utilities, internet, cable, or insurance.

Negotiate with your providers: Contact your current service providers and negotiate lower rates or ask for any available discounts.

Bundle your services: Look into bundling your internet, cable, and phone services with the same provider to potentially save on monthly fees.

Cut Unnecessary Costs

Identifying and eliminating unnecessary costs from your budget can lead to significant savings. Here are some areas to consider cutting back on:

Eating out: Instead of dining out frequently, try cooking at home and taking packed lunches to work. This can help you save money on restaurant bills.

Entertainment subscriptions: Assess your streaming and subscription services and unsubscribe from those you rarely use or can do without.

Impulse purchases: Before making a purchase, ask yourself if it is a want or a need. Minimizing impulse buying can help you save money.

Unused memberships: Evaluate any memberships or subscriptions you have and cancel those you no longer use or find alternatives that offer similar benefits at lower costs.

Transportation costs: Consider carpooling, using public transportation, or even cycling to reduce fuel and maintenance expenses.

By reducing your monthly bills and cutting unnecessary costs in these areas, you can make significant progress towards achieving a debt-free future. Take a close look at your expenses, identify areas where you can make changes, and commit to stick to your budget. Every small saving counts and brings you one step closer to financial freedom!

Credit: www.ramseysolutions.com

Frequently Asked Questions Of Ways To Become Debt Free

How Do I Become Completely Debt Free?

To become completely debt-free, follow these steps:

1. Create a budget and stick to it. 2. Cut unnecessary expenses and save money. 3. Pay off high-interest debts first. 4. Consider debt consolidation or negotiating with creditors for lower interest rates.

5. Stay committed and disciplined in paying off debts.

How Long Will It Take To Pay Off $20000 In Credit Card Debt?

It depends on your repayment strategy, but typically, paying off $20,000 in credit card debt may take several years. Making consistent monthly payments and potentially increasing payments can help expedite the process. Consider seeking professional advice to create an effective repayment plan.

How Can I Legally Avoid Paying Debt?

Legally avoiding debt requires proactive financial management. You can negotiate with creditors for a rescheduled payment plan, seek credit counseling, or explore debt consolidation options. Bankruptcy may be a last resort, with potential consequences. Remember, it’s crucial to honor financial obligations and seek professional guidance when necessary.

How To Pay Off $50,000 In Debt?

To pay off $50,000 in debt, follow these steps:

1. Create a budget and cut down on unnecessary expenses. 2. Increase your income by getting a second job or freelancing. 3. Prioritize your debts and make larger payments on high-interest debts.

4. Consider consolidating your debts into a single, lower interest loan. 5. Stay disciplined and stick to your repayment plan.

Conclusion

Becoming debt-free requires commitment, perseverance, and smart financial planning. By implementing the strategies discussed in this blog post, such as creating a budget, cutting expenses, increasing income, and paying off high-interest debts first, you can take control of your financial situation.

Remember, every small step counts, and consistency is key. Stay focused on your goals, and you’ll soon be on your way to a debt-free future. Start your journey to financial freedom today!

For credit card debt, the best options include balance transfer, debt consolidation, negotiation with creditors, and seeking professional help. Are you struggling with credit card debt and looking for the best options to get out of it?

Managing credit card debt can be overwhelming and stressful, but there are several viable solutions to help you regain control of your finances. We will explore the top options that can effectively address your credit card debt concerns. These options include balance transfer, debt consolidation, negotiation with creditors, and seeking professional help.

By taking advantage of these strategies, you can take proactive steps towards becoming debt-free and achieving financial stability. Let’s delve into each option and find the one that best suits your needs.

Credit: www.palisadesfcu.org

1. Credit Card Debt Consolidation

Are you drowning in credit card debt and looking for the best options to get back on track financially? If so, credit card debt consolidation can be an excellent choice. Debt consolidation allows you to combine multiple high-interest credit card balances into one manageable payment, potentially saving you money on interest charges and helping you pay off your debt faster.

1.1 Balance Transfer

A balance transfer is a popular method of credit card debt consolidation. It involves transferring your outstanding balances from high-interest credit cards to a new credit card with a lower interest rate. This option enables you to consolidate your debts into one card, making it easier to keep track of your payments and reducing the amount of interest you pay.

To take advantage of a balance transfer, look for credit cards that offer a low or 0% introductory APR on balance transfers. This way, you can save money on interest charges during the promotional period, allowing you to make significant progress in paying off your debt. However, keep in mind that after the introductory period, the interest rate may increase, so it’s essential to have a plan in place to pay off your balance during this time.

1.2 Personal Loan

Another option for credit card debt consolidation is taking out a personal loan. With a personal loan, you can borrow a lump sum of money to pay off your credit card balances. This allows you to consolidate your debt into one loan, making it easier to manage and potentially lowering your interest rate.

When considering a personal loan for debt consolidation, compare interest rates and loan terms from different lenders to find the best option for your situation. Look for a loan with a reasonable interest rate and monthly payment that fits within your budget. By securing a lower interest rate through a personal loan, you may be able to save money on interest charges and pay off your debt more quickly.

Remember, credit card debt consolidation is not a magic solution, but it can help you simplify your finances, reduce your interest payments, and become debt-free faster. It’s essential to have a solid repayment plan in place and be disciplined with your spending to make the most of these debt consolidation options.

Credit: www.usatoday.com

2. Debt Repayment Strategies

When it comes to paying off your credit card debt, having a well-thought-out repayment strategy is crucial. Implementing the right strategy can help you stay disciplined, manage your debt effectively, and ultimately become debt-free. In this section, we will discuss two popular debt repayment strategies: the Snowball Method and the Avalanche Method.

2.1 Snowball Method

The Snowball Method is a debt repayment strategy that focuses on paying off your smallest debts first. Here’s how it works:

List all your credit card debts from smallest to largest, regardless of interest rates.

Make minimum payments on all your debts every month.

Allocate any extra money you have towards paying off the smallest debt.

Once the smallest debt is paid off, move on to the next smallest debt and repeat the process.

Continue this snowball effect until all your debts are paid off.

The Snowball Method is effective because it provides a sense of accomplishment when you clear your smaller debts. This motivation can keep you focused and motivated to tackle your larger debts. While the Snowball Method may result in paying more interest in the long run, the psychological benefits can make it a worthwhile strategy for many.

2.2 Avalanche Method

The Avalanche Method, on the other hand, prioritizes paying off debts with the highest interest rates first. Here’s how it works:

List all your credit card debts from highest to lowest interest rates.

Make minimum payments on all your debts every month.

Allocate any extra money towards paying off the debt with the highest interest rate.

Once the debt with the highest interest rate is paid off, move on to the next one with the next highest interest rate.

Continue this method until all your debts are paid off.

The Avalanche Method can save you more money on interest payments compared to the Snowball Method. By eliminating debts with higher interest rates first, you reduce the overall interest charges you’ll incur. Although it may take longer to pay off your smaller debts, this method can be financially beneficial in the long run.

3. Credit Counseling

Get the best options for credit card debt with credit counseling. Find expert guidance on managing your finances and improving your credit score, tailored to your specific needs. Say goodbye to debt and hello to financial freedom.

If you find yourself overwhelmed by credit card debt, credit counseling may be a viable option for you. This form of debt relief involves seeking assistance from a qualified credit counselor who can help you develop a plan to manage and eliminate your debt. Through a systematic process of financial assessment and debt management plans, credit counseling can provide you with the guidance you need to regain control of your financial situation.

3.1 Financial Assessment

Before embarking on a debt management plan, a comprehensive financial assessment is conducted by the credit counselor. This assessment helps to determine your current financial situation, including your income, expenses, and debt obligations. The counselor will analyze your financial data to identify areas where you can cut back on expenses and develop a realistic budget to meet your needs. Through this process, the counselor gains a complete understanding of your financial picture, enabling them to provide tailored guidance and recommendations.

During the financial assessment, it’s important to be completely transparent and provide accurate information about your finances. This will ensure that the credit counselor has all the necessary details to create an effective debt management plan.

3.2 Debt Management Plan

A debt management plan is a key component of credit counseling. It is a personalized strategy developed by the credit counselor to help you pay off your credit card debt in a manageable and efficient manner. This plan typically involves negotiating with your creditors to reduce interest rates, eliminate late fees, and create a structured repayment schedule that aligns with your budget.

One of the primary benefits of a debt management plan is that it consolidates your monthly payments into a single payment. This simplifies your financial obligations and makes it easier to stay on top of your debts. Moreover, with the guidance of a credit counselor, you can learn effective money management skills that will help you avoid future debt problems.

It’s important to note that a debt management plan requires discipline and commitment to stick to the agreed-upon payment schedule. By adhering to the plan, you can gradually reduce your credit card debt, improve your credit score, and ultimately achieve financial freedom.

In conclusion, credit counseling offers an effective way to tackle credit card debt. Through a thorough financial assessment and the development of a debt management plan, you can regain control of your finances and work towards a debt-free future. By partnering with a reputable credit counseling agency, you can receive the guidance and support needed to navigate the complexities of debt relief.

4. Bankruptcy As A Last Resort

While exploring options to deal with your credit card debt, bankruptcy should always be considered as a last resort. It is important to exhaust all other alternatives before turning to this drastic measure. Bankruptcy can have serious long-term consequences on your credit score and financial future. However, in certain cases, it can provide a fresh start and relief from overwhelming debt. If you have reached a point where bankruptcy seems inevitable, it is crucial to understand the different types available and the potential impact they may have on your situation.

4.1 Chapter 7 Bankruptcy

Chapter 7 bankruptcy, also referred to as “liquidation bankruptcy,” is the most common type of bankruptcy filed by individuals. This option aims to give debtors a clean slate by liquidating their non-exempt assets to pay off their creditors. With Chapter 7, you may be able to eliminate most, if not all, of your unsecured debts like credit card debt, medical bills, and personal loans.

Here are a few key points to consider:

Chapter 7 bankruptcy is typically a quicker process, often lasting around three to six months.

It may be subject to a means test to determine if you qualify based on your income.

You may be able to keep certain assets, known as exempt assets, such as necessary clothing and household items.

Non-exempt assets, including valuable property and luxury items, may be sold to repay creditors.

4.2 Chapter 13 Bankruptcy

Chapter 13 bankruptcy, also known as “reorganization bankruptcy,” offers an alternative solution for individuals who have a regular income and want to repay their debts over time. Unlike Chapter 7, Chapter 13 does not involve liquidating assets. Instead, it allows debtors to create a repayment plan to pay back their creditors over a specific period, usually between three and five years.

Consider the following aspects of Chapter 13 bankruptcy:

Chapter 13 bankruptcy requires you to have a steady income to develop a debt repayment plan.

Your repayment plan will be based on your disposable income, considering your reasonable living expenses.

While it may take longer than Chapter 7 bankruptcy, Chapter 13 allows you to retain your assets and catch up on missed mortgage or car payments.

Once you complete your repayment plan, any remaining eligible debts are typically discharged.

It’s worth noting that bankruptcy laws vary by country and state. Consulting with an experienced bankruptcy attorney can help you navigate the complexities of the legal process and determine the best course of action for your specific situation.

Credit: www.foxbusiness.com

Frequently Asked Questions On Best Options For Credit Card Debt

What Is The Most Effective Way To Manage Credit Card Debt?

To effectively manage credit card debt, create a detailed budget, prioritize high-interest debts, and make regular payments. Cut unnecessary expenses and consider consolidation or balance transfer options. Communication with creditors is key, so negotiate lower interest rates or ask for a payment plan to reduce your debt.

Which Option Makes It Easier To Get Out Of Credit Card Debt?

Paying off high-interest credit card debt.

How Do I Get Rid Of $30 K In Credit Card Debt?

To eliminate $30K in credit card debt, consider these steps:

1. Create a budget to track expenses and prioritize debt payments. 2. Cut down on non-essential spending to free up extra funds. 3. Negotiate with credit card companies for lower interest rates or payment plans.

4. Explore debt consolidation options like personal loans or balance transfers. 5. Consider credit counseling or debt settlement programs if necessary. Stay determined and consistent in your efforts to become debt-free.

Does Consolidating Debt Hurt Your Credit?

Consolidating debt can initially impact your credit, but in the long run, it may actually improve it. This is because it shows that you’re taking steps to manage your debt responsibly. However, it’s crucial to make your payments on time and avoid taking on new debt to maintain a positive credit score.

Conclusion

To effectively manage credit card debt, it’s crucial to explore the best options available. By considering strategies such as balance transfers, debt consolidation loans, and professional debt counseling, individuals can regain control over their finances. It’s important to remember that each option has its own pros and cons, so careful evaluation and planning are essential.

Ultimately, taking proactive steps towards reducing credit card debt will lead to financial stability and peace of mind.