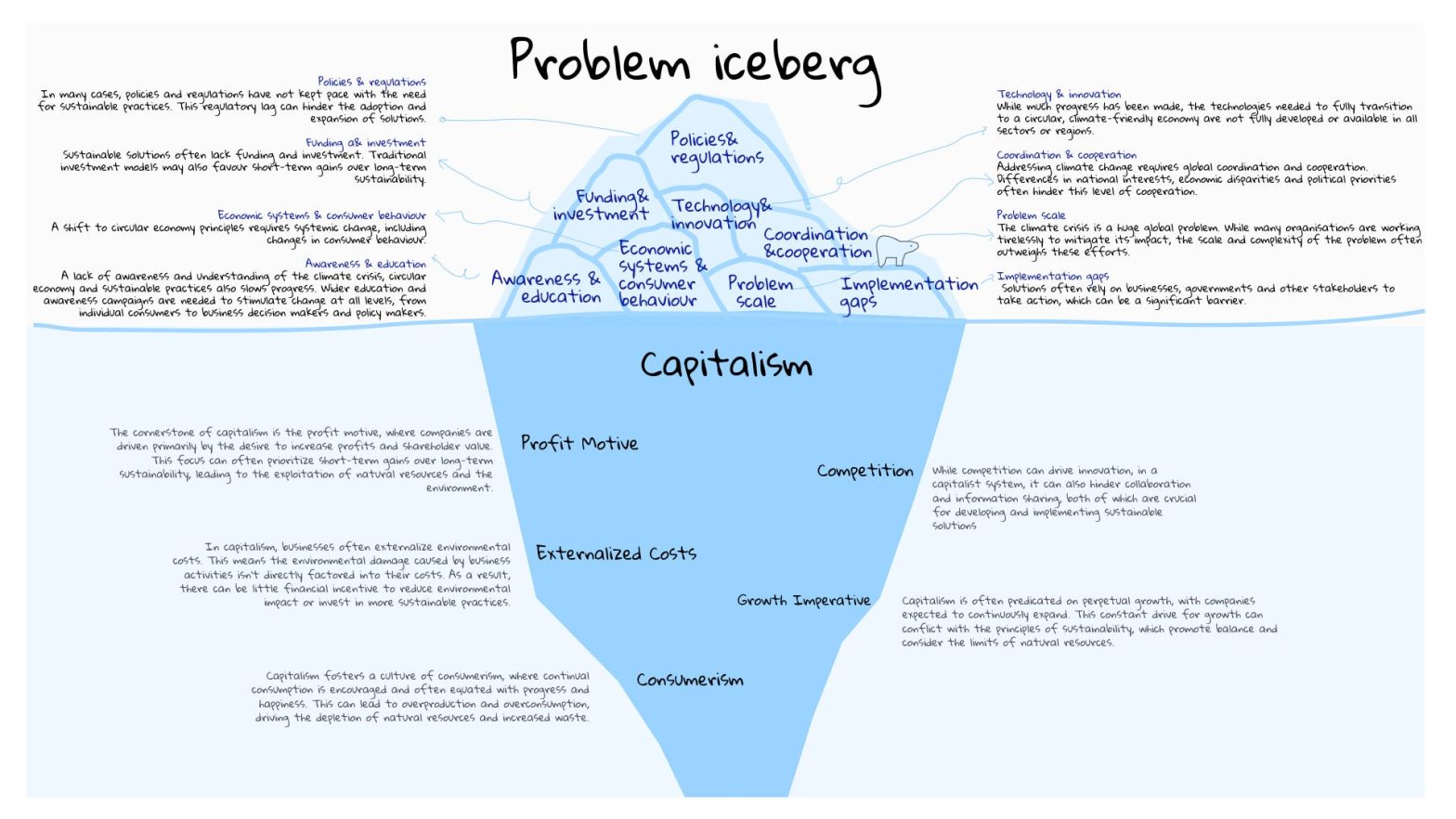

Growth is a fundamental aspect of life, and it is no different when it comes to businesses and economies. Over the years, various theories have been developed to understand the factors and patterns that contribute to growth. In this article, we will explore some of the most prominent theories of growth.

Table of Contents

1. Classical Growth Theory

The classical growth theory, developed by economists such as Adam Smith and David Ricardo, focuses on the role of capital and labor in driving economic growth. According to this theory, increased investment in capital assets, such as machinery and technology, combined with a growing labor force, leads to economic expansion.

This theory emphasizes the importance of free market mechanisms and the productive capacity of an economy. It suggests that economic growth can be achieved through policies that promote private property rights, free trade, and limited government intervention.

Credit: www.amazon.com

2. Neoclassical Growth Theory

Building upon the classical growth theory, the neoclassical growth theory introduces the concept of technological progress as a crucial driver of economic growth. It argues that advancements in technology improve productivity, leading to increased output.

This theory emphasizes the role of innovation and research and development (R&D) activities in fostering economic growth. It suggests that policies aimed at promoting innovation and creating favorable conditions for technological advancements can contribute to sustained economic expansion.

3. Endogenous Growth Theory

The endogenous growth theory, developed by economists such as Robert Solow and Paul Romer, challenges the assumption of diminishing returns to capital and suggests that knowledge and human capital are not subject to such limitations.

According to this theory, investments in education, research, and human capital development can lead to increasing returns, thereby driving long-term economic growth. It highlights the importance of investing in intellectual capital and promoting education and skills development to foster economic progress.

4. New Growth Theory

The new growth theory, put forth by economist Paul Romer, expands on the endogenous growth theory by incorporating elements of technological change and innovation. It argues that technological advancements are not purely exogenous but can be influenced by a nation’s policies and institutions.

This theory suggests that pro-innovation policies, such as intellectual property protection, government support for R&D, and investments in infrastructure, can promote technological progress and economic growth. It emphasizes the role of ideas and knowledge creation as key drivers of long-term economic expansion.

5. Productivity Growth Theory

The productivity growth theory focuses on the relationship between productivity and economic growth. It suggests that improvements in productivity, which can be achieved through technological advancements, efficient resource allocation, and organizational changes, are crucial for sustained economic expansion.

This theory emphasizes the need for policies that enhance productivity, such as investments in human capital, infrastructure development, and fostering a business-friendly environment. It highlights the role of efficiency and effectiveness in driving economic growth.

Credit: www.amazon.com

Conclusion

Understanding the theories of growth can provide valuable insights into the factors and strategies that contribute to economic expansion. These theories highlight the role of capital, labor, technology, knowledge, and productivity in driving growth.

While each theory presents a unique perspective, they all emphasize the importance of policies and investments that facilitate innovation, enhance human capital, and create an enabling environment for businesses to thrive. By incorporating these theories into policymaking and business strategies, we can foster sustained economic growth and prosperity for individuals and societies.

Leave a Reply