Sovereign Risk: Understanding the Impact on Global Economy

When it comes to international finance and investment, one key factor that cannot be ignored is sovereign risk. This term refers to the risk associated with lending to governments or investing in their debt. A government’s ability to repay its creditors or meet its financial obligations is crucial in determining sovereign risk. In this article, we will delve into the concept of sovereign risk, its impact on the global economy, and the methods used to measure and mitigate this risk.

Credit: bscdesigner.com

Defining Sovereign Risk

Sovereign risk emerges from a variety of factors, including a nation’s economic stability, political climate, institutional framework, and its level of indebtedness. It refers to the chances of a government defaulting on its debts or being unable to meet its financial obligations. The implications of sovereign risk are manifold and can have far-reaching consequences for domestic and international financial markets, investors, and creditors.

Impact On Global Economy

The global economy is inherently interconnected, with the financial well-being of one nation significantly impacting others. Sovereign risk can trigger financial crises, leading to a domino effect that spreads across countries and regions. It has the potential to disrupt capital flows, cause currency volatility, increase borrowing costs, and trigger recessions. In extreme cases, sovereign risk can even lead to a sovereign debt crisis, where a government is unable to repay its creditors and defaults on its debt.

The aftermath of the 2008 global financial crisis demonstrated the far-reaching consequences of sovereign risk. Several nations faced severe financial strain due to excessive government borrowing and mounting debt levels. Countries like Greece, Spain, and Portugal experienced significant economic downturns, with high unemployment rates, austerity measures, and social unrest. The contagion effect of sovereign risk led to a widespread economic slowdown and turmoil in financial markets.

Measuring Sovereign Risk

As sovereign risk plays a crucial role in financial decision-making and risk assessment, several tools and methods have been developed to measure and evaluate this risk. These measurements help investors, credit rating agencies, and policymakers analyze the creditworthiness and financial stability of nations.

Credit Ratings

Credit rating agencies, such as Standard & Poor’s, Moody’s, and Fitch Ratings, assess the credit quality of countries by assigning them ratings. These ratings provide an indication of a government’s ability to meet its financial obligations. Typically, higher-rated countries are considered less risky, while lower-rated nations face greater sovereign risk. Investors rely on these ratings to make informed decisions regarding their investments.

Rating

Definition

AAA

Highest credit quality

AA

High credit quality

A

Upper-medium credit quality

BBB

Lower-medium credit quality

BB

Speculative (high) credit risk

B

Speculative (very high) credit risk

Market-based Measures

Market-based measures, such as sovereign bond yields and credit default swaps (CDS), provide real-time information about the perceived riskiness of government debt. Higher yields and CDS spreads indicate higher levels of sovereign risk. These measures are essential for understanding market sentiment and for investors to gauge market appetite for a nation’s debt.

Mitigating Sovereign Risk

Given the potential consequences of sovereign risk on the global economy, it is vital for governments and policymakers to take measures to mitigate this risk. Some potential strategies and steps include:

Improving fiscal discipline: Governments should strive to maintain sound financial practices, avoid excessive borrowing, and control budget deficits.

Implementing structural reforms: Enhancing market competition, promoting transparency, and fostering good governance can contribute to reducing sovereign risk.

Diversifying funding sources: Governments should explore ways to diversify their sources of funding, such as attracting foreign direct investment or utilizing multilateral financing options.

Monitoring macroeconomic indicators: Timely monitoring and addressing signs of economic vulnerability, including inflation rates, exchange rates, and debt-to-GDP ratios, can help prevent sovereign risk from escalating.

Seeking international cooperation: Global coordination and cooperation, such as through international financial institutions like the International Monetary Fund (IMF), can play a vital role in assisting nations during times of financial stress.

Credit: www.investopedia.com

Conclusion

Sovereign risk is an essential aspect of international finance with significant implications for global economic stability. Understanding and effectively managing this risk is crucial for investors, financial institutions, and governments alike. By employing various measures and strategies to measure and mitigate sovereign risk, economies can strive towards greater financial stability and minimize the potential negative impacts that this risk poses.

Real estate development faces challenges such as financing, market volatility, regulatory hurdles, and construction delays, among others. These challenges can result in project delays, disputes, and increased costs, impacting the overall feasibility and profitability of real estate ventures.

An understanding of these challenges and effective strategies to mitigate risks are crucial for successful real estate development. Real estate development is a complex and multifaceted field that involves various challenges. From securing financing to navigating regulatory hurdles, real estate developers need to address numerous obstacles throughout the development process.

This article explores the key challenges faced by real estate developers and the importance of overcoming them. By understanding these challenges and implementing effective strategies, developers can enhance their chances of success in the competitive real estate industry. So, let’s delve into the challenges that real estate development entails and how they can be mitigated to ensure smooth project execution and improved profitability.

1. Limited Land Availability

A major challenge in real estate development is the limited availability of land, which can hinder the construction and expansion of properties. The scarcity of land presents obstacles for developers as they strive to meet growing demand in a competitive market.

Demand For Land

The real estate development industry faces many challenges, and one of the most significant is the limited availability of land. As the global population continues to grow, the demand for land for various purposes, including residential, commercial, and industrial development, has also increased.

This high demand for land has resulted in fierce competition among developers, driving up land prices and making it difficult for smaller players to enter the market. Limited land availability has also led to the development of land in less desirable locations, such as remote or environmentally sensitive areas.

This challenge is further exacerbated in urban areas, where the demand for prime land is particularly high due to the increasing population density. As cities expand, suitable land becomes scarcer, forcing developers to think creatively and adapt their strategies to make the most of the available space.

Urban Sprawl

Urban sprawl is another challenge associated with limited land availability in real estate development. This term refers to the uncontrolled and unplanned expansion of urban areas into surrounding rural or undeveloped land.

As cities grow, there is a natural tendency for development to spread outward, resulting in the consumption of more land. The consequences of urban sprawl can be detrimental to both the environment and the overall livability of an area.

Increased traffic congestion, longer commuting times, and the loss of natural habitats are just a few examples of the negative impacts of urban sprawl. Additionally, the reliance on personal vehicles in sprawling cities contributes to higher carbon emissions and air pollution levels.

Addressing the challenges of limited land availability and urban sprawl requires innovative urban planning and sustainable development practices. This includes maximizing land use efficiency, promoting mixed-use developments, and prioritizing transportation infrastructure to reduce dependency on private cars.

2. Financing And Investment

Real estate development is a complex process that involves various challenges. One of the significant hurdles faced by developers is financing and investment. The availability of capital and market fluctuations play a crucial role in determining the success of a real estate project. Let’s delve into some of the challenges associated with financing and investment in real estate development.

Capital Intensive

Real estate development is known for being capital-intensive, requiring significant financial resources for land acquisition, construction, marketing, and other related expenses. The sheer scale of investment involved makes it necessary for developers to secure financing from various sources to fund their projects. Whether it’s through personal equity, bank loans, or partnering with investors, developers must explore multiple avenues to obtain the required capital.

Here are some key aspects to consider when it comes to the capital-intensive nature of real estate development:

The acquisition cost of land constitutes a substantial part of the project’s budget.

Construction costs include materials, labor, permits, and architectural and engineering fees.

Marketing and advertising expenses are crucial for promoting the project and attracting potential buyers or tenants.

Legal and administrative costs, including permits and licenses, must also be taken into account.

Capital Intensive Considerations

Land Acquisition

The cost of acquiring land can be significant and requires careful financial planning.

Construction Costs

Construction expenses encompass various aspects, including labor, materials, permits, and fees.

Marketing & Advertising

Effective marketing strategies are essential to attract potential buyers or tenants.

Legal & Administrative

Complying with legal requirements and obtaining necessary licenses are additional financial considerations.

Market Fluctuations

Market fluctuations are a constant challenge in real estate development. The industry is subject to economic conditions, interest rates, and supply and demand dynamics that can significantly affect property values and investment returns. Developers need to assess market trends and determine the best time to initiate and complete their projects.

Here are a few important points to understand regarding market fluctuations:

Real estate values can be influenced by factors such as economic recessions, inflation, and industry-specific changes.

Supply and demand imbalances can lead to overbuilding or a shortage of properties, impacting rental rates and property prices.

Market fluctuations require real estate developers to adopt a flexible approach and make informed decisions to mitigate risks and maximize returns on their investments.

In summary, the challenges of financing and investment in real estate development stem from the capital-intensive nature of the industry and the volatility of market conditions. Developers must carefully manage financial resources, anticipate market fluctuations, and adapt their strategies to achieve success in this dynamic sector.

3. Regulatory And Legal Constraints

In real estate development, regulatory and legal constraints play a crucial role in determining the success or failure of a project. While these constraints aim to protect the interests of various stakeholders, they can also present significant challenges throughout the development process. This article will explore three key areas in which regulatory and legal constraints can impact real estate development: zoning regulations and the permitting process.

Zoning Regulations

Zoning regulations are an integral part of urban planning, helping to guide the development of land and ensure that it is used in a way that is consistent with the surrounding area. These regulations dictate how a property can be used, the density of development allowed, and any additional requirements such as setbacks or building heights.

Property use restrictions: Zoning regulations determine whether a property can be used for residential, commercial, or industrial purposes, limiting the flexibility of developers in determining the most profitable use for their land.

Density restrictions: Zoning regulations often limit the number of units or amount of floor space that can be built on a property, which can impact the financial viability of a development project.

Setback requirements: These regulations mandate the distance that a building must be set back from property lines or neighboring structures, affecting the design and layout of a project.

Height limitations: Zoning regulations can impose restrictions on the maximum height of buildings, which can impact the overall scale and density of a development.

Permitting Process

The permitting process is another major challenge in real estate development, requiring developers to navigate complex and often time-consuming procedures to obtain the necessary approvals and permits.

Multiple levels of approval: Obtaining permits typically involves navigating various levels of government, including local, regional, and state authorities. Each of these levels has their own set of requirements, timelines, and fees.

Uncertain timelines: Delays in the permitting process can significantly impact project schedules and budgets, making it challenging for developers to meet their timelines and deliver projects on time.

Regulatory compliance: Developers must ensure that their projects comply with all applicable regulations, including building codes, environmental standards, and accessibility requirements.

Public hearings and community input: In some cases, development projects may require public hearings or community input, leading to potential delays and opposition from local residents.

4. Environmental Impact

One of the significant challenges in real estate development is the environmental impact it has. As society becomes more conscious about sustainable living and conservation, real estate developers need to navigate these concerns to ensure their projects align with environmental goals.

Sustainability

Incorporating sustainable practices into real estate development is crucial for minimizing the negative impact on the environment. This includes using eco-friendly building materials, adopting energy-efficient designs, and implementing renewable energy solutions. By considering sustainability from the initial planning stages, developers can create buildings that are not only environmentally friendly but also appeal to conscious buyers and tenants.

Conservation

Conservation is another important aspect to address in real estate development. It involves protecting and preserving natural resources such as water sources, forests, and wildlife habitats. Developers can incorporate measures to reduce water consumption through efficient plumbing fixtures and landscaping choices that require less water. They can also work with environmental experts to ensure any development does not disrupt or degrade fragile ecosystems.

To minimize deforestation, developers can explore options like timber certification or using recycled materials. Additionally, implementing green spaces and planting trees not only enhances the aesthetic appeal of a project but also contributes to air quality improvement and provides habitats for birds and other wildlife.

Furthermore, encouraging sustainable transportation options by incorporating bike lanes, electric vehicle charging stations, and creating pedestrian-friendly environments can help reduce carbon emissions and promote eco-friendly mobility.

All these conservation efforts not only contribute to preserving the environment but also enhance the desirability and long-term value of the real estate development.

5. Community Opposition

5. Community Opposition

Nimbyism

NIMBYism, or Not In My Backyard syndrome, refers to the local opposition to new development projects within a community. This resistance stems from concerns over potential negative impacts such as increased traffic, changes in neighborhood character, and strain on local infrastructure. It can often lead to delays or even cancellations of real estate development plans.

Public Resistance

Public resistance can arise from various factors such as lack of transparency during the planning process, fear of displacement, or environmental concerns. When communities feel that their concerns are not adequately addressed, it can lead to widespread opposition, protests, and legal challenges, further impeding real estate development projects.

Frequently Asked Questions Of What Are Some Challenges Real Estate Development?

What Are The Challenges Of Being A Real Estate Developer?

The challenges of being a real estate developer include securing financing, zoning and regulatory hurdles, market unpredictability, competition, and managing construction.

What Is The Biggest Challenge In Real Estate?

The biggest challenge in real estate is the unpredictable market fluctuations that can affect property values and demand.

Is Real Estate Development Hard?

Real estate development can be challenging but rewarding. It requires strategic planning, market analysis, and project management skills.

Conclusion

The dynamic real estate development industry presents various challenges for developers to navigate. From land acquisition and zoning regulations to environmental concerns and changing market trends, the path to successful development is complex. However, with strategic planning, market research, and innovative solutions, these challenges can be overcome, leading to successful and sustainable real estate projects.

Understanding the Red-Herring Prospectus in the Financial Market

In the world of finance, the term “Red-Herring Prospectus” often surfaces in the context of initial public offerings (IPOs). This document plays a significant role in the process of offering securities to the public. Understanding the intricacies of a Red-Herring Prospectus is essential for both investors and companies looking to go public.

Credit: www.yumpu.com

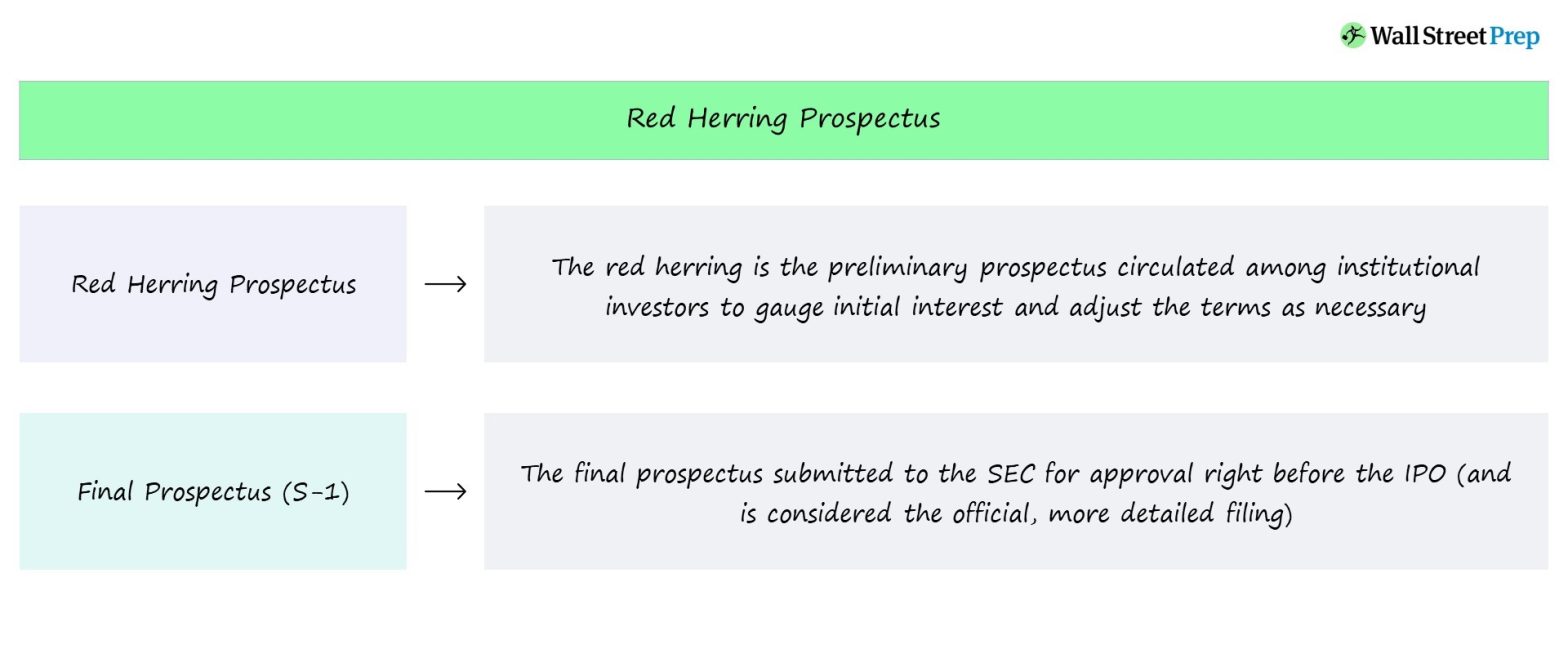

What is a Red-Herring Prospectus?

A Red-Herring Prospectus, also known as a preliminary prospectus, is a document filed with the Securities and Exchange Commission (SEC) by a company that intends to issue securities through an IPO. This document provides essential information to potential investors about the company, its business operations, financial performance, and the securities being offered.

One unique aspect of the Red-Herring Prospectus is that it does not include the offering price or the number of shares being offered. Hence, the term “Red-Herring” emphasizes that the document is not complete and is subject to further details, which are omitted intentionally at the time of the initial filing.

Key Components of a Red-Herring Prospectus

To provide a comprehensive view, a Red-Herring Prospectus typically includes various sections such as:

Company Overview

Business Operations and Strategy

Financial Performance and Projections

Risk Factors

Management and Directors

Corporate Governance

Legal and Regulatory Information

Use of Proceeds from the Offering

Underwriting Information

Other Pertinent Details

These sections aim to provide potential investors with a holistic understanding of the company’s background, the industry in which it operates, its competitive landscape, and the associated risks and opportunities.

Importance of the Red-Herring Prospectus

For investors, the Red-Herring Prospectus serves as a valuable source of information to evaluate the investment opportunity. By reviewing the details presented in the document, investors can make informed decisions about whether to participate in the IPO and at what price.

From the company’s perspective, the Red-Herring Prospectus acts as a marketing tool to generate interest and attract potential investors. It allows the company to present its business model, growth prospects, and financial position in a transparent manner, thereby building credibility among the investing community.

The Process of Finalizing the Prospectus

After the initial filing of the Red-Herring Prospectus, the company and its underwriters engage in a roadshow to promote the upcoming offering to institutional investors. During this period, known as the “waiting period,” the SEC conducts a thorough review to ensure compliance with disclosure requirements.

Following the SEC’s review and any necessary amendments, the final offering price and the number of shares offered are determined and included in the document. At this stage, the Red-Herring Prospectus is no longer “red-herring” and becomes the final prospectus, ready for distribution to potential investors.

Credit: www.futuhk.com

Frequently Asked Questions Of What Is A Red-herring Prospectus?

What Is A Red-herring Prospectus?

A red-herring prospectus is a preliminary document filed by a company before an IPO, providing essential information about the company’s offerings, risks, and financials.

How Is A Red-herring Prospectus Different From A Prospectus?

A red-herring prospectus is a preliminary document, while a prospectus is the final version that includes the offer price and the opening and closing dates of the IPO.

Why Is It Called A Red-herring Prospectus?

The term “red-herring” refers to a decoy or distraction. In the context of an IPO, it conveys that the document does not contain the final offer price or date, serving as a precaution to prevent potential investors from making uninformed decisions.

Conclusion

In the realm of capital markets, the Red-Herring Prospectus plays a pivotal role in the IPO process, providing critical information to both investors and companies. It serves as a bridge between the company seeking to go public and the investing public, facilitating transparency and informed decision-making.

Understanding the contents and significance of the Red-Herring Prospectus is fundamental for anyone involved in the financial markets, facilitating the efficient allocation of capital and contributing to the overall functioning of the economy.

Actuarial science is an exciting and rapidly growing field that combines mathematics, statistics, and business to assess and manage financial risks. While this profession may not be as well-known as others, it plays a vital role in industries such as insurance, finance, and consulting. In this comprehensive guide, we will explore what actuarial science is, the skills required, and the career prospects it offers.

What is Actuarial Science?

Actuarial science is the discipline of using mathematical and statistical methods to analyze financial uncertainties and assess their potential impact. Actuaries use their expertise to provide informed insights and develop strategies to mitigate risks for various organizations. They analyze data, perform complex calculations, and create models to predict future outcomes, especially when it comes to insurance and pension plans.

Skills Required for Actuarial Science

Actuarial science requires a strong foundation in mathematics and statistics. Actuaries must also possess exceptional analytical and problem-solving skills. Additionally, effective communication and business acumen are essential, as actuaries often have to explain complex concepts to non-technical stakeholders. Here are some key skills required:

Advanced mathematical and statistical knowledge

Strong analytical thinking and problem-solving abilities

Excellent communication and interpersonal skills

Attention to detail and ability to work with complex data

Proficiency in programming languages such as R, Python, or SAS

Credit: resumaker.ai

Actuarial Science Exams

Becoming an actuary involves passing a series of rigorous exams. These exams are conducted by professional actuarial organizations and are globally recognized. The number of exams can vary based on the level of specialization and the requirements of the actuarial society in a specific country. The exams cover various areas such as mathematics, finance, statistics, and insurance. The exams are typically challenging, requiring extensive preparation and dedication.

Career Prospects

Actuarial science offers a wide range of career opportunities, both in the public and private sectors. Here are some of the common career paths for actuaries:

Career Path

Description

Insurance Actuary

Assessing and managing risks related to insurance policies, determining premium rates, and estimating potential liabilities.

Pension Actuary

Evaluating retirement plans, calculating pension benefits, and ensuring their long-term sustainability.

Consulting Actuary

Providing actuarial expertise to various clients, advising on risk management strategies and financial planning.

Investment Actuary

Performing financial analyses, forecasting investment outcomes, and assisting in portfolio management decisions.

Actuaries are in high demand due to their unique skill set, which integrates mathematical expertise with business acumen. They play a crucial role in helping organizations make informed decisions and manage potential risks effectively.

Credit: www.amazon.com

Conclusion

Actuarial science is an intriguing field that combines mathematics, statistics, and business to analyze and manage financial risks. Actuaries are highly skilled professionals who play a vital role in guiding companies and organizations in making informed decisions. With great career prospects and the opportunity to work in diverse industries, actuarial science presents an exciting path for those with a passion for numbers and a knack for problem-solving.

Product Life Cycle Management (PLM) is the process of managing a product from its inception to its decline and removal from the market. This process includes different stages such as introduction, growth, maturity, and decline, where companies strategically manage the product’s development, marketing, and sales to maximize profitability and consumer satisfaction.

By effectively managing a product’s life cycle, companies can stay competitive, adapt to market changes, and make informed decisions about product updates, upgrades, or discontinuation.

Stages Of Product Life Cycle

The stages of product life cycle are crucial in effective product life cycle management. From introduction to growth, maturity, and decline, understanding these stages helps businesses strategize and adapt their products to meet market demands while maximizing profitability.

Introduction

Understanding the stages of product life cycle is essential for businesses to effectively manage their products. It provides insights into the various stages a product goes through, from its development to its eventual decline. Each stage presents unique opportunities and challenges that businesses must adapt to in order to maximize their product’s success.

Development

The development stage marks the early phase of a product’s life cycle. It involves research, idea generation, and product design. During this stage, businesses invest in market research to identify potential customer needs and preferences. They then develop prototypes and conduct rigorous testing to ensure the product meets quality standards and effectively addresses those customer needs.

The development stage requires close collaboration between different departments, such as product design, engineering, and marketing, to ensure a cohesive and viable product is created. It is crucial for businesses to carefully manage resources and timelines during this stage to stay on track and meet launch deadlines.

Growth

As the product gains market acceptance, it enters the growth stage. This is a period of rapid sales and increasing profitability. During this stage, businesses focus on expanding their customer base and capturing a larger market share.

Marketing efforts during the growth stage are centered around building brand awareness, increasing distribution channels, and improving customer satisfaction. Businesses may also invest in product enhancements and new features to differentiate their offering from competitors and maintain their growth momentum.

Maturity

The maturity stage is characterized by a stable market and saturation of the product. During this stage, competition intensifies, and businesses may experience a slowdown in sales growth. However, the product continues to generate consistent revenue and maintain a loyal customer base.

At this stage, businesses focus on retaining their market share and maximizing profitability. They may adjust their marketing strategies to emphasize product differentiation, customer loyalty programs, or targeted promotions. Cost management and efficiency become key considerations to maintain competitiveness in a saturated market.

Decline

The decline stage is the final phase of the product life cycle, where sales and profits steadily decline. This decline may be due to changes in consumer preferences, technological advancements, or the emergence of new products in the market.

During the decline stage, businesses must carefully evaluate the profitability and feasibility of continuing to produce the product. They may decide to discontinue the product or explore strategies to extend its life cycle, such as entering new markets or making product modifications.

Understanding and effectively managing each stage of the product life cycle is crucial for businesses to make informed decisions and achieve long-term success. By adapting their strategies to the unique challenges and opportunities presented in each stage, businesses can optimize their product’s performance and maintain a competitive edge.

Frequently Asked Questions For Product Life Cycle Management

What Does A Product Life Cycle Manager Do?

A product life cycle manager oversees the different stages of a product’s lifespan, from development to retirement. They ensure smooth execution of each phase, including market research, product launch, and post-launch analysis. Their goal is to maximize profits and extend the product’s life in the market.

What Is The Role Of A Plm Manager?

A PLM manager oversees product lifecycle management, including planning, development, and execution. They ensure efficient collaboration and data management.

What Is The Life Cycle Of A Product Manager?

A product manager’s life cycle includes identifying opportunities, defining product strategy, collaborating with teams, launching and promoting the product, and continuously iterating and improving it based on user feedback.

Conclusion

Effective product life cycle management is crucial for businesses to stay competitive and relevant in the market. By understanding the different stages of a product’s life cycle and implementing appropriate strategies, companies can maximize profitability and minimize risks. It’s imperative to adapt to the dynamic market and consumer needs to ensure long-term success.

Agency costs are the expenses incurred when one party (known as the principal) hires another party (known as the agent) to represent their interests in a business transaction or a decision-making process. These costs arise due to potential conflicts of interest between the principal and the agent, leading to inefficient outcomes or suboptimal decision-making.

Types of Agency Costs

There are several types of agency costs that can arise in different scenarios:

Agency Cost Type

Description

Monitoring Costs

The expenses incurred by the principal to ensure that the agent is acting in their best interest. This can include regular audits, performance evaluations, or other supervisory activities.

Bonding Costs

The costs associated with creating an agreement or contract to align the interests of the principal and agent. This could involve legal fees, drafting and reviewing contracts, or implementing performance incentives.

Residual Loss

The loss that occurs when the agent acts in their own self-interest, disregarding the interests of the principal. This can result in missed opportunities, inefficient decision-making, or even fraudulent activities.

Conflict of Interest

The costs associated with situations where the agent’s personal interests conflict with the best interests of the principal. These costs can arise when the agent takes actions that are not aligned with the goals of the principal, potentially leading to financial losses or damage to reputation.

Reducing Agency Costs

While agency costs cannot be completely eliminated, there are strategies that can help minimize their impact:

Effective Monitoring: Regular monitoring and performance evaluations can help ensure that the agent is acting in the principal’s best interest.

Strong Communication: Open and transparent communication between the principal and agent can foster trust and alignment of goals.

Incentive Alignment: Implementing performance-based incentives can motivate the agent to act in the best interest of the principal.

Contracts and Agreements: Carefully drafted contracts that clearly outline the responsibilities and obligations of both parties can help mitigate potential conflicts.

Competitive Selection: Choosing agents with a proven track record and reputation for acting in the best interest of their clients can reduce the risk of agency costs.

Credit: www.fleetio.com

Real-World Examples

Agency costs are prevalent in various sectors and industries. Here are a few examples:

1. Corporate Governance: In publicly-traded companies, agency costs can arise when the management team (agents) prioritize their own interests over shareholders’ (principals’) interests. This can result in excessive executive compensations or poor strategic decisions.

2. Financial Services: Agency costs can be significant in the financial services industry. For example, financial advisors may recommend certain financial products that benefit them through commissions, but may not be the best option for the client.

3. Real Estate: Real estate agents may be incentivized to push clients towards more expensive properties to earn higher commissions, potentially disregarding the buyer’s budget or preferences.

4. Government Agencies: Agency costs can also be present in government agencies. For instance, government contractors may overcharge for services or deliver subpar results due to inadequate monitoring or conflicts of interest.

5. Non-Profit Organizations: Even in non-profit organizations, agency costs can be a concern. Managers of these organizations may not always act in the best interest of the beneficiaries, resulting in misappropriation of funds or ineffective allocation of resources.

Conclusion

Agency costs are an integral part of various business and organizational relationships. Recognizing the potential conflicts of interest between principals and agents is crucial in managing these costs effectively. By implementing strategies to minimize agency costs, such as effective monitoring, strong communication, and transparent contractual agreements, businesses can strive towards achieving optimal decision-making and efficient outcomes.

:max_bytes(150000):strip_icc()/Unsystematicrisk_final-31b6d4ce82394ebe8fbebeb331c3fc29.png)