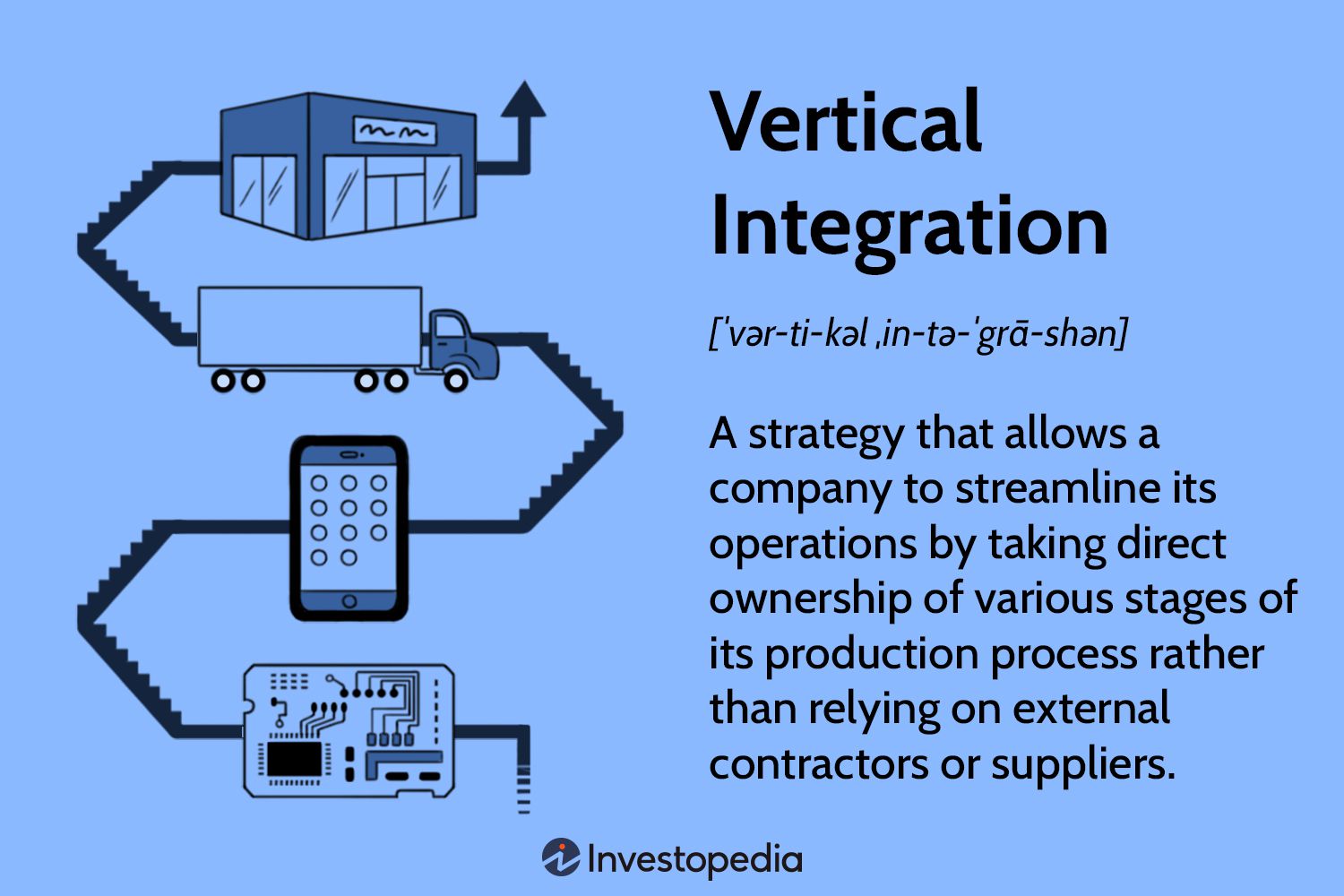

Backward Integration | The Complete Guide to Business Growth

Backward integration is a crucial business strategy that involves a company expanding its operations by acquiring or integrating suppliers or distributors. With backward integration, a company gains more control over its supply chain and reduces dependence on external parties. This strategic move can lead to increased efficiency, cost savings, and enhanced competitiveness.

Credit: www.investopedia.com

The Benefits of Backward Integration

There are numerous benefits associated with implementing backward integration in your business:

1. Cost savings: By integrating suppliers or distributors, you eliminate the need for middlemen, which reduces costs and allows for better negotiation power.

2. Quality control: Owning and integrating suppliers allows you to maintain greater control over the quality of materials or products used in your business.

3. Reduced dependency: Backward integration helps mitigate the risks associated with relying on external suppliers or distributors.

4. Increased efficiency: By integrating processes and streamlining the supply chain, you can achieve greater operational efficiency and eliminate bottlenecks.

5. Competitive advantage: Backward integration can give you a competitive edge by differentiating your business and providing unique offerings to customers.

Implementing Backward Integration

Successfully implementing backward integration requires careful planning and execution. Here are the key steps to follow:

1. Conduct A Thorough Analysis

Prior to implementing backward integration, conduct a comprehensive analysis of your supply chain. Identify the critical components or processes where integration can add value and reduce costs.

2. Identify Potential Partners

Research and identify potential suppliers or distributors that align with your business objectives and have a strong track record in quality and reliability. Evaluate their capabilities and make informed decisions about which partners to integrate.

3. Develop Strategic Partnerships

Engage in discussions with potential partners and establish strategic alliances. Negotiate favorable terms that encompass pricing, quality standards, and other relevant aspects of the partnership.

4. Establish Legal Agreements

Ensure that all necessary legal agreements, such as contracts and non-disclosure agreements, are in place to protect the interests of both parties involved in the integration.

5. Monitor And Optimize

Continuously monitor the performance of your backward integration efforts. Look for opportunities to optimize the supply chain, improve efficiency, and adapt to changing market conditions.

Real-Life Examples

Several companies have successfully implemented backward integration to fuel their growth and gain a competitive advantage:

Company

Industry

Integration Example

Apple

Technology

Apple acquired chip manufacturers to ensure a steady supply of high-quality components.

Starbucks

Food and Beverage

Starbucks established its own coffee bean farms to maintain control over the quality and supply of its primary raw material.

Amazon

Retail

Amazon acquired Whole Foods, allowing it to integrate the grocery supply chain into its online retail operations.

These examples highlight the effectiveness of backward integration in enhancing competitiveness and driving growth.

Credit: www.smartsheet.com

Conclusion

Backward integration can be a game-changer for businesses looking to achieve sustainable growth and improve their competitive position. By taking control of your supply chain and integrating key partners, you can gain cost savings, improve quality control, and reduce dependency on external parties. Remember to plan meticulously, choose the right partners, and continuously monitor and optimize your integration efforts. By doing so, you can reap the numerous benefits that backward integration offers.

Cumulative Dividend – Maximizing Your Investment Income

When it comes to investing in stocks, one of the ways to generate consistent income is through cumulative dividends. In this article, we will explore what cumulative dividends are, the benefits they offer, and how they can help maximize your investment income.

Understanding Cumulative Dividends

Cumulative dividends are a type of dividend structure offered by certain companies to its shareholders. Unlike regular dividends, which are paid on a regular basis, cumulative dividends accumulate over time when payments are missed or not made in full.

Let’s illustrate this with an example. Suppose you own 100 shares of a company that offers cumulative dividends at a rate of $1 per share per year. In a regular dividend structure, if the company fails to pay dividends for a year, you would not receive any dividend income. However, with cumulative dividends, the missed dividend is added to your account and accrues as an unpaid obligation.

The Benefits of Cumulative Dividends

One of the primary benefits of cumulative dividends is their potential for higher returns. Since missed dividends accumulate, once the company starts paying dividends again, shareholders with cumulative dividends are entitled to receive any outstanding back payments. This can result in a significant boost to your investment income.

In addition, cumulative dividends provide a level of security to investors. Companies that offer cumulative dividends are legally obligated to pay back any missed dividends before distributing dividends to common shareholders. This ensures that shareholders with cumulative dividends are given priority when it comes to receiving dividend payments.

Credit: www.yumpu.com

Maximizing Your Investment Income

If you are looking to maximize your investment income, here are a few tips:

1. Research Companies

Before investing in a company, research its dividend policy. Look for companies that offer cumulative dividends as part of their dividend structure. This will give you the advantage of potential future returns, even if dividends are temporarily suspended.

2. Diversify Your Portfolio

Spread your investments across different companies and industries. Diversification helps minimize the risk of relying on a single stock for dividend income. Choose companies with strong financials and a consistent track record of paying dividends.

3. Reinvest Your Dividends

Consider reinvesting your cumulative dividends back into the same company or other dividend-paying companies. By reinvesting, you can benefit from the power of compounding and potentially increase your investment income over time.

4. Monitor Dividend Payments

Stay updated on the dividend payments of companies you have invested in. If a company misses a dividend payment, keep track of the accumulated amount. Once the company resumes dividend payments, you will be entitled to receive the outstanding amounts due to the cumulative dividend structure.

Credit: fastercapital.com

Conclusion

In summary, cumulative dividends provide investors with the opportunity to maximize their investment income by accumulating missed dividend payments. By investing in companies that offer cumulative dividends and following the tips mentioned above, you can take advantage of this unique dividend structure to enhance your returns and build a robust investment portfolio. Remember, though, to always do your due diligence before making any investment decisions and consult with a financial advisor if needed.

Demand Shock: Understanding its Impact and How to Navigate Through It

In the world of economics, demand shock refers to a sudden and significant change in the demand for goods and services. This shift in demand can occur due to various factors such as changes in consumer preferences, economic crises, natural disasters, or even technological advancements. Regardless of the cause, demand shocks can have a profound impact on businesses, industries, and economies as a whole.

The Impact of Demand Shock

When a demand shock hits an industry or market, it disrupts the balance between supply and demand. This disruption can lead to several consequences:

Price Volatility: Demand shocks often result in extreme fluctuations in prices. When demand unexpectedly increases, prices tend to rise, and when demand unexpectedly decreases, prices fall sharply.

Supply Chain Disruptions: A sudden surge or decline in demand can disrupt the entire supply chain. Suppliers may struggle to meet increased demand, causing shortages, while a drop in demand can lead to excess inventory and financial losses.

Business Failures: Industries heavily impacted by demand shocks may experience bankruptcies, closures, and layoffs. Businesses that fail to adapt to changing market conditions are at a higher risk of going under.

Unemployment: Demand shocks can lead to a rise in unemployment rates as businesses downsize or shut down. This can have cascading effects on the overall economy, reducing consumer spending and resulting in further demand contractions.

Market Distortions: Demand shocks can create imbalances in supply and demand, leading to market distortions. This can potentially result in monopolistic behavior, reduced competitiveness, and hindered economic growth.

Navigating Through Demand Shock

While demand shocks can be challenging to navigate, businesses and economies can take certain steps to mitigate the negative impact:

Monitor Trends: Stay abreast of market trends and consumer behavior to identify potential demand shocks early on. By anticipating shifts in demand, businesses can better prepare themselves to respond effectively.

Diversify Offerings: Relying heavily on a single product or service increases vulnerability to demand shocks. Diversifying your offerings and expanding into new markets can help mitigate the risks associated with sudden changes in demand.

Adjust Production Levels: When faced with a demand shock, it is crucial to assess production levels and align them with the current demand. Scaling down production in the face of decreased demand can prevent excess inventory, while scaling up production during a surge in demand can help meet customer needs.

Strengthen Supply Chains: Building resilient and robust supply chains is vital in navigating through demand shocks. Establishing backup suppliers and diversifying sourcing locations can help businesses maintain continuity even during disruptions.

Invest in Technology: Embracing technological advancements can enhance operational efficiency and enable better demand forecasting. Utilizing data analytics and automation tools can facilitate accurate demand predictions, helping businesses make informed decisions.

Collaborate and Innovate: During challenging times, collaboration and innovation become crucial. Businesses can explore partnerships, seek new ways to differentiate themselves, and adapt their products or services to meet evolving customer needs.

Real-World Examples of Demand Shock

Throughout history, various demand shocks have had profound effects on different sectors:

Event

Sector

Impact

The 2008 Financial Crisis

Finance and Real Estate

Massive decrease in demand for housing and financial products, leading to market crashes and economic recession.

The COVID-19 Pandemic

Travel and Hospitality

Sharp decline in demand for travel and tourism-related services, causing airline bankruptcies, hotel closures, and job losses.

The Rise of E-Commerce

Retail

Increasing demand for online shopping, triggering a decline in brick-and-mortar store sales and a shift in consumer behavior.

These examples highlight the transformative impact demand shocks can have on specific industries and economies at large.

Frequently Asked Questions Of Demand Shock

Q: What Is A Demand Shock?

A: A demand shock refers to a sudden and significant change in consumer demand for goods or services, often caused by unexpected events such as economic disruptions or changes in consumer behavior.

Q: How Does A Demand Shock Affect The Economy?

A: A demand shock can have various effects on the economy, including decreased consumer spending, reduced business revenues, and potential job losses. It can also lead to changes in market demand and supply dynamics.

Q: Can Demand Shocks Be Predicted?

A: While it is difficult to predict the occurrence of specific demand shocks, economists analyze historical data and market trends to identify potential risks and vulnerabilities that may increase the likelihood of demand shocks.

Q: What Are The Common Causes Of Demand Shocks?

A: Demand shocks can be triggered by various factors, such as natural disasters, financial crises, changes in government policies, shifts in consumer preferences, or unexpected global events like pandemics.

Conclusion

Demand shocks are inevitable and can have wide-ranging effects on businesses and economies. By understanding their impact and implementing strategic measures, businesses can navigate through demand shocks successfully. Flexibility, adaptability, and proactive decision-making are key in withstanding the challenges posed by sudden shifts in demand. By staying alert, diversifying, and investing in resilience, businesses can emerge from demand shocks stronger and more resilient than ever before.

The Paradox of Thrift: Understanding its Importance in the Economy

In economics, the concept of “the paradox of thrift” refers to a situation where individual attempts to save more can lead to a decrease in overall saving and economic growth. It may seem counterintuitive, but this paradox highlights the interconnectedness of saving and spending in an economy. In this article, we will delve deeper into the paradox of thrift and explore its implications.

How Does the Paradox of Thrift Work?

At first glance, it may seem logical that if individuals decide to save more money, it should be beneficial for the economy as a whole. After all, saving is essential for long-term financial stability and economic growth. However, when everyone in the economy starts saving at the same time, it can have unintended consequences.

When people reduce their spending and increase their saving, it directly affects businesses. As consumer demand decreases, businesses have less incentive to produce goods and services, which ultimately leads to a decrease in employment opportunities. Consequently, the decrease in employment reduces people’s ability to save, perpetuating a cycle of reduced spending and economic stagnation.

Credit: fastercapital.com

The Multiplier Effect

One of the key factors that exacerbates the paradox of thrift is the multiplier effect. When individuals save rather than spend, the overall level of spending in the economy decreases. This decrease in spending ripples through the economy, affecting various sectors. Businesses experience reduced revenues, which can result in cost-cutting measures such as layoffs or reduced investment in new projects.

The reduction in consumer spending further reverberates to suppliers, who experience decreased demand for their products or services. This then leads to more layoffs or reduced production capacity. The cycle continues, ultimately undermining economic growth and stability.

Credit: www.mdpi.com

Government Intervention and Balancing the Paradox

While the paradox of thrift can have negative repercussions on the economy, governments play a crucial role in mitigating the effects. Through fiscal policy, governments can stimulate aggregate demand by implementing measures such as tax cuts or increased government spending on infrastructure projects.

By increasing government spending, it injects money into the economy and helps compensate for the decrease in consumer spending. This can kick-start economic activity, boost employment, and bring confidence back to the market. Additionally, governments can implement policies that encourage savings while also promoting spending, striking a balance between individual saving and economic growth.

The Importance of Consumer Confidence

The paradox of thrift also highlights the significance of consumer confidence in economic stability. When consumers are cautious about the future and save more, it reflects a lack of confidence in the economy. This can further dampen economic activity, as businesses respond to decreased demand by reducing investment and employment opportunities.

On the other hand, when consumers have confidence in the economy and are more willing to spend, it fuels economic growth. Increased consumer spending encourages businesses to invest and expand, thus creating more employment opportunities and ultimately leading to a healthier economy.

In Conclusion

The paradox of thrift serves as a reminder that individual saving habits can have far-reaching impacts on the economy as a whole. While saving is crucial for personal financial stability, excessive saving can hinder economic growth. Finding a balance between saving and spending is essential, and governments play a significant role in ensuring that the economy remains dynamic and resilient.

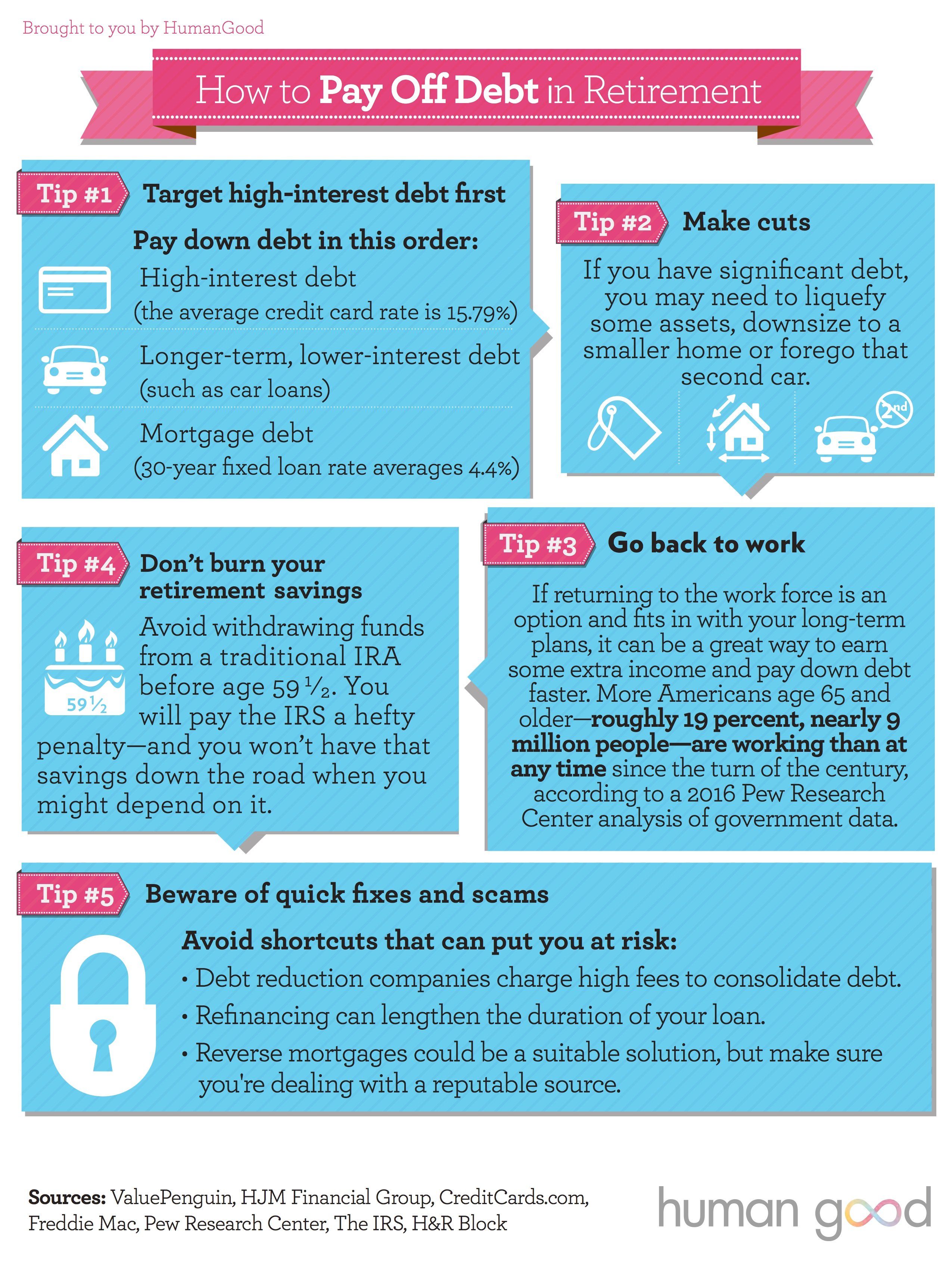

The best way to pay off a high interest credit card is to focus on making larger payments and reducing expenses. Paying more than the minimum balance each month will help you pay off the debt faster and save on interest charges.

Additionally, cutting back on unnecessary expenses can free up extra money to put towards your credit card payments. By following these strategies, you can effectively pay off your high interest credit card and improve your financial situation.

Credit: www.humangood.org

Evaluate Your Current Credit Card Situation

Evaluate your current credit card situation to find the best way to pay off a high interest credit card. Analyze your debt, create a repayment plan, and consider balance transfers or debt consolidation options to save on interest and become debt-free sooner.

If you find yourself burdened with a high-interest credit card, it’s essential to assess your current situation before taking any steps towards paying it off. Evaluating your credit card situation will give you a clear understanding of where you stand and help you make informed decisions on how to tackle your debt.

Check Your Current Interest Rate

Determining your credit card’s interest rate is the first step to understanding the financial implications of your debt. Interest rates play a significant role in how much you will ultimately pay back to the credit card issuer. To find your interest rate:

Log in to your online credit card account.

Locate the section that details your card’s terms and conditions.

Look for the section that mentions the annual percentage rate (APR) or interest rate.

Take note of the interest rate percentage, as this will help you evaluate the impact it has on your debt.

Review Your Credit Card Balance, Ensuring

Knowing your credit card balance is crucial when strategizing to pay off a high-interest credit card. To review your balance:

1. Log in to your online credit card account.

2. Locate the section that provides you with your current balance.

3. Take note of this amount, as it will determine the principal amount you need to pay off.

Explore Balance Transfer Options

Looking to pay off your high-interest credit card? Explore balance transfer options to find the best way to tackle your debt and save on interest charges. Move your balance to a lower interest rate card and take control of your finances.

Research Credit Card Offers With Low Interest Rates

Understand Balance Transfer Fees

When it comes to paying off a high-interest credit card, exploring balance transfer options can be a smart move. By transferring your outstanding balance to a credit card with a lower interest rate, you can save money on interest charges and pay off your debt more efficiently.

Research Credit Card Offers With Low Interest Rates

One of the first steps in exploring balance transfer options is to research credit card offers with low interest rates. Look for cards that specifically advertise balance transfer options or have promotional rates for new cardholders. Comparing different offers allows you to evaluate which credit card would be the most beneficial for your situation. Remember to pay close attention to the length of the promotional period, as well as any potential fees associated with the transfer.

Understand Balance Transfer Fees

To make an informed decision about balance transfers, it’s crucial to understand balance transfer fees. While a card may advertise a low or even 0% interest rate for a certain period, it’s common for there to be fees associated with the transfer. These fees are typically a percentage of the balance transferred, so it’s important to factor them into your calculations when determining if a balance transfer is the best way to pay off your high-interest credit card. Additionally, some credit cards may also have a maximum cap on the amount that can be transferred, so be sure to check for any limitations before proceeding with a balance transfer.

By researching credit card offers with low interest rates and understanding balance transfer fees, you can navigate the world of balance transfers more effectively. This way, you’ll be able to choose the best option to pay off your high-interest credit card and save money on interest charges. Remember to weigh the pros and cons of each offer and consider consulting with a financial advisor if necessary.

Create A Repayment Plan

A repayment plan is the best way to tackle a high interest credit card. By creating a structured plan, you can systematically pay off your debt, saving money in interest fees and improving your financial health.

Determine How Much You Can Afford To Pay Each Month

Before you start tackling your high-interest credit card debt, it’s important to determine how much you can afford to pay each month. Assessing your finances and understanding your current expenditure will help you create a realistic repayment plan.

Step 1: List down all your monthly income from various sources.

Step 2: Deduct your expenses, including rent, utility bills, groceries, transportation, and other necessary costs.

Step 3: Identify how much money is left after subtracting your expenses from your income.

Once you’ve calculated this amount, you know how much you can allocate towards paying off your high-interest credit card debt.

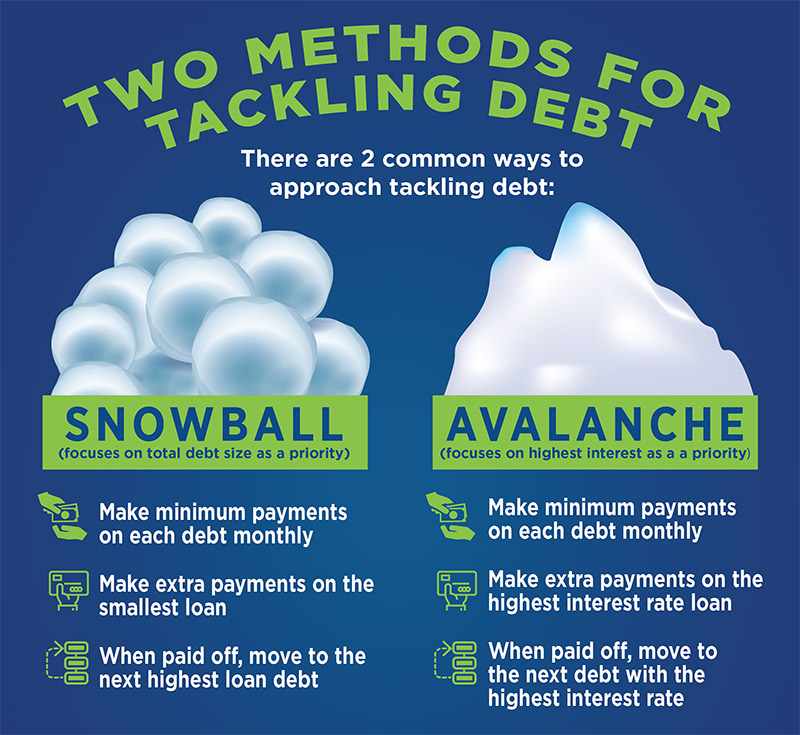

Prioritize Your Debt Payments

To effectively pay off your high-interest credit card, it’s essential to prioritize your debt payments. By strategically allocating your funds, you can snowball your payments and save money on interest in the long run.

Step 1: Make a list of all your credit card debts, including the balance and interest rate for each.

Step 2: Identify the credit card with the highest interest rate, as this is the one costing you the most money.

Step 3: Allocate the maximum amount you can afford towards paying off this high-interest credit card, while making minimum payments on your other credit cards.

Step 4: Once you’ve paid off the card with the highest interest rate, move on to the one with the next highest interest rate and repeat the process.

By prioritizing your debt payments based on interest rates, you’ll effectively reduce the amount of interest you pay over time.

Credit: www.investopedia.com

Consider Debt Consolidation

Consider debt consolidation as a potential solution to pay off your high-interest credit card. By consolidating your debts, you can streamline your monthly payments and potentially lower your interest rates. Here, we will discuss how to research and evaluate your options for debt consolidation, so you can make an informed decision.

Research Options For Consolidating Your High-interest Debt

When considering debt consolidation, it is important to research and explore the various options available to you. Look for reputable financial institutions, credit unions, or online lenders that offer debt consolidation services. You can also consult a credit counselor or financial advisor who can guide you through the process and help you find the best option for your specific situation.

Evaluate The Pros And Cons Of Debt Consolidation

While debt consolidation can be an effective way to manage your high-interest debt, it is essential to evaluate the pros and cons before making a decision. Let’s take a closer look at both:

Pros

Cons

Consolidating multiple debts into a single monthly payment

Potentially lowering your interest rates

Reducing the risk of missed payments and late fees

Simplifying your financial management

May require you to pay closing costs or origination fees

Could result in a longer repayment period

May impact your credit score temporarily

Some consolidation options may only be available to individuals with good credit

By carefully evaluating these pros and cons, you can determine if debt consolidation is the right choice for you. Consider your financial goals, budget, and overall debt situation when making this decision. Remember, what works for one person may not work for another, so it’s important to choose an option that aligns with your individual circumstances.

Credit: www.crcu.org

Frequently Asked Questions For Best Way To Pay Off A High Interest Credit Card

How Do I Pay Off My Credit Card If My Interest Is High?

To pay off a credit card with high interest, focus on these steps: 1. Make larger payments than the minimum amount due. 2. Prioritize paying off cards with the highest interest rate first. 3. Consider transferring the balance to a card with a lower interest rate or exploring debt consolidation options.

4. Try negotiating with your credit card company for a lower interest rate. 5. Avoid accumulating more debt by using cash or a debit card for purchases.

How To Pay Off $3 000 In 6 Months?

Pay off $3,000 in 6 months by creating a budget, cutting expenses, and prioritizing debt repayments. Increase income through side hustles or part-time work. Avoid unnecessary spending and consider selling unwanted items. Stay committed and track progress to stay on target.

What’s The Smartest Way To Pay Off A Credit Card?

To pay off a credit card smartly, make consistent payments, prioritize high-interest cards, and consider debt consolidation or a balance transfer. Avoid adding more debt, create a budget, and explore options like snowball or avalanche methods.

How To Pay Off $10,000 Credit Card Debt?

Pay off $10,000 credit card debt by following these steps: 1) Create a budget and cut unnecessary expenses. 2) Increase monthly payments to pay off the principal faster. 3) Consider balance transfers to lower interest rates. 4) Explore debt consolidation options.

5) Seek professional advice to create a personalized repayment plan.

Conclusion

Paying off a high-interest credit card can seem daunting, but with the right approach, it’s entirely possible. By focusing on strategies like consolidation, balance transfers, and making extra payments, you can take control of your debt. Remember to create a budget, track your expenses, and prioritize reducing your credit card balance.

With discipline and determination, you’ll soon be free from the burden of high-interest debt and on your way to financial freedom. Start today and take the first step towards a debt-free future.

In today’s digital age, social networking has become an integral part of our lives. It has revolutionized the way we connect, interact, and share information. Social networking platforms have opened up endless possibilities for communication and collaboration, enabling individuals from all around the world to connect with each other. In this blog post, we will explore the benefits of social networking, its impact on society, and how it has transformed the way we communicate.

Credit: growth99.com

The Benefits of Social Networking

Social networking brings people together, regardless of geographical boundaries. It allows us to connect and communicate with friends, family, colleagues, and even strangers, providing a sense of belonging and community. Through social networking, we can easily stay connected with people who are important to us, no matter where they are in the world.

One of the key benefits of social networking is the ability to share information and ideas. Whether it’s through text, photos, videos, or links, social networking platforms provide a platform for individuals and businesses to share their thoughts, experiences, and expertise with a wider audience.

Furthermore, social networking enables us to discover new opportunities, both personally and professionally. We can join groups and communities that align with our interests or professional goals, expanding our network and connecting with like-minded individuals. These connections can lead to new friendships, collaborations, and even career opportunities.

The Impact of Social Networking on Society

Social networking has had a profound impact on society, transforming the way we communicate and interact with each other. It has revolutionized the traditional methods of communication, making interactions more instantaneous, convenient, and global.

One of the significant impacts of social networking is its ability to break down barriers and bridge gaps between cultures. Through social networking, individuals from different backgrounds can come together, share experiences, and gain knowledge about diverse cultures and perspectives. It has opened up new horizons for understanding and appreciation of different cultures and has contributed to promoting inclusivity and global awareness.

Moreover, social networking has played a vital role in supporting social movements and bringing about social change. It has provided a platform for individuals to voice their opinions, raise awareness on social issues, and mobilize others towards a common cause. From raising funds for charitable organizations to organizing protests and awareness campaigns, social networking has empowered individuals to make a meaningful impact on society.

Transformation of Communication

Social networking platforms have transformed the way we communicate, offering a wide range of features and tools to facilitate interaction and collaboration. These platforms have become our primary means of communication, allowing us to connect with others in real-time through instant messaging, video calls, and voice chats.

Additionally, social networking platforms have made it easier to share and consume information. Through news feeds, we can stay updated with the latest news, trends, and happenings around the world. We can also follow our favorite brands, celebrities, and influencers, and get an insight into their lives and activities.

Furthermore, social networking has facilitated collaborative work environments, enabling teams to communicate and collaborate irrespective of their physical location. It has enhanced productivity and efficiency by providing tools for file sharing, project management, and virtual meetings.

Credit: www.linkedin.com

Conclusion

Social networking has undoubtedly transformed the way we connect, communicate, and collaborate. It has provided us with endless opportunities to interact with others, share information, and create meaningful connections. However, it is essential to use social networking platforms responsibly and maintain a balance between the digital world and real-life interactions.

As social networking continues to evolve, it will likely shape the future of communication and further connect the world digitally. Embracing the benefits of social networking while being mindful of its impact will allow us to harness its power and create a positive digital environment.

:max_bytes(150000):strip_icc()/backwardintegration.asp-final-fe409a0661e64045aeb4da510d5febd4.png)

:max_bytes(150000):strip_icc()/debt-avalanche-vs-debt-snowball-which-best-you.asp_v1-b62b7fef4c6949aa96550aa2c33b391e.png)