Bullish And Bearish | Understanding Market Sentiment

Bullish and bearish are two common terms used in the financial markets to describe market sentiment. Understanding these terms is crucial for investors and traders as they help to predict future price movements and make informed investment decisions.

What does bullish mean?

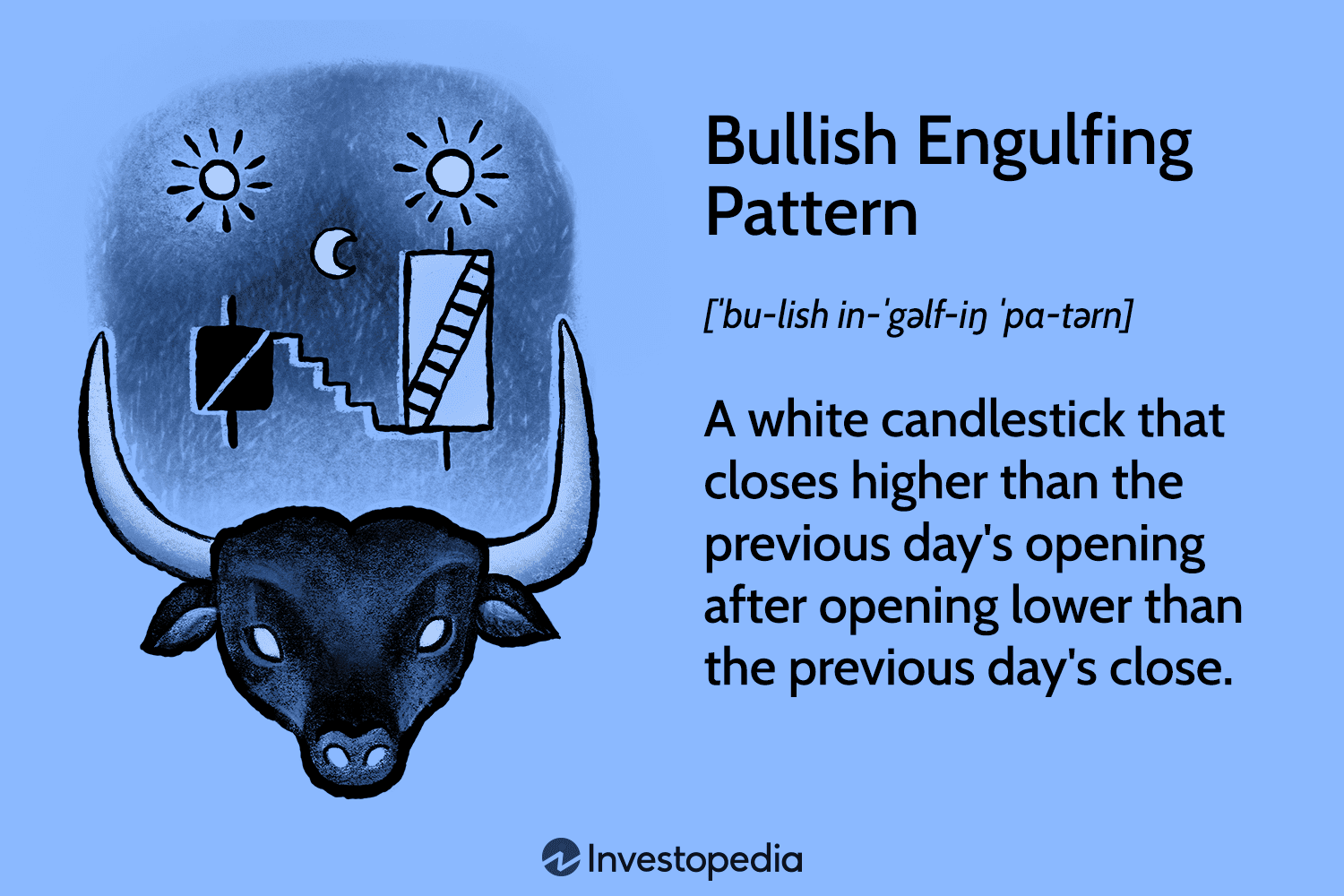

When the market is in a bullish state, it means that investors have a positive sentiment about the future direction of the market or a specific asset. In other words, they expect prices to rise. Bullish investors are optimistic and believe that there are more buyers than sellers, leading to upward price momentum. They often buy assets in the hopes of selling them at a higher price in the future.

Characteristics of a bullish market

During a bullish market, there are certain characteristics that can be observed:

Overall rising prices

Increasing trading volumes

Positive economic indicators

Optimistic investor sentiment

New highs being reached

Stock market indices showing upward trends

Credit: www.thebalancemoney.com

Credit: www.linkedin.com

What does bearish mean?

In contrast, when the market is bearish, it means that investors have a negative sentiment about the future direction of the market or a specific asset. They expect prices to fall and may sell assets, leading to downward price momentum. Bearish investors are pessimistic and believe that there are more sellers than buyers, resulting in a decline in prices. They often take short positions or sell assets.

Characteristics of a bearish market

During a bearish market, you can observe the following characteristics:

Overall declining prices

Decreasing trading volumes

Negative economic indicators

Pessimistic investor sentiment

New lows being reached

Stock market indices showing downward trends

Factors affecting market sentiment

Various factors can influence market sentiment and contribute to either a bullish or bearish market. Some of these factors include:

Factors

Bullish

Bearish

Economic indicators

Rising GDP, low unemployment

Weak GDP, high unemployment

Interest rates

Low interest rates stimulate borrowing and investment

High interest rates can discourage borrowing and investment

Corporate earnings

Increasing profits, strong financial results

Declining profits, poor financial results

Geopolitical events

Stability, positive developments

Uncertainty, conflicts, negative developments

Using bullish and bearish indicators

Investors and traders often use technical and fundamental analysis to identify bullish or bearish indicators. Technical indicators include moving averages, trend lines, and volume analysis, while fundamental analysis involves analyzing economic data, company financials, and news events.

By examining these indicators, investors gain insight into market sentiment and can make predictions about future price movements. This information helps them decide whether to enter a long or short position, buy or sell an asset, or adjust their investment strategy accordingly.

Conclusion

Understanding the concepts of bullish and bearish sentiment is essential for anyone involved in the financial markets. By recognizing these market sentiments and analyzing the factors that influence them, investors can make more informed decisions and potentially profit from market movements.

Unemployment is a pressing issue that affects economies worldwide. While the job market experiences fluctuations, one type of unemployment that often occurs is called cyclical unemployment. In this article, we will delve into the causes and potential solutions for cyclical unemployment.

Definition of Cyclical Unemployment

Cyclical unemployment is a type of unemployment that occurs due to fluctuations in the business cycle. It is also known as demand-deficient unemployment, as it arises when the demand for goods and services decreases during economic downturns.

The Causes of Cyclical Unemployment

The primary cause of cyclical unemployment is a decline in aggregate demand. When consumers and businesses spend less on goods and services, companies experience a decrease in demand, leading to reduced production and workforce layoffs. This results in an increase in the number of people looking for jobs, leading to cyclical unemployment.

The business cycle plays a crucial role in cyclical unemployment. The cycle consists of four phases: expansion, peak, contraction, and trough. During the contraction and trough phases, economic activity slows down, businesses face financial challenges, and unemployment rates tend to rise. As the economy recovers during the expansion and peak phases, cyclical unemployment typically decreases.

The Impact of Cyclical Unemployment

Cyclical unemployment can have severe consequences for both individuals and the overall economy. When people lose their jobs due to the cyclicality of the business cycle, they experience financial strain, reduced purchasing power, and increased uncertainty about their future. This, in turn, can lead to a decrease in consumer spending, further exacerbating the economic downturn.

From a macroeconomic perspective, high levels of cyclical unemployment indicate an underutilization of resources, as the economy is not operating at full capacity. This results in a loss of potential output and economic growth. Additionally, cyclical unemployment contributes to social and psychological costs, including higher crime rates, mental health issues, and social unrest.

Potential Solutions for Cyclical Unemployment

Addressing cyclical unemployment requires a combination of macroeconomic policies and targeted strategies. Here are some potential solutions:

1. Monetary Policy

The central bank can implement expansionary monetary policies to stimulate economic growth and increase aggregate demand. By lowering interest rates, the cost of borrowing decreases, incentivizing consumers and businesses to spend more, thus boosting the economy and reducing cyclical unemployment.

2. Fiscal Policy

Government intervention through fiscal policy can also play a crucial role in mitigating cyclical unemployment. During economic downturns, governments can increase public spending or implement tax cuts to stimulate demand and create jobs. These measures help to stabilize the economy and reduce the impact of cyclical unemployment.

3. Job Training And Education

Investing in job training programs and education can equip individuals with the necessary skills to adapt to changing economic conditions. By improving the match between the available workforce and the evolving demands of the economy, the occurrence of cyclical unemployment can be minimized.

4. Infrastructure Investment

Governments can boost employment and economic growth by investing in infrastructure projects during periods of downturn. These projects stimulate demand for labor, create job opportunities, and improve the overall productivity and competitiveness of the economy.

5. Coordination With Businesses

Collaboration between governments and businesses is crucial in addressing cyclical unemployment. By providing incentives for businesses to retain workers or support programs that encourage hiring during economic downturns, governments can help stabilize the labor market and reduce the adverse effects of cyclical unemployment.

Frequently Asked Questions Of Cyclical Unemployment

What Is Cyclical Unemployment?

Cyclical unemployment is a type of unemployment that occurs due to fluctuations in the business cycle. It is caused by a decrease in aggregate demand, forcing companies to lay off workers.

How Does Cyclical Unemployment Affect The Economy?

Cyclical unemployment can have significant effects on the economy. During economic downturns, the increase in cyclical unemployment leads to reduced consumer spending, decreased production, and lower overall economic growth.

What Are The Causes Of Cyclical Unemployment?

Cyclical unemployment is primarily caused by changes in the business cycle. Factors such as decreased consumer spending, recessions, and contractions in the economy contribute to the rise in cyclical unemployment.

How Does Cyclical Unemployment Differ From Other Types Of Unemployment?

Unlike other types of unemployment, cyclical unemployment is directly influenced by the business cycle. It occurs when there is a downturn in the economy and affects a large number of workers across various industries.

Conclusion

Cyclical unemployment is a significant challenge faced by economies during periods of economic downturn. Understanding the causes and implementing appropriate solutions is crucial in minimizing its impact. By employing a combination of monetary and fiscal policies, investing in education and training, and promoting collaboration between governments and businesses, we can work towards reducing cyclical unemployment and creating a more stable and resilient job market for all.

A Pay As You Go pension plan is a retirement savings option where contributions are made on a regular basis, and the funds are invested to provide a future income. A Pay As You Go pension plan is a flexible retirement savings option that allows individuals to make regular contributions, which are then invested to build a future income stream.

This type of plan allows for greater control over contributions and investment decisions and provides a reliable source of income during retirement. With the flexibility to adjust contributions based on changing financial circumstances, it offers a convenient and adaptable approach to retirement planning.

As individuals seek to secure their financial future, a Pay As You Go pension plan offers a practical and accessible solution for long-term savings and retirement income.

Understanding Pay As You Go Pension

What Is Pay As You Go Pension?

Pay As You Go Pension is a retirement scheme where current workers’ contributions are used to fund retirees’ benefits, rather than setting aside funds for individual workers. It is a commitment by the government to provide financial assistance to the aging population.

History Of Pay As You Go Pension

The concept of Pay As You Go Pension dates back to the 1889 Old Age Pension Act in the United Kingdom. This was designed to provide financial support for individuals over a certain age, funded by contributions from the current working population. Over time, similar systems have been implemented in various countries across the globe, each tailored to their specific economic and social needs.

Pros And Cons

While planning for retirement, one of the options to consider is the Pay As You Go (PAYG) pension plan. This type of pension scheme involves contributions from current workers that are used to pay pensions for current retirees. Understanding the pros and cons of this pension plan is crucial in making informed decisions for your financial future.

Advantages Of Pay As You Go Pension

There are several advantages to opting for a Pay As You Go pension plan:

Financial Stability: A PAYG pension plan ensures a steady source of income during retirement, providing financial stability without the need to accumulate large savings over the years.

Shared Responsibility: By having current workers contribute to the pension fund, the burden of retirement benefits is distributed, mitigating the risk of financial strain on individual retirement accounts.

Flexibility: Under the PAYG system, the amount of pension received is often adjustable to match the current economic conditions, allowing for potential increases to keep pace with inflation.

Social Safety Net: The Pay As You Go pension plan acts as a safety net, providing support for retirees who might not have sufficient savings or alternative sources of income.

Disadvantages Of Pay As You Go Pension

Despite its advantages, the PAYG pension plan also comes with some drawbacks to consider:

Population Aging: As the population ages and the number of retirees increases, the burden on the pension system intensifies, potentially leading to higher contributions for current workers to sustain the system.

Uncertainty: Factors such as economic instability, changing demographics, and fluctuations in the labor force can create uncertainty regarding the future sustainability of the PAYG pension plan.

Dependency on Government: The viability of the PAYG pension plan largely depends on government decisions and policies, which can change over time, potentially affecting the amount and availability of pension benefits.

Limited Control: Unlike private pension plans or individual retirement accounts, PAYG pension contributors have limited control over how their contributions are invested or managed.

Understanding the pros and cons of a Pay As You Go pension plan is crucial when it comes to making informed decisions for your retirement. While it offers stability and shared responsibility, there are also uncertainties and limitations to consider. Carefully weighing these factors will help you determine if this pension plan aligns with your financial goals and circumstances.

Comparison With Other Pension Plans

When it comes to planning for retirement, it’s important to explore a variety of options to ensure financial security in the golden years. Two common pension plans that individuals can consider are the Pay As You Go Pension Plan and the Defined Contribution Plan. Let’s take a closer look at how these plans compare to each other:

Contrasting Pay As You Go Pension With Defined Contribution Plan

The Pay As You Go Pension Plan is a unique arrangement where the current workforce finances the retirement benefits of the retirees. Unlike the Defined Contribution Plan, which is funded by individual contributions, the Pay As You Go Pension Plan does not require individuals to set aside a portion of their income for retirement. Instead, it relies on the ongoing contribution of the active workforce.

On the other hand, the Defined Contribution Plan allows individuals to make regular contributions towards their retirement. These contributions are typically invested in various investment vehicles, such as stocks, bonds, or mutual funds, with the goal of growing the retirement savings over time. The amount of money an individual receives upon retirement is based on the total value of their contributions and the performance of the investments.

In summary, the main difference between the Pay As You Go Pension Plan and the Defined Contribution Plan lies in their funding structure. While the Pay As You Go Pension Plan relies on the contributions of the current workforce, the Defined Contribution Plan requires individuals to make their own contributions towards their retirement.

Comparing Pay As You Go Pension With Defined Benefit Plan

Another pension plan commonly offered to employees is the Defined Benefit Plan. This plan guarantees a specific payout to retirees based on a predetermined formula, typically taking into account factors such as years of service and salary history. Let’s see how it compares to the Pay As You Go Pension Plan:

Contrast

Pay As You Go Pension Plan

Defined Benefit Plan

Funding

The Pay As You Go Pension Plan is funded by the active workforce.

The Defined Benefit Plan is funded by the employer or a combination of employer and employee contributions.

Payout

The payout for the Pay As You Go Pension Plan is dependent on the contributions made by the current workforce.

The Defined Benefit Plan provides a guaranteed payout based on a predetermined formula.

Risk

The risk of not receiving a pension is low as long as the active workforce continues to contribute.

The risk of not receiving the promised pension payout is generally assumed by the employer.

In summary, while the Pay As You Go Pension Plan relies on the contributions of the active workforce and does not guarantee a specific payout, the Defined Benefit Plan offers a guaranteed payout based on a predetermined formula and is funded by the employer or a combination of employer and employee contributions.

Future Of Pay As You Go Pension

As the landscape of pension plans evolves, the future of Pay As You Go Pension is a topic of growing interest. With shifting demographics and changing economic conditions, it’s crucial to analyze the challenges and reforms, as well as gain a global perspective on this system.

Challenges And Reforms

The challenges facing Pay As You Go Pension systems are multifaceted, ranging from an aging population to fluctuating birth rates. These demographic changes exert pressure on the sustainability of the system. To address these challenges, reforms such as increasing the retirement age, optimizing contribution structures, and diversifying investment strategies have been proposed.

Global Perspective On Pay As You Go Pension

When examining the global perspective on Pay As You Go Pension, it’s evident that various countries have distinct approaches and experiences with this system. For instance, some nations have successfully navigated the changing dynamics through innovative policy decisions and proactive measures. Others are still grappling with the intricacies of sustaining their Pay As You Go Pension schemes in the long run.

Frequently Asked Questions For Pay As You Go Pension Plan

What Is The Paygo System Pension?

The pay-as-you-go (PAYG) pension system is a retirement plan where current workers’ contributions fund retirees’ benefits.

What Is The Difference Between Pay-as-you-go And Funded Pension?

Pay-as-you-go pension is funded by contributions from current workers, while funded pension is built with contributions made by individuals throughout their working years. Pay-as-you-go relies on current workers to fund pensions for retirees, while funded pension allows individuals to accumulate savings for their retirement independently.

What Is The Pay-as-you-go System?

The pay-as-you-go system allows users to pay only for the services they use, without any fixed commitments or monthly fees. You can use and pay for services on a per-usage basis, providing flexibility and cost control.

Conclusion

To summarize, a Pay As You Go Pension Plan offers a flexible and convenient way to save for retirement. With the ability to contribute as and when you can, it caters to individuals who have irregular income or prefer a more adaptable retirement savings approach.

By avoiding long-term commitments, you have control over your contributions and can adjust them according to your financial circumstances. This ensures financial security without compromising your present needs. Explore the benefits of a Pay As You Go Pension Plan and start building your retirement fund today.

Revenge Spending: The Psychology and Impact on Economy

Revenge spending, also known as revenge shopping or revenge buying, has gained considerable attention in recent years. It refers to the phenomenon where individuals indulge in extravagant spending after a period of deprivation or restriction, seeking to make up for the lost time. This behavior has significant psychological implications and can have a profound impact on the economy.

The Psychology of Revenge Spending

Revenge spending is deeply rooted in human psychology. When individuals feel deprived or restricted, whether due to financial constraints or external circumstances, they often develop a strong desire to compensate for the perceived loss. This desire is fueled by the psychological need to regain a sense of control and emotional satisfaction.

Many people view revenge spending as a form of reward or self-soothing mechanism. By indulging in extravagant purchases, individuals perceive it as an opportunity to enhance their self-esteem, boost their mood, and counterbalance the negative emotions associated with deprivation.

Moreover, social comparison plays a significant role in revenge spending. In a society driven by consumerism, people are constantly exposed to the lifestyle and possessions of others. When individuals perceive that others have been able to enjoy luxuries or engage in extravagant spending, it further motivates them to engage in revenge spending to keep up with social expectations.

Credit: www.elon.edu

The Impact on the Economy

Revenge spending can have a substantial impact on the economy, both positively and negatively. During periods of economic recovery or after a significant event, such as the lifting of COVID-19 restrictions, revenge spending can fuel consumer demand and stimulate economic growth. This surge in spending can benefit businesses across various sectors, particularly those heavily reliant on discretionary spending.

However, revenge spending can also lead to unsustainable patterns of consumption. Individuals may engage in impulsive buying decisions, exceeding their financial means and accumulating debt. Such behavior can be detrimental to personal financial stability and can have long-term consequences for individuals and the overall economy.

Businesses, on the other hand, need to be cautious when targeting revenge spenders. While they represent a lucrative market segment, it is essential to strike a balance between catering to their desires and maintaining ethical marketing practices. Encouraging responsible spending and offering sustainable products or services can help businesses mitigate the negative impacts of revenge spending.

Credit: www.hottytoddy.com

The Role of Marketing and Retail Strategies

Marketers and retailers play a vital role in the revenge spending phenomenon. By understanding the psychological drivers behind this behavior, they can craft effective strategies to attract and engage revenge spenders.

Creating a sense of urgency, exclusivity, and scarcity through limited-time offers or limited stock can provoke consumers to make impulsive buying decisions. Utilizing social media influencers and digital marketing channels can also tap into the desire for status and external validation, further encouraging revenge spending.

Moreover, retailers can implement loyalty programs or personalized offers, rewarding revenge spenders for their continued support. By fostering a positive shopping experience and establishing emotional connections with consumers, retailers can foster long-term relationships and loyalty.

In Conclusion

Revenge spending is a complex phenomenon influenced by psychological factors and societal expectations. It can both stimulate economic growth and lead to unsustainable spending patterns. Understanding the psychology behind revenge spending is critical for businesses and consumers alike to strike a balance between indulgence and financial stability.

As individuals, it is crucial to practice responsible spending and be mindful of our financial limitations. Businesses, on the other hand, must adapt their marketing and retail strategies to cater to the desires of revenge spenders while promoting sustainable consumption.

Noise Trader – Understanding the Impact of Emotional Trading

Investing in financial markets involves a range of participants, each with different strategies and objectives. One category of traders, known as noise traders, can have a unique impact on market dynamics due to their emotional decision-making process. In this article, we will explore the concept of noise traders, their behaviors, and the implications for overall market efficiency.

What are Noise Traders?

Noise traders are individuals or institutions who make investment decisions based on emotions, intuition, or incomplete information rather than rational analysis. They often trade on short-term market trends or rumors without thoroughly assessing the underlying fundamentals of the securities they are trading.

Noise traders are driven by various behavioral biases, including overconfidence, herding, and anchoring. These biases can lead to market inefficiencies and contribute to exaggerated price movements.

Credit: www.mdpi.com

Behavioral Biases of Noise Traders

1. Overconfidence: Noise traders tend to overestimate their knowledge and abilities, leading them to trade excessively. They often believe they have an edge in predicting short-term price movements, even when evidence suggests otherwise.

2. Herding: Noise traders are prone to following the crowd and mimicking the actions of other market participants. This herd mentality can create exaggerated price movements as traders react to the actions of others rather than fundamental factors.

3. Anchoring: Noise traders may anchor their trading decisions to certain reference points, such as past prices or media reports. This bias can lead them to hold onto losing positions in the hope of a price rebound or to sell winners prematurely out of fear of missing out on potential gains.

Credit: www.wsj.com

The Impact of Noise Traders

Noise traders can have both positive and negative impacts on market dynamics:

Positive Impact

Negative Impact

1. Liquidity provision to the market.

1. Increased market volatility.

2. Enhanced price discovery.

2. Mispricing of securities due to irrational trading.

3. Increased trading volume.

3. Amplification of market bubbles or crashes.

While noise traders may contribute to market inefficiencies, their presence also creates opportunities for profit-seeking investors to exploit mispriced securities through arbitrage strategies.

Managing Noise Trader Behavior

Financial markets rely on information dissemination and efficient pricing mechanisms to function effectively. While it is impossible to completely eliminate the presence of noise traders, there are measures that can be taken to manage their behavior:

Improved Investor Education: Educating investors about the importance of rational decision-making and the impact of emotional biases can help reduce the prevalence of noise trading.

Market Regulations: Implementing regulations that promote transparency, discourage market manipulation, and enhance market surveillance can help minimize the negative impact of noise traders.

Liquidity Management: Maintaining adequate liquidity in the market can help absorb the impact of noise traders and prevent excessive price fluctuations.

In Conclusion

Noise traders play a significant role in financial markets, driven by their emotions and biases. While their behaviors can lead to market inefficiencies, they also create opportunities for profit-seeking investors. Recognizing the impact of noise traders and implementing measures to manage their behavior is essential for maintaining overall market efficiency.

Put Swaption: A Comprehensive Guide on How to Utilize it Effectively

Put swaption is a financial instrument commonly used in the world of options trading. In this comprehensive guide, we will explore what put swaptions are, how they work, and how you can effectively utilize them in your investment strategy.

Understanding Put Swaptions

A put swaption is a type of option that gives the holder the right, but not the obligation, to enter into a swap agreement as the fixed-rate receiver. The underlying asset in a put swaption is typically an interest rate swap.

The key feature of a put swaption is the ability to protect against a drop in interest rates. If the interest rates decrease during the life of the swaption, the holder can exercise the option and enter into a swap agreement to receive the fixed rate, which is higher than the prevailing market rate.

How Put Swaptions Work

Put swaptions work in the following manner:

Investor A purchases a put swaption from Investor B, who is the writer of the option.

If interest rates increase, rendering the fixed rate less attractive, Investor A will not exercise the put swaption and the contract will expire worthless.

If interest rates decrease, making the fixed rate more attractive, Investor A will exercise the put swaption.

If the swaption is exercised, Investor A will enter into a swap agreement with Investor B, becoming the fixed-rate receiver.

Investor B will become the floating-rate receiver, essentially swapping the interest rate payments.

The value of the put swaption increases as the difference between the fixed rate and the prevailing market rate widens.

It is important to note that put swaptions are typically used by investors as a form of insurance against falling interest rates, rather than for speculation purposes.

Benefits of Put Swaptions

There are several benefits associated with the usage of put swaptions:

Protection against falling interest rates: Put swaptions provide investors with a valuable tool to protect against the negative impact of decreasing interest rates.

Flexibility: The option to exercise the put swaption provides investors with flexibility in their investment strategy, allowing them to adapt to changing market conditions.

Potential for profit: If interest rates drop significantly, the investor can profit from exercising the put swaption and entering into a swap agreement at a higher fixed rate.

Considerations when Utilizing Put Swaptions

While put swaptions offer various benefits, it is important to consider the following factors before incorporating them into your investment strategy:

Market conditions: Analyze market conditions thoroughly to assess whether the usage of put swaptions is appropriate given the current interest rate environment.

Cost: Put swaptions may come with a premium cost, which needs to be taken into account when evaluating their potential benefits.

Risk tolerance: Understand your risk tolerance and investment goals to determine if put swaptions align with your overall investment strategy.

Frequently Asked Questions On Put Swaption

Q: What Is A Put Swaption?

A: A Put Swaption is a financial contract that gives the holder the right to enter into a swap agreement as the receiver of the fixed-rate payment.

Q: How Does A Put Swaption Work?

A: With a Put Swaption, the holder has the option to enter into a swap where they receive a fixed rate and pay a floating rate.

Q: What Are The Benefits Of Using A Put Swaption?

A: Put Swaptions provide a way to protect against falling interest rates and can enhance hedging strategies to manage interest rate risk.

Q: Who Typically Uses Put Swaptions?

A: Institutional investors, such as banks and insurance companies, often use Put Swaptions to manage their interest rate exposure.

Conclusion

Put swaptions can be a valuable tool for investors looking to protect against falling interest rates. By providing a flexible option to enter into a swap agreement as the fixed-rate receiver, put swaptions offer a level of risk management in uncertain market conditions.

However, it is essential to thoroughly analyze market conditions, consider cost implications, and understand your risk tolerance before incorporating put swaptions into your investment strategy. Utilize the benefits of put swaptions wisely and make informed decisions to enhance your overall investment performance.

:max_bytes(150000):strip_icc()/what-do-long-short-bullish-and-bearish-mean-1030894-v2-94771b18dbf54fb8a7f624297405acf4.png)