Market risk affects cost of capital by increasing the required rate of return for investors, which can raise the cost of borrowing for companies. This can lead to higher expenses and decrease in profits.

Market risk is a key factor that impacts the cost of capital for businesses. It refers to the possibility of financial losses due to changes in market conditions such as interest rates, currency fluctuations, and economic volatility. The higher the market risk, the higher the return expected by investors, leading to an increase in the cost of capital for companies.

Understanding the influence of market risk on the cost of capital is crucial for businesses to make informed financial decisions and mitigate potential negative impacts on their bottom line.

Factors Influencing Market Risk

Market risk can significantly impact the cost of capital for businesses. Fluctuations in market conditions, economic indicators, and geopolitical events can all influence market risk. As a result, businesses may face higher borrowing costs and reduced investor confidence, impacting their overall cost of capital.

Factors Influencing Market Risk

Market risk can significantly impact a company’s cost of capital and ultimately affect its performance in the financial markets. Understanding the factors that influence market risk is crucial for businesses to make informed decisions and manage their cost of capital effectively. Two key factors that play a pivotal role in determining market risk are economic conditions and market volatility.

Economic Conditions

Economic conditions encompass a broad range of variables, including interest rates, inflation, and overall economic growth. In a thriving economy, where interest rates are low and consumer confidence is high, businesses generally face lower market risk. Conversely, during economic downturns, high inflation rates, and sluggish growth, market risk tends to elevate.

Market Volatility

Market volatility refers to the degree of variation in the trading price of a financial instrument within a specific period. Factors such as geopolitical events, corporate developments, and investor sentiment can contribute to market volatility. In times of high volatility, investors are likely to perceive greater uncertainty, leading to heightened market risk.

Understanding the intricate relationship between economic conditions and market volatility is crucial for companies to assess their exposure to market risk accurately. By considering these influential factors, businesses can develop robust strategies to mitigate market risk and effectively manage their cost of capital.

Methods To Measure Market Risk

Market risk plays a crucial role in determining the cost of capital for companies. Understanding the various methods to measure market risk is imperative for businesses to make well-informed financial decisions. By employing these methods, organizations can assess their exposure to market fluctuations and subsequently determine the appropriate capital cost. Let’s delve into the key methods used to measure market risk.

Beta Coefficient

The Beta coefficient, often referred to simply as beta, is a measure of a stock’s volatility in relation to the overall market. It provides insights into how a particular stock moves in comparison to the market as a whole. High-beta stocks are more volatile, while low-beta stocks demonstrate more stability. Calculating the beta coefficient enables investors and financial analysts to assess the systematic risk associated with a specific stock or portfolio.

Value At Risk (var)

Value at Risk (VaR) is a statistical measure used to quantify the potential loss on an investment, portfolio, or asset over a specified period. It helps in estimating the maximum potential loss given a certain level of confidence within a defined time frame. VaR is a valuable tool for risk management, allowing organizations to understand the worst-case scenario and implement appropriate risk mitigation strategies.

Managing Market Risk

Diversification

Diversification is a crucial strategy for managing market risk. By spreading investments across different asset classes and industries, companies can reduce the impact of volatility in any one market segment.

Derivatives

Derivatives offer another tool for managing market risk. These financial instruments, such as options and futures, allow companies to hedge against adverse price movements in the markets, helping to protect their cost of capital.

Frequently Asked Questions For How Does Market Risk Affect Cost Capital

How Market Conditions Affect Cost Of Capital?

Market conditions affect the cost of capital by influencing interest rates and investor perception. In strong markets, access to capital is easier, lowering costs. In weak markets, borrowing becomes more expensive, raising costs. This impacts businesses’ ability to fund projects and determine their cost of capital.

How Does Risk Affect The Opportunity Cost Of Capital?

Risk affects the opportunity cost of capital by influencing the return investors expect. Higher risk often leads to higher returns, increasing the opportunity cost of capital. Lower risk, on the other hand, leads to lower returns, decreasing the opportunity cost of capital.

What Are The Factors Influencing Cost Of Capital?

Factors influencing cost of capital include interest rates, market conditions, company risk profile, and capital structure. The cost of debt and equity also affects it.

Conclusion

Market risk plays a crucial role in determining the cost of capital for businesses. Understanding and effectively managing market risk can significantly impact a company’s financial health and growth opportunities. By incorporating risk management strategies, organizations can mitigate potential losses and improve their overall capital structure.

Embracing a proactive approach to market risk can ultimately lead to sustainable business success.

Endogenous growth theory is a concept in economics that focuses on explaining the factors and mechanisms that drive economic growth within a country. Unlike traditional exogenous growth theories, which emphasize the role of exogenous factors such as technology and capital accumulation, endogenous growth theory posits that growth is driven by internal factors such as human capital, innovation, and productivity.

Credit: fastercapital.com

The Key Drivers of Endogenous Growth

Several key factors contribute to endogenous growth, and understanding them is crucial for policymakers and economists. The following table highlights some of the main drivers:

Factor

Description

Human Capital

The knowledge, skills, and abilities that individuals acquire through education, training, and experience.

Innovation

The creation and adoption of new ideas, technologies, and processes that improve productivity and create economic value.

Research and Development (R&D)

Investments in R&D activities to drive innovation and technological advancements.

Entrepreneurship

The process of identifying and exploiting new business opportunities, driving economic growth through the creation of new ventures.

Institutional Framework

The legal, regulatory, and economic environment that supports entrepreneurship, innovation, and investment in human capital.

Credit: www.sciencedirect.com

The Role of Human Capital

Human capital plays a crucial role in endogenous growth theory. Investment in education and training is seen as essential for boosting productivity and driving economic progress. A skilled workforce that possesses up-to-date knowledge and expertise can generate innovation, adopt advanced technologies, and improve production processes, leading to sustained economic growth.

Furthermore, the development of human capital encourages technological advancements in areas such as healthcare, agriculture, and information technology. These advancements not only contribute to economic growth but also improve the overall quality of life for the population.

Innovation and Technological Progress

Innovation is another key driver of endogenous growth. By fostering a culture of creativity and encouraging investment in research and development, countries can stimulate innovation and technological progress. This leads to improvements in productivity, market expansion, and the creation of new industries.

Moreover, innovation has a positive feedback effect on economic growth. As new ideas and technologies are developed, they generate further opportunities for growth, attracting additional investment and fostering a virtuous cycle of innovation, productivity gains, and economic development.

Government Policies and the Institutional Framework

Effective government policies and a supportive institutional framework are essential for fostering endogenous growth. Governments can encourage innovation and human capital development through measures such as tax incentives for research and development, funding for education and vocational training, and the protection of intellectual property rights.

Furthermore, a transparent and efficient legal system, reliable infrastructure, and access to financial resources are also crucial for nurturing entrepreneurship and attracting investments. A robust institutional framework helps create an enabling environment that promotes economic growth by facilitating innovation, facilitating collaboration, and reducing barriers to entry.

Conclusion

Endogenous growth theory provides a valuable framework for understanding the internal drivers of economic growth. By focusing on factors such as human capital, innovation, and the institutional framework, policymakers and economists can develop strategies to promote sustained economic development.

Investing in education and training, fostering innovation, and creating a supportive environment for entrepreneurship are key ingredients for unlocking the potential of endogenous growth. This approach not only fuels economic progress but also contributes to improving living standards and enhancing overall societal well-being.

The financial crisis significantly impacted millennials, leading to job insecurity and delayed financial milestones. As the crisis unfolded, millennials faced challenges in finding stable employment and struggled to achieve economic independence.

Many were burdened with high levels of student loan debt, making it difficult to save for their futures. The financial crisis also led to a decline in home ownership among millennials and delayed their ability to start families. Additionally, the stock market crash eroded their investment portfolios, impacting their long-term financial security.

Overall, the financial crisis had a profound and lasting impact on the financial well-being of millennials, shaping their attitudes and behaviors toward money and economic stability.

Impact On Job Market

When financial crises hit, the impact on the job market is one of the most immediate and enduring consequences. Millennials, in particular, have felt the reverberations of economic downturns in their career prospects and opportunities. Let’s delve into how the financial crisis affected the job market for this generation.

Unemployment Rates

Financial crises often lead to a surge in unemployment rates as businesses downsize and cut costs to weather the economic storm. Millennials faced significant challenges during these periods as they struggled to secure stable employment. The instability of the job market during financial crises directly impacted the ability of this generation to kick-start their careers and build financial security.

Underemployment Issues

In addition to high unemployment rates, millennials also encountered underemployment issues. Many were forced to take on part-time or low-paying jobs that did not utilize their skills and education, leaving them financially strained and unable to progress in their careers. Underemployment can have long-term effects, leading to income stagnation and diminished prospects for wealth accumulation.

Challenges In Homeownership

Millennials have faced numerous challenges in achieving homeownership, particularly in the wake of financial crises. The rising housing costs and difficulty in saving for a down payment have made it increasingly tough for this demographic to realize their dream of owning a home.

Rising Housing Costs

The financial crises have led to a significant increase in housing costs, making it unattainable for many Millennials to afford their own homes. The inflation of housing prices has outpaced the growth of their income, creating a substantial barrier to entry into the housing market.

Difficulty In Saving For Down Payment

With the burdensome rise in housing costs, Millennials are finding it challenging to save for a down payment. The larger proportion of their income is allocated to rent and other living expenses, leaving little room for saving, thereby delaying or even preventing potential home purchases.

Moreover, the stringent lending criteria and high student loan debt further compound the struggle in accumulating sufficient funds for a down payment, impeding their homeownership ambitions.

Student Loan Burden

The financial crisis has burdened millennials with overwhelming student loan debt. This has created a significant impact on their financial well-being, making it challenging to achieve milestones such as homeownership and saving for retirement. The student loan burden continues to be a pressing concern for this generation, shaping their financial futures.

Increased Debt Levels

The student loan burden on millennials has reached unprecedented levels, causing a significant increase in their debt. With the rising cost of higher education, millennials have had to rely heavily on student loans to finance their studies. As a result, they find themselves grappling with overwhelming debt that can greatly affect their financial well-being.

This increased debt load has created immense pressure on millennials as they try to navigate their way through their careers and personal lives. Many are forced to delay important life milestones, such as buying a house or starting a family, due to the weight of their student loan obligations.

Moreover, the burden of increased debt levels can have far-reaching consequences beyond just personal goals. The overall economy can experience a slowdown as millennials have less disposable income to contribute to various sectors, such as housing, consumer goods, and investments. This, in turn, can have a detrimental impact on the nation’s economy as a whole.

Impact On Financial Stability

The student loan burden faced by millennials not only hinders their financial growth but also threatens their overall financial stability. Mounting debt can lead to increased stress, anxiety, and even mental health issues as individuals strive to make ends meet while paying off their loans.

In addition to the psychological toll, the financial stability of millennials is at risk due to their student loan burden. High monthly repayments make it challenging for them to save money, build an emergency fund, or invest in their future. With limited financial resources, they are left vulnerable to unexpected expenses or economic downturns.

Furthermore, the burden of student loans can also impact millennials’ ability to secure credit for other financial needs, such as buying a car or starting a business. Lenders may view the existing debt as a signal of risk, making it difficult for millennials to access additional funds when needed.

Unfortunately, the repercussions of this financial instability extend beyond an individual level. As a generation burdened by student loans struggles to achieve financial stability, it can have cascading effects on the economy as a whole. Reduced purchasing power and limited investment opportunities can impede economic growth, potentially leading to long-term consequences.

Effects On Long-term Financial Planning

Millennials have been navigating the treacherous financial landscape left in the wake of the global financial crisis. The repercussions of the crisis have cast a long shadow over their long-term financial planning, impacting retirement savings, and investment decisions. Let’s delve into the effects on these crucial aspects of financial stability in more detail.

Retirement Savings

Many millennials are finding it challenging to save for retirement in the aftermath of the financial crisis. The economic turmoil has made it difficult for this generation to secure stable, well-paying jobs. As a result, they are often unable to allocate the necessary funds towards their retirement accounts. This lack of saving early on can significantly hinder their ability to accumulate substantial retirement savings over time.

Investment Decisions

The financial crisis has left a lasting impression on the investment decisions of millennials. The shockwaves of the crisis have instilled a sense of caution, prompting many individuals to approach investment opportunities with increased scrutiny. A prevailing fear of market volatility has led to a more conservative approach, with millennials often favoring safer but lower yielding investments over riskier, potentially high-yield options.

Frequently Asked Questions For How Financial Crisis Affected Millennials

Why Millennials Are Struggling Financially?

Millennials struggle financially due to high student loan debt, low wages, and a competitive job market. Rising living costs and limited access to affordable housing also contribute to their financial challenges. Additionally, many are burdened with credit card debt and struggle to save for the future.

What Economic Problems Do Millennials Face?

Millennials face economic problems such as high levels of student debt, low wage growth, and difficulties in buying a home due to rising prices. They also encounter challenges in saving for retirement and have limited job opportunities with job insecurity.

These factors contribute to financial instability and a lack of economic mobility for this generation.

What Is The Debt Crisis For Millennials?

The debt crisis for millennials is the significant financial burden they face due to student loans, credit card debt, and rising housing costs. This affects their ability to save for the future and achieve financial stability.

Conclusion

As Millennials navigate the aftermath of the financial crisis, they face unique challenges and opportunities. Understanding the impact of this event on their financial decisions is crucial for shaping their future. By adapting and leveraging new tools and strategies, Millennials can navigate the economic landscape and build a more resilient and secure financial future.

Financial advisors provide crucial assistance in managing debt by offering expert advice and creating customized strategies. Debt can be overwhelming, but these professionals help clients develop a clear picture of their financial situation, explore available options, and design a plan to alleviate debt burdens efficiently.

By utilizing their expertise, financial advisors can provide clients with a comprehensive analysis of their debt, propose suitable debt management tools and techniques, and guide them towards achieving financial freedom. From consolidating debts, negotiating with creditors, and setting realistic repayment goals, to offering ongoing support and monitoring progress, financial advisors play a pivotal role in helping individuals regain control of their finances and achieve a debt-free future.

The Role Of Financial Advisors

Financial advisors play a crucial role in helping individuals and families overcome debt and achieve financial stability. With their professional expertise and customized financial plans, they provide invaluable guidance and support to help individuals navigate the complexities of debt management. In this article, we will explore the various ways in which financial advisors can assist in alleviating debt and creating a solid financial foundation.

Professional Expertise

Financial advisors possess the knowledge and experience necessary to effectively address debt-related issues. With their understanding of financial markets, investment strategies, and debt management techniques, they can offer insights that are tailored to the specific needs of their clients. Their expertise extends beyond mere numbers; they analyze individual circumstances, explore options, and provide recommendations that align with the goals and values of the client. By leveraging their professional knowledge, financial advisors guide individuals towards making informed decisions that will have long-lasting positive impacts on their financial well-being.

Customized Financial Plan

A key aspect of a financial advisor’s role in debt management is developing a customized financial plan. This plan takes into account individual income, expenses, assets, and liabilities to create a comprehensive roadmap for debt reduction. Through careful evaluation, financial advisors identify areas where individuals can cut costs, optimize their budgets, and maximize their income potential. They outline clear steps to be taken, suggest debt consolidation strategies when appropriate, and establish a timeline for achieving debt reduction goals. By tailoring the plan to suit individual circumstances, financial advisors empower individuals to overcome debt in a structured and achievable manner.

Moreover, financial advisors provide ongoing support and guidance throughout the implementation of the financial plan. They track progress, evaluate the effectiveness of strategies, and make adjustments as necessary. By ensuring that individuals stay on track and keep their financial goals in focus, financial advisors help them maintain their motivation and stay committed to the debt repayment plan.

In summary, financial advisors play a vital role in assisting individuals in their journey towards debt reduction and financial security. They bring their professional expertise and customizable financial plans to the table, which enable them to provide tailored guidance and support. By working with a financial advisor, individuals can gain the tools and knowledge necessary to overcome debt and ultimately achieve long-term financial success.

Debt Management Strategies

Financial advisors can assist in debt management strategies by providing personalized plans to tackle debt effectively. They offer guidance on consolidating debts, negotiating with creditors, and creating budgets to regain financial stability. With their expertise, individuals can navigate the complexities of debt management and work towards a debt-free future.

Financial advisors can play an instrumental role in helping individuals tackle their debt by implementing effective debt management strategies. These strategies are designed to provide individuals with the necessary tools and guidance to regain control of their finances and ultimately achieve debt freedom. Here are three key debt management strategies:

Debt Consolidation

Debt consolidation is a powerful approach that financial advisors often recommend to individuals burdened with multiple debts. It involves combining all outstanding debts into a single loan or credit line with a lower interest rate. By doing so, individuals simplify their repayment process and save money on interest charges. Debt consolidation provides not only financial relief but also peace of mind as individuals have a clear overview of their monthly repayment obligations.

Budgeting And Planning

Creating a realistic budget and sticking to it is crucial when dealing with debt. Financial advisors help individuals chart out a comprehensive budget that considers their income, expenses, and debt obligations. This budgeting and planning process entails identifying unnecessary expenses, prioritizing debt repayments, and establishing clear financial goals. By adopting a disciplined approach to budgeting, individuals can steadily reduce their debt and regain financial stability.

Debt Repayment Strategies

Financial advisors guide individuals in developing effective debt repayment strategies. These strategies may include the snowball method or the avalanche method. The snowball method involves paying off the smallest debts first, while the avalanche method focuses on tackling debts with the highest interest rates. By implementing these strategies, individuals can make significant progress in reducing their debt and gain momentum as they clear smaller balances or chisel away at high-interest debts.

It’s essential to note that debt management strategies vary depending on individual circumstances. Financial advisors leverage their expertise and customize strategies to match the specific needs and goals of their clients. By accessing professional guidance, individuals can overcome their debt challenges more efficiently and start building a solid financial foundation.

Negotiating With Creditors

Dealing with debt can be overwhelming and stressful, but financial advisors are there to lend a helping hand. One important aspect of their role is negotiating with creditors on behalf of their clients. By leveraging their expertise and experience, financial advisors can assist in debt resolution and pave the way towards financial freedom.

Debt settlement is a viable option that financial advisors explore with creditors to help alleviate financial burdens. With debt settlement, a creditor agrees to accept a reduced amount as a full payment on the outstanding debt. This can significantly reduce the total debt owed, allowing individuals to make more manageable payments and regain control over their finances. Negotiating favorable debt settlements requires sound financial knowledge, persuasive negotiation skills, and a thorough understanding of the client’s financial situation.

High interest rates on debts can make it challenging to make progress in paying them off. Financial advisors step in to negotiate lower interest rates with creditors. By persuading lenders to reduce the interest rates, financial advisors help to decrease the overall cost of the debt and allow for more substantial portions of payments to go towards reducing the principal amount owed. This reduction in interest rates not only eases the financial burden but also shortens the time it takes to become debt-free.

By negotiating with creditors, financial advisors play a crucial role in helping individuals tackle their debt issues effectively. Whether it’s through debt settlement or reducing interest rates, they strive to create a more feasible financial landscape for their clients. With their expertise and guidance, individuals can take proactive steps towards regaining control over their finances and achieving a debt-free future.

Improving Credit Score

Financial advisors have the expertise to guide individuals in improving their credit scores and managing debt effectively. Through personalized strategies and financial planning, they can help clients take control of their finances and achieve a better financial standing.

Credit Report Review

One of the first steps a financial advisor can take to help improve your credit score is to review your credit report. Your credit report contains important information about your financial history, including details about your credit accounts, payment history, and any outstanding debts. By thoroughly examining your credit report, a financial advisor can identify any errors or discrepancies that may be negatively impacting your credit score.

A credit report review with a financial advisor will also involve analyzing your credit utilization ratio, which is the amount of credit you’re using compared to your total credit limit. This ratio plays a significant role in determining your creditworthiness, as lenders prefer to see a lower credit utilization ratio. By assessing this ratio, a financial advisor can provide guidance on how to better manage your credit and potentially increase your credit score.

Rebuilding Credit

If your credit score has been negatively impacted by past mistakes or financial hardships, a financial advisor can assist you in rebuilding your credit. A key aspect of this process is devising a personalized plan tailored to your unique financial situation. This plan may involve strategies such as:

Creating a budget to manage your income and expenses effectively

Establishing a savings account to demonstrate financial stability

Setting up automatic payments for your bills to avoid missed payments

Working with creditors to negotiate lower interest rates or payment plans

Exploring options like secured credit cards or credit builder loans to establish positive credit history

Through careful guidance and support, a financial advisor can help you navigate the complexities of rebuilding your credit and set you on a path towards financial success.

Long-term Financial Wellness

Long-term financial wellness is essential for individuals looking to build a strong financial future and achieve their goals. Financial advisors play a crucial role in achieving this goal by providing expert guidance and personalized strategies to help individuals manage their debt effectively and work towards long-term financial stability. One of the key areas where financial advisors can make a profound impact is in helping individuals develop a solid plan for savings and investments, as well as retirement planning.

Savings And Investments

Creating a sound strategy for savings and investments is vital for mitigating debt and securing financial stability in the long run. Financial advisors work with individuals to develop tailored plans that allocate funds into diverse investment vehicles, such as stocks, bonds, and mutual funds, as well as high-yield savings accounts. These efforts help individuals to build a strong financial foundation that can be utilized to manage debt effectively while also growing their wealth over time.

Retirement Planning

Retirement planning plays a crucial role in long-term financial wellness. Financial advisors assist individuals in creating comprehensive retirement plans that align with their financial goals and debt management strategies. This includes guidance on retirement account contributions, investment choices, and retirement income projections to ensure that individuals can navigate through their retirement years without being burdened by debt.

Frequently Asked Questions For How Financial Advisors Can Help Debt?

Can A Financial Advisor Help You Get Out Of Debt?

Yes, a financial advisor can assist you in overcoming debt by offering expert guidance and creating effective financial strategies. They provide personalized solutions, helping you develop a realistic budget and explore debt repayment options that align with your goals. Their expertise can significantly improve your financial situation.

Can A Financial Advisor See Your Debt?

Yes, a financial advisor can see your debt as part of their analysis and assessment. They use this information to provide advice and suggest strategies to manage and reduce your debt effectively.

Who Is The Best Person To Talk To About Debt?

To get advice on debt, the best person to talk to is a financial advisor or credit counselor. They can provide expert guidance on managing debt and creating a plan to improve your financial situation.

Conclusion

Financial advisors play a crucial role in helping individuals tackle their debt and regain financial stability. By offering personalized advice and guidance, these professionals empower their clients to develop effective strategies for managing debt, creating budgets, and improving credit scores.

With their expertise and knowledge, financial advisors can provide invaluable support and assist individuals in achieving their long-term financial goals. Don’t let debt control your life – seek the assistance of a qualified financial advisor today.

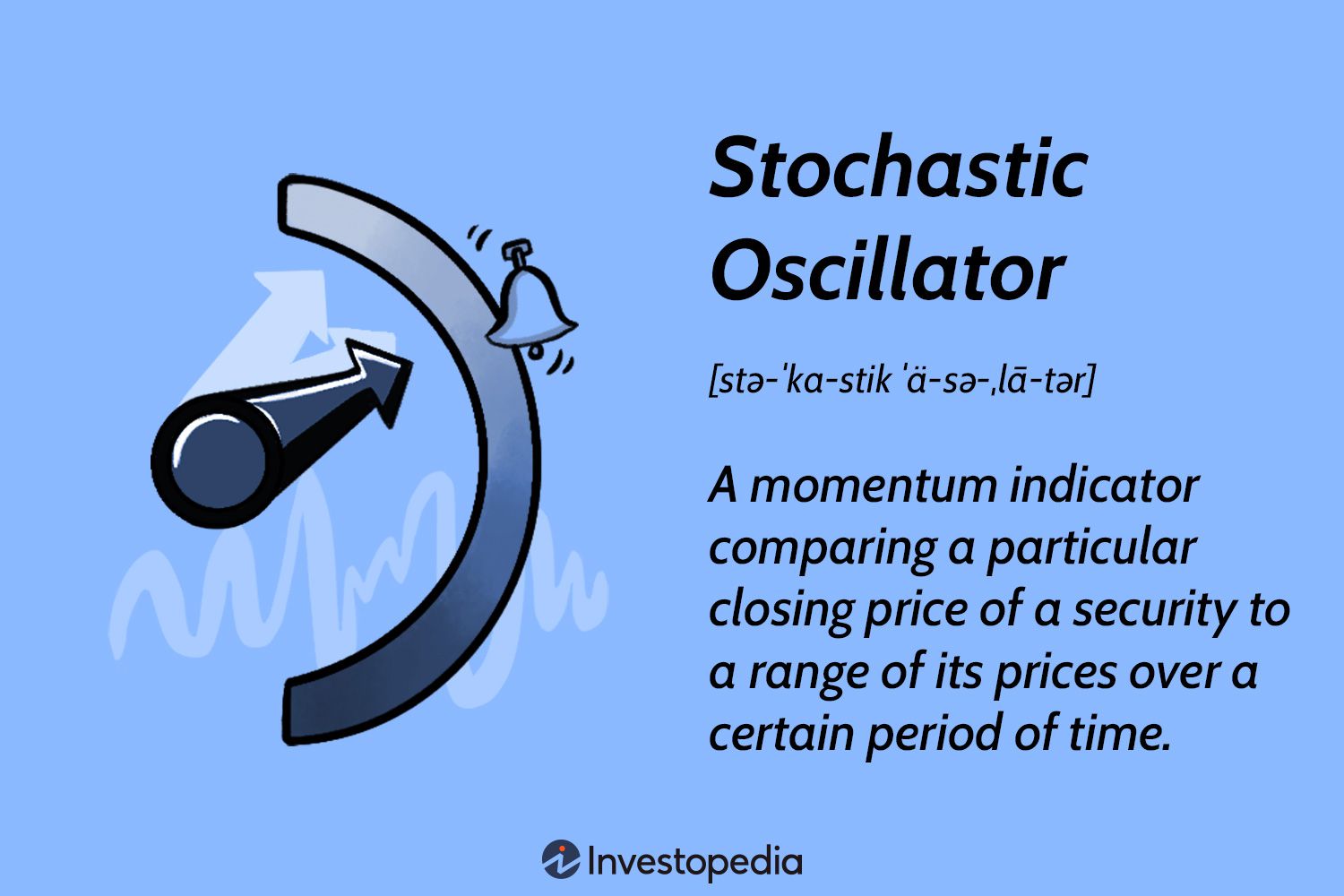

The stochastic oscillator is a popular technical analysis tool used by traders and investors to identify potential reversals in price trends. It is a momentum indicator that compares a security’s closing price with its price range over a specified period of time. The stochastic oscillator consists of two lines – %K and %D – that oscillate between 0 and 100.

Credit: www.investopedia.com

How Does the Stochastic Oscillator Work?

The stochastic oscillator is derived from the observation that as prices increase, closing prices tend to be closer to the upper end of the price range, while in a downtrend, closing prices tend to be closer to the lower end of the price range. By comparing the current closing price with the highest high and lowest low over a specific period, the stochastic oscillator determines the position within the range.

This information is then plotted on a chart and displayed as two lines: %K and %D. The %K line represents the current price relative to the range, while the %D line is the moving average of %K. Typically, a 14-day period is used for calculation, but this can be adjusted according to the trader’s preference.

Interpreting the Stochastic Oscillator

The stochastic oscillator generates signals based on overbought and oversold conditions. When the %K line crosses above the %D line, it is considered a bullish signal, indicating that the price may be poised to rise. Conversely, when the %K line crosses below the %D line, it is considered a bearish signal, suggesting that the price may be ready to decline.

Additionally, the stochastic oscillator is often used to identify overbought and oversold levels. Traditionally, values above 80 are considered overbought, while values below 20 are considered oversold. Traders may interpret these levels as potential reversal points, as overbought conditions can signal a potential decline, while oversold conditions may indicate a potential rise in price.

Credit: www.britannica.com

Using the Stochastic Oscillator in Trading

The stochastic oscillator is a versatile tool that can be used in various trading strategies. When combined with other technical analysis indicators, it can provide valuable insights into market conditions and potential opportunities. Here are a few ways traders use the stochastic oscillator:

Trend Confirmation:

Traders can use the stochastic oscillator to confirm the strength of a trend. If the oscillator’s lines are consistently moving in the same direction as the price trend, it suggests that the trend is strong and likely to continue. Conversely, if the oscillator’s lines start to diverge from the price trend, it may signal a potential reversal or weakening trend.

Reversal Confirmation:

The stochastic oscillator can also be used to confirm potential reversals. When the %K line crosses above the %D line in the oversold zone, it may indicate a bullish reversal signal. Conversely, when the %K line crosses below the %D line in the overbought zone, it may suggest a bearish reversal signal.

Divergence Analysis:

Divergence occurs when the price trend and the oscillator’s lines move in opposite directions. This can signal a potential reversal in the price trend. Traders look for situations where the price makes a new high or low, but the stochastic oscillator fails to reach a new high or low. This bearish or bullish divergence can indicate weakening momentum and a possible trend reversal.

Conclusion

The stochastic oscillator is a popular tool among traders and investors for identifying potential changes in price trends. By providing signals for overbought and oversold conditions, as well as confirming trends and possible reversals, it can be a valuable addition to any trading strategy. However, like any technical analysis tool, it is important to use the stochastic oscillator in conjunction with other indicators and analysis methods to make well-informed trading decisions.

Temporary car insurance provides short-term coverage for drivers, typically ranging from a day to a few weeks. It offers flexibility for unique situations, such as borrowing a vehicle or test driving a new car.

Temporary car insurance, also known as short-term car insurance, offers a convenient and flexible option for those who only require coverage for a brief period of time. Whether you need to borrow a friend’s car for a weekend road trip or want to provide temporary coverage for a visiting relative, this type of insurance can meet your needs without the commitment of a long-term policy.

We will explore the benefits and considerations of temporary car insurance, helping you make an informed decision when seeking short-term coverage for your vehicle.

What Is Temporary Car Insurance?

Temporary car insurance is a short-term auto insurance policy that provides coverage for a limited duration, typically ranging from a single day to several months. Unlike traditional annual policies, temporary car insurance offers flexibility, making it an ideal option for drivers who may only require coverage for a brief period.

How Is It Different?

Temporary car insurance is distinct from standard auto insurance in that it allows drivers to obtain coverage for a specific time frame, eliminating the need for a long-term commitment. This temporary solution is particularly advantageous for individuals who are borrowing or renting a vehicle for a short period, helping them avoid being tied to a standard annual policy.

When Is It Useful?

Temporary car insurance can be especially useful in a variety of situations, such as when individuals are borrowing a friend’s car, embarking on a road trip, or needing coverage for a temporary vehicle. It also proves beneficial for students returning home for holidays or individuals requiring immediate insurance for a newly purchased car.

Benefits Of Temporary Car Insurance

Temporary car insurance provides flexibility for short-term coverage without affecting existing policies. It is ideal for borrowing vehicles, test-driving, or moving house, offering peace of mind and cost-effective protection. This temporary option is easy to obtain and can be tailored to individual needs, making it a convenient choice for various situations.

Benefits of Temporary Car Insurance

Temporary car insurance offers several advantages for drivers who may need short-term coverage for various reasons. From flexibility to cost-effectiveness, this type of insurance provides practical solutions for different situations.

Flexibility

Temporary car insurance is designed to offer flexibility to drivers who require short-term coverage. Whether you need to borrow a friend’s car for a weekend getaway or drive a rental car during a vacation, temporary car insurance can be customized to suit your specific needs. This type of insurance allows you to adjust the length of coverage based on your requirements, providing the flexibility to stay insured only for the necessary duration.

Cost-effectiveness

One of the key benefits of temporary car insurance is its cost-effectiveness. Instead of committing to a long-term policy, you can opt for short-term coverage when you only need insurance for a limited period. This can result in significant cost savings as you only pay for the exact duration of coverage required. Additionally, temporary car insurance allows you to avoid annual policy fees and enables you to streamline costs based on your immediate needs.

In conclusion, temporary car insurance provides the flexibility to adapt coverage to your specific needs and offers a cost-effective alternative to long-term policies. Whether you need short-term coverage for a borrowed car or a rental vehicle, temporary car insurance presents a practical and economical solution.

How To Obtain Temporary Car Insurance

Are you searching for a flexible insurance option for your temporary driving needs? Temporary car insurance provides a convenient solution for short-term coverage, suitable for situations such as borrowing a car, Test driving a vehicle, or driving a rental car. In this guide, we’ll walk you through the requirements and process to obtain temporary car insurance.

Requirements

To obtain temporary car insurance, you need to meet certain requirements. Here are the basic criteria:

Age: Typically, you must be at least 21 years old.

Driving License: A valid driver’s license for the country in which you wish to secure the insurance.

Vehicle Information: Details of the vehicle you want to insure, including the registration number and the vehicle owner’s permission.

Process

The process of obtaining temporary car insurance is generally straightforward. Here’s an overview of the typical steps:

Research: Research and compare various insurance providers that offer temporary coverage.

Quote: Obtain a quote by providing the necessary details about yourself and the vehicle.

Application: Complete the application process by providing personal and vehicle information.

Payment: Make the required payment to activate the temporary insurance coverage.

Considerations Before Purchasing

Before purchasing temporary car insurance, there are several essential considerations to keep in mind to ensure the coverage meets your specific needs and requirements.

Coverage Options

When considering temporary car insurance, understanding the coverage options is essential. Liability coverage is mandatory in most states and covers damages to another person’s property or injury to another person in an at-fault accident. Collision coverage pays for damages to your car in an accident, regardless of fault. Comprehensive coverage protects against non-collision-related incidents, such as theft or natural disasters.

Duration

The duration of temporary car insurance should align with your specific needs. Whether you require coverage for a weekend getaway, a week-long business trip, or a month-long vacation, ensure that the policy’s duration provides adequate protection for the intended timeframe.

Frequently Asked Questions For Temporary Car Insurance

Is Temporary Car Insurance Legit?

Yes, temporary car insurance is legitimate. It provides short-term coverage for specific needs.

Can I Get Insurance For A Week?

Yes, you can get insurance for a week. Many insurance companies offer short-term policies to meet your temporary coverage needs.

Can You Get Temporary Car Insurance In The Us?

Yes, you can get temporary car insurance in the US. It’s commonly known as short-term auto insurance. Temporary car insurance offers coverage for a short period, usually from one day to a few months, providing flexibility for various situations.

Conclusion

Temporary car insurance provides a flexible solution for short-term coverage needs. It offers peace of mind for drivers who require temporary additional protection. With the convenience of easily accessible coverage, individuals can navigate unexpected situations with confidence. Explore the options available to find the right fit for your temporary insurance needs.

:max_bytes(150000):strip_icc()/Supertrend-indicator-7976167_final-1a52b8c33183472d89f20d99771ab042.png)