Debt can be overwhelming. Many people struggle with it every day. But help is available. Several organizations and programs offer debt relief. This article will guide you through them.

Credit: www.mdpi.com

Non-Profit Credit Counseling Agencies

Non-profit credit counseling agencies are a great place to start. They offer free or low-cost services. These services include budgeting help and debt management plans.

- National Foundation for Credit Counseling (NFCC)

- Financial Counseling Association of America (FCAA)

These agencies provide certified counselors. These counselors work with you to create a plan. They can negotiate with creditors on your behalf.

Debt Settlement Companies

Debt settlement companies can also help. They negotiate with your creditors. The goal is to reduce the amount you owe. This can be a risky option. It can negatively impact your credit score.

- Freedom Debt Relief

- National Debt Relief

Make sure to research these companies. Ensure they are reputable. Read reviews and check for any complaints.

Government Programs

The government offers several debt relief programs. These can help with student loans, mortgages, and taxes.

Student Loans

The U.S. Department of Education offers various programs. These include income-driven repayment plans and loan forgiveness programs.

- Income-Driven Repayment Plans

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

Mortgages

The U.S. Department of Housing and Urban Development (HUD) provides assistance. They offer programs to help avoid foreclosure.

- Home Affordable Modification Program (HAMP)

- Federal Housing Administration (FHA) loans

Taxes

The Internal Revenue Service (IRS) offers options to manage tax debt. These include installment agreements and offers in compromise.

- Installment Agreements

- Offers in Compromise

Debt Consolidation

Debt consolidation is another option. This involves combining multiple debts into one. This can simplify payments and lower interest rates.

There are several ways to consolidate debt:

- Personal loans

- Balance transfer credit cards

- Home equity loans

Consider speaking with a financial advisor. They can help you decide if debt consolidation is right for you.

Bankruptcy

Bankruptcy is a last resort. It can provide relief but has serious consequences. It can stay on your credit report for up to 10 years.

Types Of Bankruptcy

- Chapter 7 Bankruptcy: Liquidation

- Chapter 13 Bankruptcy: Repayment Plan

Consult with a bankruptcy attorney. They can help you understand your options.

Friends and Family

Sometimes, friends and family can help. They may be able to lend money or provide support. Be sure to discuss terms and repayment plans clearly.

:max_bytes(150000):strip_icc()/debt-settlement-cheapest-way-get-out-debt-v2-b624644919284cac8d8ca641e3a5ff21.png)

Credit: www.investopedia.com

Frequently Asked Questions

Who Offers Debt Relief Services?

Many organizations, including credit counseling agencies and debt settlement companies, offer debt relief services.

Is Debt Relief Available For Credit Card Debt?

Yes, debt relief programs can help manage and reduce credit card debt.

Can Non-profit Agencies Provide Debt Relief?

Non-profit credit counseling agencies often provide debt relief programs and financial education.

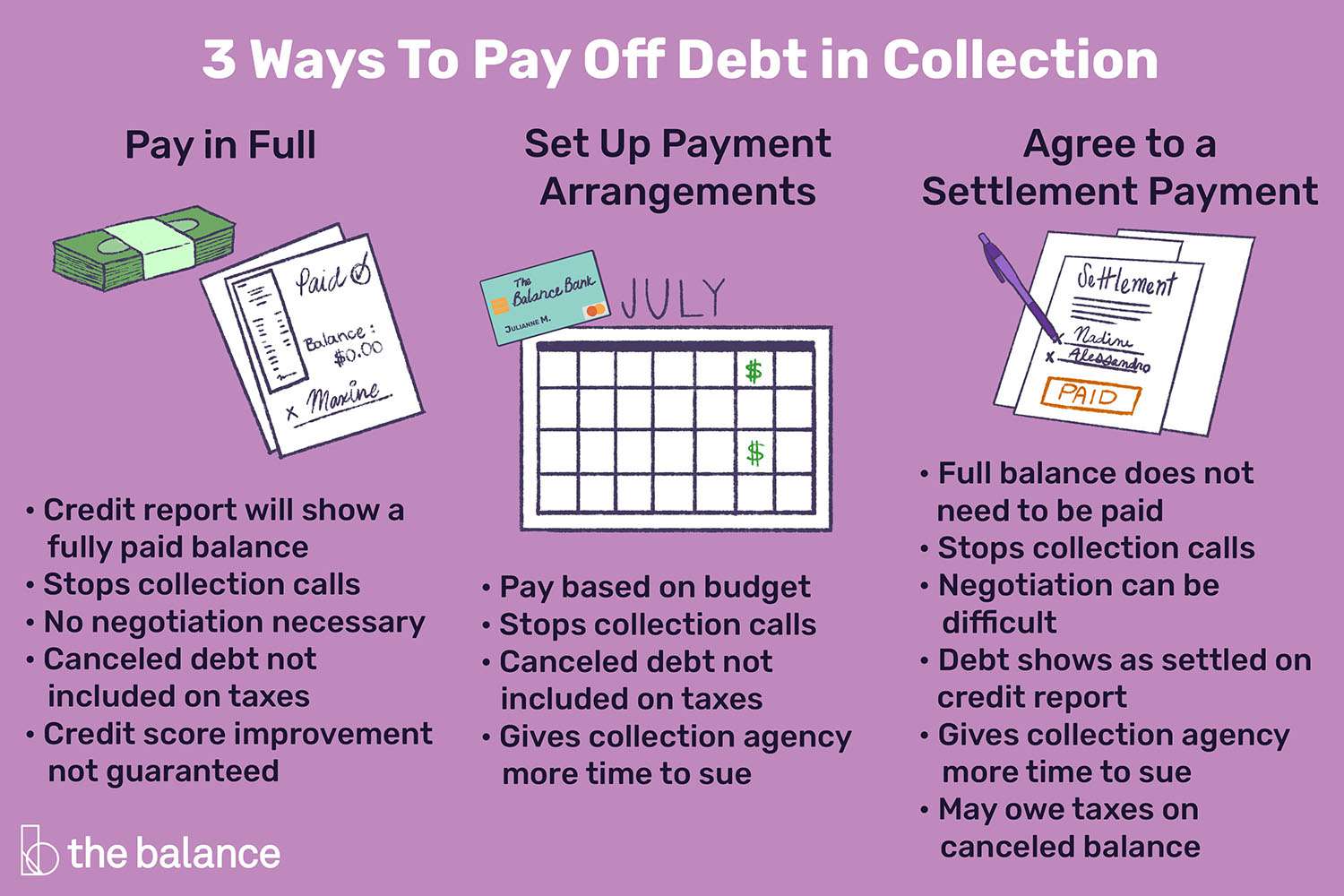

How Does Debt Settlement Work?

Debt settlement involves negotiating with creditors to pay a lump sum less than the total owed.

Conclusion

Debt relief is available from many sources. Non-profit agencies, debt settlement companies, and government programs can help. Debt consolidation and bankruptcy are other options. Friends and family may also provide support.

Take the time to research your options. Seek professional advice when needed. Debt relief can help you regain control of your finances.

:max_bytes(150000):strip_icc()/How-to-get-debt-relief-7514809_final-0a5d2bab416f4af2898e5458748ea6e9.png)

:max_bytes(150000):strip_icc()/what-happens-if-you-dont-pay-a-collection-960591-v3-5bbe02b546e0fb00510fde7e.png)