In the vast world of finance, interest rates play a pivotal role in determining the cost of borrowing and the return on investment. However, arriving at an appropriate interest rate for financial transactions can be complex. This is where the reference interest rate comes into play. In this blog post, we will delve into the concept of interest rate reference rates, their significance, and their impact on financial markets.

What is an Interest Rate Reference Rate?

An interest rate reference rate, also known as a benchmark rate or base rate, is a standardized interest rate that serves as a basis for determining the interest rates charged on various financial products and transactions. It acts as a common point of reference for lenders and borrowers, providing a transparent and consistent benchmark that reflects prevailing market conditions.

Importance and Applications:

Interest rate reference rates are integral to financial markets, fulfilling several crucial functions:

Pricing Loans: Banks and financial institutions use reference rates to determine interest rates on loans, mortgages, and other credit products. Lenders typically add a margin or spread to the reference rate based on factors such as credit risk, market conditions, and the borrower’s creditworthiness.

Valuing Fixed-Income Securities: Reference rates are essential in pricing and valuing fixed-income securities such as bonds, notes, and debentures. The interest rates on these securities often depend on a spread over a benchmark rate, allowing investors to assess their relative attractiveness.

Derivatives Pricing: Interest rate reference rates form a basis for pricing various interest rate derivatives such as interest rate swaps, options, and futures. These derivative contracts derive their value from fluctuations in reference rates, enabling market participants to manage interest rate risks.

Commonly Used Reference Rates:

A reference rate, or benchmark rate, is an interest rate that is used as the basis for setting other interest rates. Different types of transactions use different reference rate benchmarks, but some of the most common include:

SMART (Six-month Moving Average Rate of Treasury Bills) by Bangladesh Bank (BB): The SMART is a six-month moving average of the interest rates on treasury bills issued by the Bangladesh Bank. It is used as a benchmark rate for short-term loans and other financial products. The current SMART rate is 7.10%, which is almost unchanged from the previous month(7,13% for May 2023).

London Interbank Offered Rate (LIBOR): Historically, LIBOR was one of the most widely used reference rates, serving as a benchmark for short-term interbank lending. However, due to concerns about its integrity, it is being phased out and replaced by alternative reference rates.

Euro Interbank Offered Rate (EURIBOR): Similar to LIBOR, EURIBOR serves as the benchmark rate for euro-denominated loans and financial products within the Eurozone.

US Treasury Yield Curve: The US Treasury Yield Curve represents the interest rates on US government bonds with different maturities. It provides a reference for pricing various fixed-income securities and serves as a key indicator of market sentiment.

The Secured Overnight Financing Rate (SOFR) is a benchmark interest rate used in the United States to reference short-term U.S. dollar-denominated loans. It is based on the interest rates on overnight repurchase agreements (repos) that are collateralized by U.S. Treasury securities.

Regulatory Oversight and Reforms:

In recent years, there has been a significant shift in the landscape of interest rate reference rates due to regulatory reforms and the need for more robust and reliable benchmarks. Authorities around the world have been working on transitioning from existing reference rates like LIBOR to alternative rates based on more transactional data and stronger governance.

Conclusion:

Interest rate reference rates are vital components of the financial ecosystem, providing a standardized benchmark for pricing various financial products. They contribute to transparent and efficient markets, enabling lenders, borrowers, and investors to make informed decisions based on prevailing market conditions. As the financial landscape continues to evolve, the transition to alternative reference rates ensures the integrity and stability of interest rate benchmarks, reinforcing the foundation of global finance.

The “six-month moving average rate of treasury bills (SMART)” is a new monthly reference lending rate formula introduced by Bangladesh Bank on June 19, 2023, to be implemented in July 2023. It replaced the single-digit 6%-9% interest cap regime. The rate is fixed based on the weighted average rate of a six-month treasury bill plus a premium/margin.

The current margin is a maximum of 3.75%for banks and 5,75% for non-banking financial institutions since the last week of November.

The margin was up to 3% for banks and 5% for non-banking financial institutions at first when declared in June. Later, in October, it was increased to 3.50% for banks and 5,50% for financial institutions

Existing SMART Rate by BB

The Rate is from the Bangladesh Bank Website:

If we want to understand the SMART framework, we may take an example.

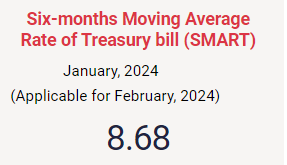

The prevailing Short-term Moving Average Rate of the Treasury Bill (SMART) is 8.68% as declared by BB applicable for February 2024. According to this framework, Banks can charge a maximum of 12.43% while FIs will be able to charge a 14.43% maximum on their credits. In the case of CMSMEs and consumer Loans, Banks can charge a maximum of 13.43% while Agricultural and Pre-Shipment Export Loans will be charged an 11.43% maximum.The below table may help with the calculation:

Particular

Lending Rates

Banks

SMART+ max 3.75% margin (Max 12.43%)

CMSMEs & Consumer Loans

An additional fee of up to 1% may be charged. (Max 13.43%)

Agricultural and Pre-Shipment Export Loans

SMART+ max 2.75% margin (Max 11.43%)

FIs

SMART+ max 5.75% margin ( Max 14.43%) CMSMEs & Consumer Loans (Max 15.43% including 1% charge)

Credit card loans

20% as before (not tagged with SMART)

The previous rate was as follows:

The smart rate will be reviewed every six months, and it may be adjusted up or down depending on market conditions.

SMART Reference Lending Rate in Bangladesh

The smart rate is very different from the previous single-digit lending rate cap, which was set in 2019. The Bangladesh Bank has said that the new rate is necessary to control inflation and ensure the stability of the financial system.

The SMART Reference Lending Rate is a new lending rate mechanism introduced by the Bangladesh Bank in July 2023. It is based on the six-month moving average rate of treasury bills (T-bills). Banks can add up to 3.75 percentage points to the SMART rate to fix their lending rates.

The current SMART rate for February 2024 is 8.68%. This means that banks can lend at a maximum rate of 13.43%, including the addition of a 1% supervision fee. The lending rate for agricultural and rural loans is 11.43%, and the lending rate for credit cards remains unchanged at 20%.

The SMART rate is reviewed every month, and it is expected to be adjusted in line with market conditions.

The SMART Reference Lending Rate is a more market-based and transparent lending rate mechanism than the previous system, which was based on the repo rate. It is expected to help reduce the spread between lending and deposit rates, and it provides banks with more flexibility in setting their lending rates.

Bangladesh Bank, in its Monetary Policy Statement for the July-December 2023 period, focuses more on being market-driven in both interest rate and exchange rate. As a step towards removing restrictions on banks’ lending and investment activities and setting up market-oriented interest rates, BB has introduced a new method of reference rate called SMART (Short-term Moving Average Rate of Treasury-Bill). The prevailing lending interest rate cap at 9% will be lifted from the beginning of July. The new interest rate framework is said to be market-driven in the sense that the offers for the yield on 182-Day T-bills usually come from participating financial institutions/individuals through primary dealers and the yield is not set by BB. Banks will have space to add margin depending on their different factors.

In this method, BB publishes the rate on the first day of every month on its website. The calculation methodology will take into account the yield of the 182-day Treasury bill. This reference rate will be active on 01-July-2023 and the lending interest cap will be set in the following manner.

SMART Reference lending rate calculation

The calculation of the smart rate by BB is a 3-step process shown as follows:

Weighted average rate of a six-month treasury bill

Firstly, BB will calculate the weighted average yield of the 182-Days T-bills on a weekly basis. The weighted average rate of a six-month treasury bill is the average interest rate that commercial banks pay when they borrow money from the Bangladesh Bank through treasury bill auctions. The weighted average rate is calculated by taking the total amount of money borrowed by commercial banks and dividing it by the total interest paid. It is done by the Debt Management Department, BB.

Premium

In the following step, BB will calculate a simple average of the four weeks’ weighted average yields every month. The premium is a margin that is added to the weighted average rate to determine the smart rate for loans and advances. The premium is intended to compensate commercial banks for the risks associated with lending money.

The premiums to be added are:

3.75% for banks (3.75% + 1% supervision fee can be added to personal, car, and consumer loans)

2.75% for Agricultural and Pre-Shipment Export Loans

5.75% for FIs

Lending rate

In the final stage, BB will compute the moving average of the yields over the past six months and this rate will be made public on the first working day of each month through the BB website. The lending rate is the rate of interest that commercial banks charge their customers when they borrow money. The lending rate is calculated by adding the weighted average rate and the premium.

Here are some of the factors that will be considered when setting the smart rate:

The inflation rate

The interest rate environment in other countries

The demand for and supply of credit in the domestic market

The stability of the financial system

The smart rate is reviewed every six months, and it may be adjusted up or down depending on market conditions. The Bangladesh Bank will consider several factors when setting the smart rate, including the inflation rate, the interest rate environment in other countries, the demand for and supply of credit in the domestic market, and the stability of the financial system.

Reference rates worldwide

All over the world, there are reference rates that commercial banks follow as a base rate for their lending operation. They may add the required premium or several premium factors to finalize their domestic lending rate. The rates may vary from entity to entity, individual to individual depending on various factors. In some countries, the central bank policy rate acts as the reference rate for commercial banks. For example, the Fed Funds Rate, the policy rate in the USA, is the reference rate in the USA.

For international lending operations, the LIBOR rate used to be the popular one. As the LIBOR phase-out is in transition, SOFR (Secured Overnight Financing Rate) for USD lending, SONIA (Sterling Overnight Index Average) for GBP lending, EONIA (Euro Overnight Index Average) for EUR loans, TONAR (Tokyo Overnight Average Rate) for JPY lending are becoming popular nowadays in replacement for LIBOR rate of different currencies.

The Story and History of SMART

Banks can charge a maximum of 12.43 percent interest on loans for now (a 1% charge can be added for CMSME and Consumer loans). The rate will be 14.43 percent (a 1% charge can be added for CMSME and Consumer loans) for non-bank financial institutions, meaning the spread between the lending and deposit interest rates will be a maximum of 3.75 percentage points.

SMART Launched

To trace the history, the Banking Regulation and Policy Department of Bangladesh Bank published a circular for the banks on June 19, 2023, about the interest rate with a special focus on the market-based rate with a new concept of SMART. It was applicable from July 2023. The prevailing lending interest rate cap at 9% is to be lifted from the beginning of July 2023.

Soon after the circular for banks, on June 20, 2023, the Department of Financial Institutions and Markets, Bangladesh Bank published another circular regarding interest rates for the FIs.

FIs can let their depositors enjoy interests of up to 2% above the SMART reference rate on deposits, and 5% above the SMART rate for loans and advances.

On November 27, 2023, the Banking Regulation and Policy Department of Bangladesh Bank published another circular for the banks allowing more 25 basis points on margin. So, banks now can add 3.75% margins to the existing SMART rate. So, the maximum rate now maybe 8.68% + 3.75%=12.43%. (11.43% for Agricultural and Pre-Shipment Export Loans whereas 13.43% for CMSMEs and Consumer loans as a 1% supervision charge can be applied)

Consequently, on November 29, 2023, the Department of Financial Institutions and Markets, Bangladesh Bank published another circular regarding interest rates for the FIs.

FIs can let their clients enjoy interests of up to 2.75% above the SMART reference rate on deposits, and charge 5.75% above the SMART rate for loans and advances.

As MPS mentioned, this new interest rate framework will act as a catalyst to make the interest rate dynamics in the market act freely as banks will be able to adjust the lending rate depending on market variations and other considerations. This will help efficient credit allocation of banks’ funds and expedite the competitiveness among banks. The interest rate will also be able to capture inflation expectations which will be incorporated while calculating SMART and it is said to have an impact to hold the rein of inflation.

It is mention-worthy that the SMART is more complicated than the previous single interest rate cap and it is variable in nature. The rate will vary every month. This might make some complications in calculating the end lending interest rate of commercial credits.

However, as per the circular, the interest rate cannot be changed within six months of its imposition. This means that even if the interest rate increases, the bank cannot raise it for existing customers.

The band or the corridor is too narrow to consider as market-aligned. Nonetheless, this move to make the interest rate free from the cage and to pave the way to have a rein on runaway inflation is appreciable.

Why did BB introduce a SMART Rate?

Bangladesh Bank recently introduced a SMART lending reference rate (SLRR) for banks to set their lending rates based on market conditions. This new system replaces the traditional base rate system. In this article, we will discuss the ten reasons why Bangladesh Bank introduced the SLRR system to list some of the potential advantages of the smart rate:

1. To Encourage Banks to Offer Competitive Rates

Under the traditional base rate system, banks set their lending rates based on their cost of funds and overheads. This led to high-interest rates, making it difficult for borrowers to obtain loans. By introducing the SLRR system, Bangladesh Bank hopes to reduce lending rates and make loans more affordable for businesses and individuals.

2. To Promote Financial Inclusion

By reducing lending rates, the SLRR system aims to encourage more people to take out loans, promoting financial inclusion across the country. Small and medium enterprises (SMEs) and low-income individuals, who previously struggled to access loans due to high-interest rates, will now be able to obtain credit at more affordable rates.

3. To Improve the Transparency of Lending Rates

The SLRR system is based on market conditions, which means that lending rates will be transparent and visible to borrowers. This increased transparency will help borrowers make better-informed decisions about their borrowing requirements.

4. To Support Economic Growth

By making loans more affordable, the SLRR system will encourage businesses to invest in new projects and expand existing ones, leading to job creation and economic growth.

5. To Reduce the Dependence on Informal Sources of Credit

Many low-income individuals and small businesses in Bangladesh have no choice but to turn to informal lenders for credit, as they cannot access formal loans due to high-interest rates. The SLRR system aims to reduce the dependence on these informal sources of credit by making formal loans more affordable.

6. To Encourage Banks to Adopt Good Lending Practices

The SLRR system takes into account the risk profile of borrowers, encouraging banks to adopt good lending practices and assess the creditworthiness of borrowers before granting loans.

7. To Increase Competition in the Banking Sector

The SLRR system aims to promote competition among banks by encouraging them to offer lower lending rates. This increased competition will benefit borrowers and promote innovation in the banking sector.

8. To Align Lending Rates with Market Conditions

Under the traditional base rate system, lending rates were not always aligned with market conditions, leading to high-interest rates even when market rates were low. The SLRR system aims to correct this by setting lending rates based on market conditions.

9. To Promote Financial Stability

The SLRR system takes into account the risks associated with lending, promoting financial stability by encouraging banks to adopt prudent lending practices.

10. To Align with International Best Practices

The SLRR system aligns with international best practices, making it easier for Bangladesh to attract foreign investment and integrate with the global economy.

11. To tame inflation.

The Bangladesh Bank believes that the smart rate will help to control inflation by making it more expensive for businesses to borrow money. This will discourage businesses from borrowing money and investing, which will help to slow down the economy and bring down inflation.

12. To ensure the stability of the financial system.

The Bangladesh Bank believes that the smart rate will help to ensure the stability of the financial system by making it more difficult for banks to make risky loans. This will help to prevent a financial crisis, which could have a devastating impact on the economy.

13. To make the lending rate more market-driven.

The previous lending rate cap was set by the Bangladesh Bank, which meant that commercial banks were not free to set their own lending rates. The smart rate will be based on market conditions, which will give commercial banks more flexibility in setting their lending rates. This could lead to more competition among banks, which could benefit consumers by lowering the cost of credit.

The introduction of the SMART lending reference rate system by Bangladesh Bank is a positive step towards promoting financial inclusion, encouraging good lending practices, and supporting economic growth. The system aims to reduce lending rates, increase transparency, and align with international best practices, making it easier for borrowers to access credit and encouraging banks to compete on rates.

Impacts of the SMART Rate

The smart rate is a new tool that the Bangladesh Bank will use to manage the country’s monetary policy. It remains to be seen how effective the rate will be in achieving its objectives. However, it is a significant departure from the previous lending rate cap, and it could have a major impact on the availability and cost of credit in Bangladesh.

The cost of credit could increase, which could make it more difficult for businesses to borrow money and invest. This could slow down the economy and lead to job losses.

The availability of credit could decrease, as banks may be less willing to lend money at higher interest rates. This could make it more difficult for businesses and consumers to access credit, which could hurt the economy.

The smart rate could lead to more competition among banks, as they will be trying to attract customers by offering lower interest rates. This could benefit consumers by lowering the cost of credit.

More market-based and transparent lending rate mechanism. The SMART rate is based on the six-month moving average rate of treasury bills, which is a more market-based indicator than the previous lending rate regime, which was based on the repo rate. This means that the SMART rate is more responsive to changes in market conditions, and it is also more transparent, as it is based on an observable market rate.

Reduced spread between lending and deposit rates. The SMART rate is expected to help reduce the spread between lending and deposit rates. This is because the SMART rate is more market-based, which means that it is more likely to reflect the true cost of funds for banks. As a result, banks will be less likely to mark up their lending rates above the cost of funds, which will help to narrow the spread between lending and deposit rates.

More flexibility for banks in setting lending rates. The SMART rate provides banks with more flexibility in setting their lending rates. This is because banks can add up to 3 percentage points to the SMART rate to fix their lending rates. This flexibility will allow banks to better compete for customers and to offer more competitive lending rates.

Improved efficiency of the lending market. The SMART rate is expected to improve the efficiency of the lending market. This is because the SMART rate is more market-based and transparent, which will make it easier for borrowers and lenders to find each other. As a result, the SMART rate is expected to help to reduce the cost of credit for borrowers and to improve the efficiency of the lending market.

Improved risk management by banks. The SMART rate is based on the six-month moving average rate of treasury bills, which is a more stable indicator than the repo rate. This means that the SMART rate is less likely to fluctuate sharply, which will make it easier for banks to manage their risk. As a result, banks will be less likely to suffer losses due to unexpected changes in interest rates.

Overall, the impact of the smart rate is uncertain. It could have both positive and negative effects on the economy. Only time will tell how effective the rate will be in achieving its objectives. Reference rates are constantly evolving as the financial markets change. For example, the LIBOR is being phased out and replaced by new reference rates, such as the Secured Overnight Financing Rate (SOFR). This is because LIBOR has been criticized for being manipulated by banks and for not being a reliable indicator of the true cost of borrowing money.

Challenges of the SMART Rate

The smart rate is a new monetary policy tool that has the potential to both benefit and challenge the Bangladeshi economy. Some of the potential challenges of the smart rate include:

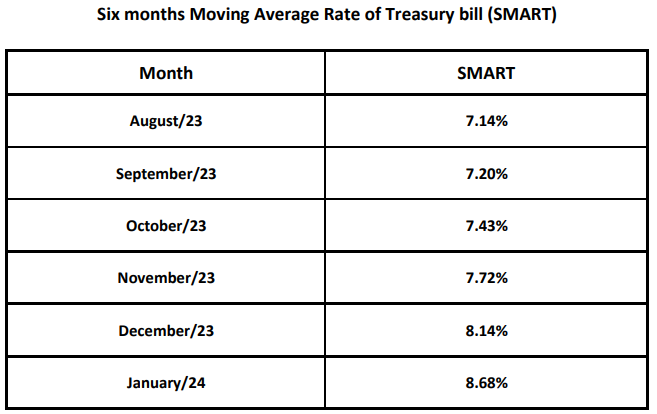

Increased cost of credit: The smart rate is based on the weighted average rate of a six-month treasury bill, which is currently at 7.72%. This means that the smart rate is likely to be higher than the previous lending rate cap of 9%. This could make it more expensive for businesses and consumers to borrow money, which could slow down economic growth.

Decreased availability of credit: If the smart rate is too high, banks may be less willing to lend money. This could make it more difficult for businesses and consumers to access credit, which could also slow down economic growth.

Increased volatility in the financial markets: The smart rate is a market-based tool, which means that it is subject to change based on market conditions. This could lead to increased volatility in the financial markets, which could make it more difficult for businesses and investors to plan for the future.

Difficulties in managing the tool: A SMART rate is a new tool, and it is not yet clear how the Bangladesh Bank will be able to effectively manage it. If the Bangladesh Bank is not able to manage the tool effectively, it could lead to unintended consequences for the economy.

In addition to the challenges mentioned above, there are a few other potential challenges that could arise from the implementation of the smart rate. These include:

Lack of transparency: The smart rate is a complex calculation, and it is not clear how the Bangladesh Bank will calculate it. This lack of transparency could make it difficult for businesses and consumers to understand how the smart rate will affect them.

Inflationary pressures: If the smart rate is too high, it could lead to inflationary pressures. This is because businesses may pass on the higher interest costs to consumers in the form of higher prices.

Negative impact on the financial sector: The smart rate could hurt the financial sector. This is because banks may be less willing to lend money if the smart rate is too high. This could lead to a decrease in lending, which could hurt economic growth.

It is important to note that these are just potential challenges. The actual impact of the smart rate will depend on several factors, including how the Bangladesh Bank manages the tool and how the market reacts to it.

Is SMART really smart?

There are several reasons why the SMART Reference Lending Rate (SRLR) is considered to be “smart.” First, the SRLR is based on a weighted average of the lending rates of commercial banks. This means that it is more reflective of the actual cost of lending in the market, as opposed to the previous lending rate, which was set by the Bangladesh Bank.

Second, the SRLR is reviewed every month, which means that it can be adjusted more quickly to changes in market conditions. This can help to ensure that the SRLR remains a fair and competitive lending rate.

Third, the SRLR is transparent and publicly available. This means that businesses and consumers can easily see what the SRL is, and they can use this information to make informed decisions about their borrowing.

Overall, the SMART Reference Lending Rate is a positive development for the Bangladeshi economy. It is expected to help to reduce lending costs, improve the efficiency of the financial system, and promote economic growth.

However, some argue that the SRLR is not really “smart” after all. They also argue that the SRL is not responsive enough to changes in market conditions.

Only time will tell whether the SRLR is truly a “smart” lending rate. However, the early signs are promising, and the SRLR will likely have a positive impact on the Bangladeshi economy.

Last Lines

The SMART Reference Lending Rate is a new lending rate mechanism in Bangladesh that is based on the six-month moving average rate of treasury bills. It is more market-based and transparent than the previous lending rate regime, and it is expected to help reduce the spread between lending and deposit rates. The current SMART rate for February 2024 is 8.68%, and banks can add up to 3.75% points to this rate to fix their lending rates whereas FIs can add 5.75%.

To budget for a disability, identify necessary expenses and prioritize them accordingly. Allocate funds for unexpected costs and consider seeking financial assistance if needed.

Living with a disability can come with financial challenges that require careful budgeting. From medical expenses and assistive technology to transportation and home modifications, it’s essential to identify necessary expenses and prioritize them accordingly. Additionally, it’s important to allocate funds for unexpected costs and plan for potential changes in income or living situations.

Seeking financial assistance through government programs, community organizations, or crowdfunding can also be helpful. By creating a comprehensive budget, those living with a disability can better manage their finances and ensure their needs are being met.

Credit: www.diabetesadvocacy.com

Understand Your Expenses

Breakdown Essential Expenses

When budgeting for a disability, it’s essential to prioritize your expenses. You must identify your essential expenses, ensuring that these costs are covered before anything else. This should include:

Housing and utilities: This is typically the most substantial expense most individuals face. You’ll need to budget for rent/mortgage, electricity, gas, water, and other utilities necessary for daily living.

Food: You must budget for groceries or other food expenses, including any specialized dietary requirements.

Transportation: This must include transportation costs specific to your disability, such as a wheelchair accessible vehicle or other modifications.

Medical and health expenses: Medical costs can vary widely, and it’s essential to ensure that you’re adequately covered and have the right insurance in place. This could include medication, medical equipment, and caregiver costs.

Insurance: You’ll need to budget for insurance, including life, health, and disability insurance.

Categorize Non-Essential Expenses

Once you’ve identified your essential expenses, it’s time to categorize your non-essential expenses, which include any discretionary spending. Examples of such expenses include:

Entertainment: This includes expenses like movies, concerts, and other recreational activities.

Dining out: This refers to eating out in restaurants or ordering takeout.

Shopping: This includes any non-essential shopping purchases, such as clothing or electronics.

Travel: This includes any vacation or travel expenses that aren’t essential.

It’s essential to be honest with yourself about what you can realistically afford to spend on non-essential expenses. You may have to cut back on these costs to free up more money for essential expenses.

Evaluate The Impact Of Disability On Expenses

Having a disability can significantly impact your expenses. You’ll need to factor in additional expenses related to your disability, such as:

Medical expenses: These can include medical bills, hospital stays, physical therapy, and occupational therapy.

Mobility equipment: This includes wheelchairs, walkers, and other mobility aids that may need to be modified or customized to fit your needs.

Home modifications: This includes any updates or changes required to make your home more accessible, such as installing a ramp or widening doorways.

Caregiver costs: If you require the assistance of a caregiver, you’ll need to factor in these costs when budgeting for your disability.

It’s important to consider the long-term impact of your disability when budgeting. Be mindful of any additional expenses that may arise, and try to plan for them in your budget. Remember, budgeting for a disability requires careful planning, but with the right strategy, you can manage your finances and maintain a good quality of life.

Explore Disability Benefits

Budgeting for a disability can be a challenging task. However, exploring available disability benefits can help alleviate financial strain. There are several different types of disability benefits available. In this blog post, we’ll explore the different types of disability benefits and how to access them.

Research Government Benefits

The government offers several types of disability benefits that may be available to people with disabilities. These benefits include:

Supplemental security income (ssi): Ssi is a program for low-income individuals who are blind, disabled, or over the age of 65. Ssi provides monthly cash payments.

Social security disability insurance (ssdi): Ssdi provides monthly cash payments to individuals who have a disability and have worked for a certain number of years.

Medicare: Medicare is a federal health insurance program for people who are 65 or older, or for people under 65 who have a disability.

Medicaid: Medicaid is a federal and state-funded program that provides healthcare coverage to low-income individuals who have a disability.

To apply for government benefits, individuals must complete an application process with the appropriate government agency.

Insurance Benefits

In addition to government benefits, some people with disabilities may be eligible for insurance benefits. These benefits include:

Private insurance: Private insurance plans may cover the costs of certain medical treatments and services.

Worker’s compensation: If an individual was injured on the job, they may be eligible for worker’s compensation benefits.

Long-term disability insurance: Long-term disability insurance may provide monthly cash payments to individuals who are unable to work due to a disability.

To access these benefits, individuals should contact their insurance provider or employer.

Healthcare Accessibility Benefits

There are also several healthcare accessibility benefits available to people with disabilities. These benefits include:

Accessible transportation: Some cities provide transportation programs for people with disabilities.

Assistive technology: Assistive technology, such as hearing aids or wheelchairs, may be covered by insurance.

Accessible housing: Some cities offer accessible housing programs for people with disabilities.

To access these benefits, individuals should contact their local government or healthcare provider.

Social Security Disability Insurance Benefits

Social security disability insurance (ssdi) is a federal program available to people who have a disability and have worked for a certain number of years. To apply for ssdi, individuals must complete an application process with the social security administration.

Budgeting for a disability can be a challenging task. However, by exploring available disability benefits, individuals can relieve financial stress. There are several different types of disability benefits available, including government benefits, insurance benefits, and healthcare accessibility benefits. By researching these benefits and completing the necessary application processes, individuals with disabilities can access the resources they need to live their best lives.

Assess Your Income

Budgeting for a disability can be a daunting and overwhelming task. The process becomes even more challenging when you have little information about how to assess your income. In this section, we will explore tips and tricks for assessing your income, exploring alternative sources of income as a person with a disability.

Calculate Monthly Income

Calculating your monthly income is a critical step when budgeting for a disability. Below are some key points to consider when assessing your income:

Employment income: If you are employed, your income can be structured in several ways, such as hourly, weekly, bi-weekly, or monthly. Make sure you understand all components of your income, such as base salary, overtime, or tips.

Government benefits: If you receive benefits from the government, such as social security disability insurance (ssdi) or supplemental security income (ssi), you need to understand the amount you receive monthly and how it is impacted by other income.

Pensions and retirement: If you receive a regular payment from a pension plan or retirement account, make sure you understand the amount you receive monthly and if it is taxable.

Other income: If you have other forms of income, such as rental income or alimony, make sure you understand how much you receive monthly.

Explore Alternative Sources Of Income

Sometimes, your income may not be sufficient to meet all your financial needs, especially as a person with a disability. The following are alternative sources of income to consider:

Work from home: With the rise of remote work, more companies are offering work from home opportunities, which can be ideal for persons with disabilities.

Freelance and consulting: If you have marketable skills, such as writing, accounting, programming, or graphic design, you can consider offering freelance or consulting services.

Online business: You can start an online business selling products or offering services, such as tutoring, coaching, or virtual assistance.

Side hustle: You can explore other ways to earn income, such as ride-sharing, pet sitting, or food delivery.

Assessing your income is a crucial step in budgeting for a disability. It allows you to understand your financial situation, identify gaps, and explore alternative sources of income. By following the tips and tricks provided in this section, you can effectively assess your income and create a budget that works for you.

Create A Realistic Budget

Creating A Realistic Budget For Disability

Coping with a disability can be an overwhelming experience, and budgeting can be especially challenging. While it might seem daunting, with proper planning and a realistic approach, you can create a budget that works for you. Here are some tips and tricks on how to create a realistic budget when dealing with a disability.

Define Spending Limits

When creating a budget, there are two separate terms you need to consider: income and expenses. First, you need to define your monthly income. Include everything you earn, such as salary, disability payments, or any other form of earnings. Once you have a clear idea of your monthly income, you can then begin to track your expenses.

Prioritize Essential Expenses

Your essential expenses are what you need to survive. These items include housing, food, transportation, and medical expenses. Other essential expenses may be specific to your disability and should be factored into your budget. For example, if you have mobility issues, you may need to install ramps or handrails in your home.

List down all your essential expenses, and make sure that your income is sufficient to cover them.

Trim Non-Essential Expenses

Once you have prioritized your essential expenses, you can start trimming non-essential expenses. Take a closer look at your budget and determine which expenses you can eliminate. Non-essential expenses might include entertainment, dining out, or subscriptions you no longer use.

Allocate Budget To Disability Related Expenses

A disability often comes with additional financial burdens. These may include assistive devices, medication, or specialized care. Make sure to include these disability-related expenses when budgeting. Additionally, look for ways to reduce these expenses, such as through insurance or utilizing government programs.

Creating a realistic budget when dealing with a disability requires careful planning and prioritization. Identify your essential expenses, trim non-essential ones, and allocate budget to disability-related expenses. The key is to make a budget that works for you, one that is flexible enough to accommodate your life’s changes while keeping your disability’s financial impact manageable.

Implement Money Management Tools

If you have a disability, managing your finances can be a challenge. Fortunately, there are several money management tools available to help you budget successfully. From financial planning software to disability assistance programs, implementing these tools can improve your financial situation.

In this post, we will go over the different options you have to budget for a disability.

Financial Planning Software

Financial planning software is a great option for those who want to keep track of their expenses. This type of software can help you create a budget and keep track of your spending. Here are some key benefits of using financial planning software:

Helps you create a budget based on your income and expenses.

Syncs with your bank account to track your spending automatically.

Provides you with detailed reports on your spending habits.

Offers suggestions for ways to improve your financial situation.

Online Budgeting Tools

In addition to financial planning software, there are many online budgeting tools available. These tools can help you track your spending and create a budget that works for you. Here are some of the benefits of using online budgeting tools:

Easy to use and accessible from anywhere with an internet connection.

Can help you identify areas where you are overspending.

Offers reminders for bills and upcoming expenses.

Can be used to track your progress towards financial goals.

Disability Assistance Programs

There are several disability assistance programs available that can help you manage your finances. These programs can provide you with financial assistance and support services. Here are some of the benefits of using disability assistance programs:

Can provide financial assistance for medical expenses and other related costs.

Offers support services, such as help with finding employment.

Provides counseling services to help you manage your finances and create a budget.

Offers education and training programs to help you improve your financial situation.

Financial Advisor

If you are having difficulty managing your finances, working with a financial advisor may be a good option. A financial advisor can provide you with guidance and advice on how to manage your money. Here are some benefits of working with a financial advisor:

Offers personalized advice based on your financial situation.

Can help you create a budget and stick to it.

Provides guidance on effective money management strategies.

Can help you plan for the future and achieve your financial goals.

Implementing money management tools is essential when budgeting for a disability. Financial planning software, online budgeting tools, disability assistance programs, and financial advisors are all great options to help you successfully manage your finances. By using these tools, you can improve your financial situation and achieve your financial goals.

Plan For Emergencies

People with disabilities must budget for unforeseen situations. This is especially crucial because disabilities may lead to unexpected medical expenses or even job losses. Therefore, it is essential to create a budget that contains enough funds to cover emergencies. Here are some ways to create an emergency fund:

Create An Emergency Fund

Creating an emergency fund can be a lifesaver during unexpected events. In order to have a functional emergency fund:

Set aside an amount of money monthly towards the emergency fund.

Ensure that you have at least six months of living expenses in the emergency savings account.

Label the account as an emergency fund to restrict any unnecessary expenses.

Establish A Savings Plan

If living with a disability, it is important to adopt a savings plan to ensure financial security. By having a savings plan, you can build wealth for yourself and cover future expenses, including disability-related costs. Here are some tips to establish a savings plan:

Create a savings plan to meet specific financial goals, such as paying off debt or purchasing a property.

Keep track of your expenses to help you identify areas where you can reduce your spending.

Discuss your savings goals with your financial advisor to create a personalized plan.

Enroll For Short-Term And Long-Term Disability Insurance

Disability insurance helps to cover expenses in the event of a disability-related situation. Short-term insurance provides financial assistance in situations where the disability takes a short time to recover, while long-term insurance provides benefits for a longer period of time.

Here are some tips to get disability insurance:

Do research and compare different insurance options to help you choose the best insurance cover for your needs.

Ensure that you obtain a policy that covers long-term disability.

Consider purchasing any additional riders to complement your policy, such as accidental death or dismemberment insurance.

Budgeting can be an overwhelming process for people with disabilities. However, creating an emergency fund, establishing a savings plan, and getting disability insurance can aid in financial security for unforeseen emergencies.

Re-Evaluate And Adjust Your Budget

If you are living with a disability, it is vital to create and manage a budget that suits your lifestyle and income. However, your budget should not be set in stone. It needs to change over time to adapt to changes in income and expenses.

In this section, we will look at some tips to help you re-evaluate and adjust your budget as needed.

Regularly Revisit Your Budget

Revisiting your budget regularly enables you to make necessary adjustments. As your income and expenses change, you need to take time weekly, monthly, or quarterly to see if your budget still aligns with your financial goals. It also helps you identify any areas that need improvement to stay on track with your finances.

Some things you need to consider during this process include:

Identifying your current expenses

Review past spending

Analyze any changes in income

Look at the variable expenses and prioritize them

Update your budget allocation accordingly

Modify Budget To Adapt To Changes In Lifestyle And Income

It’s crucial to make changes to your budget when necessary. When you experience significant life changes like a job loss, illness, or disability, it’s essential to re-evaluate your budget and make modifications to accommodate these changes. You may need to prioritize some expenses over others and find ways to cut back on non-essential expenses.

Adapting your budget to your lifestyle changes keeps your finances stable and ensures that you are living within your means.

Overview Of Budgeting For Disability

When it comes to budgeting for disability, your budget should include the following:

A comprehensive list of expenses like accommodation, transportation, medical bills, and food, among others

Prioritizing expenses to ensure essentials are taken care of first

Identifying areas of potential savings to help you stay within your income limit

Incorporating provisions for emergency funds

Keeping track of your spending, income, and investments using a budget tracking tool

Importance Of Creating And Managing A Budget To Manage Expenses

Creating, managing, and adjusting your budget is a critical aspect of managing your expenses effectively. A budget enables you to:

Know your income and how much you need to spend

Prioritize expenses based on importance

Identify unnecessary expenses that you can cut down

Plan for the future by saving for emergencies or other goals

Additional Resources And Support Available For Help

If you need help budgeting for a disability, there are several resources available. Many organizations offer financial planning services and advice specifically tailored to people living with disabilities. You can also speak to a qualified financial advisor to assist you in developing a budget that works best for your lifestyle and income.

Re-evaluating and adjusting your budget regularly is essential in helping you remain financially stable when living with a disability. Prioritizing your spending, creating an emergency fund, and incorporating provisions for unexpected expenses are all important in ensuring that you stay within your income limit.

With these tips, you can efficiently budget for your disability and secure a stable financial future.

Frequently Asked Questions Of How To Budget For A Disability

What Is Disability Budgeting?

Disability budgeting is a financial plan to manage disability-related expenses.

Why Is Disability Budgeting Important?

Disability budgeting helps individuals with disabilities manage living costs, medical bills, and unexpected emergencies.

What Are Some Common Disability Expenses?

Common disability expenses include medical bills, home modifications, mobility aids, and transportation costs.

How Do I Create A Disability Budget?

Create a disability budget by tracking income and expenses, setting financial goals, and reducing unnecessary spending.

What Benefits Can I Apply For?

You can apply for benefits such as social security disability insurance (ssdi), supplemental security income (ssi), and medicaid.

How Can I Save Money On Healthcare Costs?

You can save on healthcare costs by using a prescription discount program, switching to generic medications, and using telemedicine services.

What If I Can’T Afford Necessary Equipment Or Modifications?

Consider applying for grants or low-interest loans from nonprofit organizations that provide assistance for people with disabilities.

How Do I Plan For Unexpected Expenses?

Plan for unexpected expenses by creating an emergency fund, seeking financial assistance, and developing a backup plan.

What If My Income Changes?

Adjust your disability budget to reflect changes in income and expenses. It’s important to be flexible and make necessary adjustments.

What Other Resources Are Available For Disability Budgeting?

There are many resources available such as financial counseling services, community-based programs, and support groups.

Conclusion

As you can see, budgeting for a disability can be challenging but not impossible. With the right mindset, discipline, and guidance, you can effectively manage your finances and achieve your financial goals. Remember to take advantage of various government and community resources, such as the supplemental security income (ssi) program and vocational rehabilitation, to help you become financially independent.

Always strive to increase your income streams and cut your expenses by creating a realistic and flexible budget. Lastly, don’t hesitate to seek help and support from financial experts, non-profit organizations, and your loved ones. With these tips in mind, you can stay financially secure and confident despite having a disability.

Money in economics is a store of value, aunit of account, a standard of deferred payment and a medium of exchange that we use to purchase goods and services without the need for cumbersome bartering. It is a fundamental concept in the field of economics and plays a crucial role in the functioning of modern societies.

Overall, money enables economies to function efficiently by providing a means of exchange, facilitating trade, and measuring value. In this article, we will delve deeper into the concept of money in economics and explore its various characteristics.

Credit: www.amazon.com

Characteristics Of Money

Medium of Exchange: Money serves as a widely accepted medium of exchange, providing a convenient and efficient way to facilitate transactions. It eliminates the need for barter, where goods or services are directly exchanged for other goods or services. With money, individuals can easily trade what they have for what they want, enabling specialization, division of labor, and the development of complex economies.

Unit of Account: Money serves as a unit of measurement and comparison for the value of goods, services, and assets. It provides a standardized means to express and quantify economic value. By assigning prices to different goods and services, money allows for efficient comparison and evaluation of their relative worth. This enables individuals and businesses to make informed decisions about production, consumption, investment, and resource allocation.

Store of Value: Money functions as a store of wealth over time. It allows individuals to save and hold onto their economic value for future use. By holding money, people can preserve their purchasing power, as money typically retains its value more reliably than perishable goods or commodities. Money’s ability to store value depends on factors such as stability, inflation rates, and the trust placed in the underlying economic and monetary system.

Portable: Money is designed to be easily carried and transferred, facilitating transactions across distances and among different parties. Physical money, such as coins or banknotes, is designed for portability and can be conveniently transported. Additionally, with the advent of digital payments, money can be quickly and securely transferred electronically, allowing for seamless transactions without the need for physical transportation.

Divisible: Money is divisible into smaller units, providing flexibility in transactions of varying values. This divisibility ensures that money can accommodate transactions at different price points, from small everyday purchases to larger investments or high-value transactions. For example, a dollar can be divided into cents, allowing for precise and granular pricing. Divisibility enhances the efficiency and versatility of money as a medium of exchange and facilitates economic activity across a wide range of transaction sizes.

Fungible: Money is fungible, which means that each unit of currency is mutually interchangeable with others of the same value. For example, if you have two $10 bills, you can exchange one for goods or services just as easily as the other. Fungibility ensures that money maintains its uniformity and acceptability in transactions, regardless of specific individual units.

Durability: Money should possess durability to withstand the wear and tear associated with repeated use. Physical forms of money, such as coins and banknotes, need to be able to circulate without deteriorating too quickly. Proper materials and quality standards are employed to ensure that money remains intact and usable over time, maintaining its value as a medium of exchange and store of wealth.

Acceptability: Money’s acceptability refers to its widespread recognition and willingness of individuals, businesses, and institutions to accept it as a form of payment. To function effectively, money must be accepted and trusted as a valid means of exchange within a given economic system. Legal frameworks, cultural norms, and established systems of commerce contribute to the acceptability of money.

Scarcity: Money derives value from its scarcity, meaning that it has a limited supply relative to the demand for it. If money were excessively abundant, its value would diminish, leading to inflation and loss of purchasing power. Maintaining a controlled and regulated supply of money helps to ensure its value over time, supporting stability and confidence in the economy.

Legal Tender: Money is recognized as legal tender when it is declared by the government as an authorized form of payment for settling debts and obligations within a specific jurisdiction. Legal tender status ensures that money is legally accepted and must be honored in payment transactions, providing a foundation of trust and confidence in its use as a medium of exchange.

These characteristics collectively make money a fundamental tool for economic exchange, enabling individuals, businesses, and governments to conduct transactions, allocate resources, measure value, save, and plan for the future. The development and acceptance of a stable and efficient monetary system are crucial for the functioning of modern economies and promoting economic growth and prosperity.

Functions Of Money

Money serves several important functions within an economy. Here are the key functions of money:

Medium of Exchange: Money acts as a widely accepted medium of exchange, facilitating the smooth exchange of goods and services. It eliminates the inefficiencies and limitations of barter by providing a universally accepted means of payment. With money, individuals can easily trade what they have for what they want, promoting specialization, trade, and economic growth.

Unit of Account: Money serves as a standard unit of measurement and comparison for the value of goods, services, and assets. By assigning prices to various items, money enables individuals and businesses to assess and compare the relative worth of different goods and services. It provides a common language for economic transactions, facilitating efficient resource allocation and economic decision-making.

Store of Value: Money allows individuals to store their wealth and purchasing power over time. It provides a reliable means of preserving value, unlike perishable goods or commodities. By saving money, individuals can accumulate wealth and defer consumption to the future. Money’s function as a store of value promotes economic stability, financial planning, and long-term investments.

Standard of Deferred Payment: Money serves as a standard for settling debts and making future payments. It allows individuals and businesses to enter into credit arrangements, loans, and contracts with confidence that the agreed-upon value can be honored and repaid in the future. Money’s function as a standard of deferred payment facilitates economic transactions, credit markets, and the smooth functioning of financial systems.

Measure of Value and Price Stability: Money provides a consistent measure of value that allows for comparing the prices of goods and services over time. It helps in evaluating changes in purchasing power and tracking inflation or deflation. Stable prices, supported by a stable monetary system, allow for more accurate economic calculations, investment decisions, and efficient allocation of resources.

Medium of Distribution: Money serves as a medium for distributing income, wages, and profits. It enables the fair and efficient exchange of labor and capital for monetary compensation. Money’s function as a medium of distribution ensures that individuals are rewarded for their contributions to the economy and can participate in economic activities.

Facilitates Specialization and Division of Labor: Money facilitates specialization and the division of labor within an economy. By providing a medium of exchange, it allows individuals and businesses to focus on their respective areas of expertise and engage in specialized production. This leads to increased efficiency, productivity, and overall economic growth.

Encourages Economic Growth and Investment: Money plays a crucial role in promoting economic growth and investment. It provides the necessary capital for businesses to expand, innovate, and invest in new technologies. Access to money enables entrepreneurs to start new ventures, create job opportunities, and drive economic development.

Facilitates Economic Calculation: Money enables accurate economic calculations by providing a common metric for valuing resources, production costs, and profitability. It allows businesses and individuals to evaluate the costs and benefits of different choices, make informed decisions, and allocate resources efficiently.

Enables Economic Stability and Policy Implementation: Money, when effectively managed by central banks and monetary authorities, contributes to maintaining price stability, controlling inflation, and promoting overall economic stability. Monetary policy tools, such as interest rates and money supply management, are used to regulate the economy, address economic imbalances, and mitigate the impact of economic fluctuations.

These functions of money collectively form the basis of modern economies, facilitating economic transactions, resource allocation, investment, and growth. Understanding the functions of money is crucial for individuals, businesses, policymakers, and economists to navigate financial systems, formulate effective policies, and foster sustainable economic development.

Types Of Money

There are several types of money that have been used throughout history and are still in use today. Here are the main types of money:

Commodity Money: Commodity money is a type of money that has intrinsic value based on the material it is made of. Historically, commodities such as gold, silver, and other precious metals have been used as commodity money. The value of commodity money is derived from the value of the underlying commodity itself.

Fiat Money: Fiat money is a type of money that is not backed by a physical commodity but is declared by the government as legal tender. Its value is based on the trust and confidence placed in the issuing authority. Most modern currencies, such as the US dollar, euro, or yen, are examples of fiat money. Fiat money has value because the government mandates its use and accepts it as a means of payment for debts and taxes.

Representative Money: Representative money is a form of money that represents a claim on a commodity, typically a precious metal. In the past, paper currency or banknotes were often redeemable for a specific amount of gold or silver. While the representative money itself may not have intrinsic value, it can be exchanged for the underlying commodity upon demand.

Digital Money: Digital money refers to money that exists in electronic or digital form. It includes electronic bank account balances, digital currencies, and mobile payment systems. Digital money allows for convenient and fast transactions, often facilitated through online banking platforms, mobile apps, or cryptocurrencies such as Bitcoin.

Cryptocurrency: Cryptocurrency is a type of digital currency that uses cryptography for security and operates on decentralized networks called blockchains. Examples include Bitcoin, Ethereum, and Litecoin. Cryptocurrencies are not issued or regulated by any central authority, and their value is determined by supply and demand dynamics in the market.

Local and Community Currencies: Local or community currencies are forms of money that are used within a specific locality or community. They are often created to encourage local economic activity, foster community development, and promote sustainable practices. Local currencies are typically not widely accepted outside their specific region and may coexist alongside national currencies.

Bank Money: Bank money refers to money that exists in the form of electronic records or account balances held by commercial banks. When individuals deposit money in banks, they receive account balances that can be used for transactions. Bank money is created through the process of fractional reserve banking, where banks keep only a fraction of their deposits as reserves and lend out the rest.

Legal Tender: Legal tender refers to the money that is recognized by law as a valid means of payment for settling debts and obligations within a particular jurisdiction. It is the form of money that must be accepted by individuals and businesses to fulfill financial obligations. Legal tender status is typically assigned to the official currency issued by the government.

These are some of the main types of money that have been used or are currently in use. The type of money employed in an economy can vary based on historical, cultural, and technological factors. The evolution of money continues to be influenced by advancements in digital technology and the emergence of new forms of currency.

Money Creation And Monetary Policy

Money creation and monetary policy play a significant role in economics. Banks create money by using a central banking system and setting aside reserves. The amount of money in circulation affects the economy’s supply and demand, causing changes in interest rates, inflation, and unemployment levels.

The central banks manage monetary policy by increasing or decreasing the money supply. When the economy slows, they may reduce interest rates to stimulate spending and investment. Alternatively, they may raise interest rates to curb inflation when the economy is growing too fast.

The central banks’s actions have a significant impact on economic growth. By carefully managing the money supply, they ensure that the economy stays healthy and stable.

Frequently Asked Questions On What Is Money In Economics?

Q1. What Is Money’S Definition In Economics?

Money is a medium of exchange in an economy used to buy goods and services.

Q2. Why Is Money Important In Economics?

Money facilitates economic transactions, helps savings, and assists in measuring economic activities.

Q3. How Does Money Circulate In An Economy?

Money circulates through economic agents such as households, businesses, and financial institutions.

Q4. What Are The Different Types Of Money In Economics?

There are various types of money such as fiat money, commodity money, and representative money.

Q5. How Does Inflation Affect The Value Of Money?

Inflation decreases the value of money; therefore, the purchasing power of money decreases.

Q6. What Is The Role Of The Central Bank In Managing Money?

Central banks are responsible for monetary policy and issuing and regulating money in an economy.

Q7. How Does Money Affect The Standard Of Living In An Economy?

Money affects the standard of living by influencing economic growth, income, and consumption patterns.

Conclusion

Ultimately, money is a complex and fundamental aspect of economics that plays a crucial role in our daily lives. It facilitates trade, provides a means of exchange, and serves as a unit of account. The concept of money has evolved over time, from simple exchange systems to modern, digital currencies.

Still, the underlying principles remain the same: money has value because we believe it does. Understanding the functions and characteristics of money is essential for policymakers and individuals alike. While there are ongoing debates and discussions about the best types of money and how they should be managed, it is clear that money will continue to play a central role in our economies and societies.

By grasping the nuances of money and its role in our lives, we can make informed decisions, both at the individual and policy level, to contribute to a more prosperous and equitable future.

Money is an integral part of our daily lives. From buying groceries to paying bills, money is essential. But have you ever wondered what the actual functions of money are? In this article, we’ll explore the functions of money and why it’s important to understand them.

Functions of Money

The functions of money are essential for the smooth functioning of an economy. Without money, it would be much more difficult for people to trade with each other, save for the future, and make economic decisions. money mainly serves 4 functions-namely

A Medium of exchange

A Unit of Account

A Store of Value

A Standard of deferred payment

Medium of Exchange

The first and most obvious function of money is that it acts as a medium of exchange. Without money, individuals and businesses would need to rely on bartering – exchanging goods or services for other goods or services. This can be time-consuming and difficult, as it relies on two parties having something the other wants. Money, on the other hand, is universally accepted and can be used to buy any goods or services.

Money serves several functions, and one of its primary roles is functioning as a medium of exchange. Here are the key functions of money in its role as a medium of exchange:

Facilitates Transactions: Money serves as a universally accepted medium for exchanging goods and services. It eliminates the need for a barter system, where direct exchange of goods or services would require a double coincidence of wants. With money, individuals can easily trade what they have for what they desire, enabling a more efficient and flexible exchange of goods and services.

Enhances Efficiency: Money improves the efficiency of transactions by providing a standardized and widely accepted medium of exchange. It simplifies the process of buying and selling, as individuals can accept money in exchange for their goods or services, knowing that they can use it to acquire other goods or services in the future. This efficiency promotes specialization, division of labor, and the development of complex market economies.

Overcomes the Problem of Indivisibility: Money helps overcome the challenge of indivisibility that exists in barter systems. With barter, it may be difficult to exchange goods of different values or quantities. Money solves this problem by providing a divisible medium that can be used for transactions of varying sizes. It allows for precise pricing and enables transactions involving fractions or multiples of the currency unit.

Facilitates Trade Across Boundaries: Money acts as a universal medium of exchange that transcends geographic boundaries and simplifies international trade. It eliminates the need for direct barter between countries with different currencies and enables the exchange of goods and services across nations through currency conversion. Money enables global trade by providing a common medium for conducting international transactions.

Enables Future Transactions: Money’s function as a medium of exchange extends to future transactions. It allows for deferred payments and the establishment of credit arrangements. By accepting money as payment for goods or services, individuals and businesses can accumulate purchasing power that can be used for future transactions or settling outstanding debts. This promotes economic activity and supports the functioning of credit markets.

Provides Pricing Mechanism: Money serves as a pricing mechanism by assigning a monetary value to goods and services. Prices expressed in terms of money provide a standardized metric that helps individuals evaluate the relative worth of different goods and make informed decisions about their purchase or sale. Money enables efficient price discovery and promotes market transparency.

Supports Market Liquidity: Money enhances market liquidity by providing a readily acceptable medium of exchange. It ensures that there is a sufficient supply of fungible money that can be easily exchanged for goods or services, promoting the smooth functioning of markets. Market liquidity facilitated by money allows for swift and efficient transactions, reducing transaction costs and enhancing market efficiency.

Reduces Transaction Costs: Money reduces transaction costs associated with barter systems. In a barter economy, individuals would need to spend time and effort finding a suitable trading partner with mutually desired goods. Money simplifies this process by providing a universally accepted medium of exchange, eliminating the need for direct barter negotiations and reducing transaction costs.

Enables Specialization and Efficiency Gains: Money’s role as a medium of exchange encourages specialization and the division of labor. It allows individuals and businesses to focus on their core competencies, producing goods or services in which they have a comparative advantage. Specialization, made possible by money, leads to increased efficiency, productivity, and economic growth.

Promotes Economic Development: Money’s function as a medium of exchange plays a crucial role in promoting economic development. It encourages trade, investment, and the efficient allocation of resources within an economy. The availability of a stable and widely accepted medium of exchange is essential for fostering economic growth, attracting investment, and improving living standards.

Unit of Account

Money serves as a unit of account, meaning it is a way of measuring and comparing the value of goods and services. For instance, when you go to a grocery store, you look at the price tags to determine the value of each product. The store owner uses money as a unit of account to determine the value of the goods they sell.

Here are the functions of money as a store of value:

Wealth Preservation: Money acts as a store of value by allowing individuals to hold and preserve their wealth over time. Instead of immediately spending all their earnings, people can save money for future use, ensuring the preservation of their financial resources.

Future Purchasing Power: Money retains its value over time, allowing individuals to save for future needs and aspirations. By storing money, people can accumulate purchasing power and have the means to acquire goods, services, or assets at a later date.

Inflation Hedge: Money can serve as a hedge against inflation. Inflation refers to the general increase in prices over time, resulting in the erosion of purchasing power. By holding money, individuals can protect their wealth from the effects of inflation and maintain their ability to buy goods and services in the future.

Stability and Liquidity: Compared to other assets, money offers a high degree of stability and liquidity. It is readily accessible and can be easily converted into goods or other forms of assets when needed. This liquidity ensures that money can serve as a reliable store of value, providing individuals with financial flexibility.

Deferred Consumption: Money as a store of value enables individuals to defer consumption and postpone spending. By saving money, people can delay immediate gratification and allocate resources towards achieving long-term goals, such as purchasing a house, funding education, or planning for retirement.

Intermediary Function: Money as a store of value also facilitates various financial activities, such as investment and lending. It allows individuals and institutions to accumulate funds and deploy them for productive purposes, leading to economic growth and development.

Stability and Certainty: Money, particularly in the form of stable currencies, provides a sense of stability and certainty in financial transactions. By storing value in money, individuals can mitigate risks associated with fluctuations in the value of other assets, such as stocks, real estate, or commodities.

Store of Value

Money acts as a store of value, which means it can be stored away and used at a later date. For example, you can save money in a bank account or invest it in stocks or bonds. This way, your money retains its value and can be used in the future.

Here are the functions of money as a unit of account:

Standardized Measurement: Money serves as a common unit of account, providing a standardized measurement for valuing goods, services, and assets. It establishes a uniform system that enables individuals and businesses to compare and quantify the value of different items.

Pricing and Valuation: Money allows for the determination of prices and the valuation of goods and services in a consistent and easily understandable manner. By using a common unit of account, individuals can assess the relative worth of various products, making informed decisions about purchases, sales, and investments.

Comparability: Money facilitates the comparison of prices and costs across different goods and markets. It enables individuals to evaluate the relative value of similar products or services and make choices based on their preferences and budget constraints. The use of a unit of account enhances market transparency and efficiency.

Accounting and Financial Reporting: Money serves as the basis for financial accounting and reporting. It provides a standard unit for measuring revenues, expenses, assets, and liabilities in financial statements. This uniformity ensures consistency in financial records and enables meaningful comparisons over time.

Contracts and Agreements: Money as a unit of account is essential for drafting and enforcing contracts and agreements. It establishes a common reference point for specifying prices, payment terms, and financial obligations. Parties involved in transactions can rely on money as a reliable unit of measurement when formalizing their agreements.

Economic Analysis: Money facilitates economic analysis by allowing economists and policymakers to measure and track various economic indicators, such as GDP (Gross Domestic Product), inflation rates, and consumer spending. These indicators are expressed in monetary terms and provide insights into the state of the economy.

Decision Making: Money as a unit of account supports decision making at both individual and organizational levels. It enables individuals to assess the costs and benefits of different choices and make rational economic decisions. Similarly, businesses can use monetary units to evaluate profitability, set prices, and allocate resources effectively.

Standard of Deferred Payment

Money also serves as a standard of deferred payment, which means it can be used to pay off debts at a later time. For instance, if you take out a loan, you can pay it back over time using money as a standard of payment. Similarly, credit cards allow consumers to make purchases and pay them off later using money as a standard of payment.

Here are the functions of money as a standard of deferred payment:

Debt Settlement: Money serves as a standard of deferred payment by allowing individuals and businesses to settle debts and financial obligations over time. It provides a universally accepted medium for repayment, ensuring that creditors can expect to receive value for their goods or services in the future.

Borrowing and Lending: Money as a standard of deferred payment enables borrowing and lending activities. Individuals and businesses can borrow money and promise to repay it in the future, with interest, using money as the agreed-upon medium of exchange. Lenders accept money as a reliable means of deferring payment and expect to receive it back with added compensation.

Credit Transactions: Money facilitates credit transactions, wherein individuals or businesses purchase goods or services on credit, agreeing to make future payments. By accepting money as a standard of deferred payment, sellers are assured of receiving the agreed-upon value at a later date.