To refinance your investment property, start by assessing your property’s current value and existing mortgage terms. Then, compare rates and terms from various lenders to find the best refinancing option for your investment property.

Refinancing can help lower your monthly payments, reduce your interest rate, and consolidate debt, ultimately improving your overall financial position. Refinancing your investment property can be a wise financial move, helping you take advantage of lower interest rates or access your property’s equity.

By refinancing, you may be able to secure a more favorable loan term, reduce your monthly payments, or even access cash for other investment opportunities. Understanding the steps involved in refinancing your investment property can empower you to make informed decisions about your financial future.

Assessing Your Property Value

When looking to refinance your investment property, one crucial step is assessing your property value. Proper evaluation helps you understand how much equity you have and determines the refinancing options available to you. Here are the essential steps to assess your property value:

Researching Comparable Properties

Start by researching similar properties in your area to determine the current market value. An effective way is to use online real estate platforms that provide data on recent property sales. Look for properties with similar size, location, and condition to get a clear picture of your property’s value.

Obtaining A Professional Appraisal

A professional appraisal is crucial for an accurate valuation of your investment property. An appraiser will assess various factors, including the property’s condition, location, and recent sales data to provide a comprehensive evaluation. This appraisal serves as an unbiased and expert opinion of your property’s worth, which is essential for refinancing.

Understanding Refinancing Options

Understanding your refinancing options is crucial when it comes to maximizing your investment property’s potential. By exploring different loan programs and considering the various interest rates and terms available, you can make informed decisions that suit your financial goals and objectives.

Exploring Different Loan Programs

When considering refinancing your investment property, it’s essential to explore the different loan programs available. Conventional loans, for example, are popular for investment properties, offering both fixed and adjustable rate options. Another alternative is government-backed loans such as FHA or VA loans, which have specific eligibility requirements and terms. Additionally, portfolio loans provided by portfolio lenders can be customized to fit your unique financial situation, providing greater flexibility.

Considering Interest Rates And Terms

Interest rates and terms play a significant role in the decision-making process for refinancing your investment property. It’s crucial to compare and analyze the current market rates and carefully consider whether a fixed-rate mortgage or an adjustable-rate mortgage aligns with your investment strategy. Paying attention to the loan term is also important, as different terms can significantly impact your monthly cash flow and overall interest costs.

Preparing Your Finances

Refinancing an investment property requires thorough preparation of your finances. By organizing income and expense documentation and checking your credit score and history, you can position yourself for a successful refinance. Properly managing your finances is essential to demonstrate your financial stability and increase the likelihood of securing favorable terms for your refinance.

Organizing Income And Expense Documentation

Start by gathering all necessary documents related to your investment property, including income statements, rental agreements, and tax returns. Create a clear and comprehensive overview of your property’s financial performance to ensure you can present a complete picture to potential lenders. This detailed documentation is essential for lenders to assess the income potential of your investment property and evaluate your eligibility for refinancing.

Checking Credit Score And History

Obtain a recent copy of your credit report and carefully review it for any inaccuracies or discrepancies. Ensure timely payments on existing debts and resolve any outstanding issues to improve your credit score. Your credit history plays a significant role in determining the terms and interest rates for your refinance. By maintaining a strong credit profile, you position yourself as a reliable borrower and increase your chances of securing a favorable refinancing deal.

Navigating The Refinancing Process

When it comes to refinancing your investment property, navigating the process can seem daunting. However, with the right approach and understanding, you can successfully navigate the refinancing process and achieve your financial goals. Here’s a breakdown of the crucial steps involved in refinancing your investment property.

Choosing A Lender

Choosing the right lender is a pivotal step in the refinancing journey. Look for lenders specializing in investment property refinancing. Compare and evaluate their interest rates, terms, and fees to ensure you’re getting the best deal.

Completing The Application Process

Once you’ve chosen a lender, it’s time to complete the application process. Be sure to have all necessary documents such as tax returns, bank statements, and property information ready. Provide accurate and detailed information to expedite the process and increase your chances of approval.

Frequently Asked Questions Of How To Refinance Your Investment Property

Can I Refinance An Investment Property?

Yes, you can refinance an investment property to potentially lower interest rates and monthly payments. It can also provide access to equity for other investments. Refinancing typically requires a good credit score and a solid income.

What Credit Score Is Needed To Refinance An Investment Property?

Typically, a credit score of 620 or higher is needed to refinance an investment property. However, some lenders may require a higher score. It’s essential to shop around and compare offers from different lenders to find the best option for your situation.

How Do I Pull Equity Out Of My Investment Property?

To pull equity out of your investment property, you can consider refinancing your mortgage or taking out a home equity loan or line of credit. By doing this, you can borrow against the value of your property and access the funds for other purposes.

Conclusion

Refinancing your investment property can be a wise financial move. By following the steps outlined you can potentially lower your interest rate, access cash for other investments, and improve your overall financial situation. Remember to carefully consider your options and consult with a financial advisor before making any decisions.

Voodoo Economics: Understanding the Controversial Theory

Voodoo Economics, also known as Supply-Side Economics, is a controversial economic theory that gained prominence during the 1980s. Coined by critics, the term “Voodoo Economics” suggests that the theory is fundamentally flawed and relies on unrealistic assumptions. In this article, we will delve into the principles behind Voodoo Economics and examine its impact on the economy.

Credit: www.slideshare.net

The Basics of Voodoo Economics

At its core, Voodoo Economics advocates for policies that focus on tax cuts with the belief that these reductions will stimulate economic growth. The theory argues that by reducing tax levels, individuals and businesses will have more disposable income, which in turn will encourage spending and investment. This, in theory, should lead to economic expansion, job creation, and increased government revenue.

Proponents of Voodoo Economics argue that by reducing taxes, the incentives for businesses and individuals to work, save, and invest increase. They claim that this leads to a virtuous cycle where higher economic activity offsets the initial loss of tax revenue, ultimately resulting in higher tax revenue in the long run.

The Laffer Curve

One of the central pillars of Voodoo Economics is the Laffer Curve, a graphical representation of the relationship between tax rates and tax revenue. The curve suggests that at some point, a tax rate becomes so high that it discourages economic activity and actually reduces tax revenue. Conversely, cutting tax rates below this point is believed to stimulate economic growth and increase revenue.

However, critics argue that the Laffer Curve oversimplifies the complex relationship between tax rates and revenue. They contend that it is not a reliable indicator of the exact point at which tax cuts will lead to increased revenue. Furthermore, opponents of Voodoo Economics argue that tax cuts mainly benefit the wealthy, exacerbating income inequality.

Controversies and Criticisms

Voodoo Economics has attracted both proponents and critics since its inception. Critics argue that the theory lacks a strong empirical basis and that historical evidence does not support the hypothesis that tax cuts lead to significant economic growth. They claim that while tax cuts may contribute to short-term stimulus, the long-term effects on the economy are limited.

Furthermore, opponents argue that tax cuts can lead to a decrease in government revenue, potentially resulting in budget deficits and increased national debt. They assert that this can lead to adverse consequences for the economy in the long run.

The Legacy of Voodoo Economics

Despite the criticisms, Voodoo Economics has had a lasting impact on economic policy. It played a prominent role in shaping the economic policies of the Reagan administration in the United States. Reagan implemented significant tax cuts under the belief that they would stimulate economic growth and foster prosperity.

Since then, various countries have adopted similar supply-side economic policies, with some experiencing varying degrees of success. However, the ongoing debates continue as to whether the outcomes are a result of the policies themselves or other external factors.

Credit: www.c-span.org

In Conclusion

Voodoo Economics, or Supply-Side Economics, remains a highly debated theory in the field of economics. While proponents argue that tax cuts can unleash economic growth, critics often challenge the assumptions and efficacy of such policies. Understanding the principles and controversies surrounding Voodoo Economics is crucial in comprehending the ongoing debates about economic policy.

To launch a wealth management firm, first, conduct thorough market research to identify your target audience and develop a unique value proposition. Next, acquire the necessary licensing and qualifications, create a business plan, and establish strategic partnerships within the financial industry.

This comprehensive approach will ensure a successful launch and sustainable growth for your firm. Launching a wealth management firm requires careful planning and strategic decision-making. By conducting in-depth market research and identifying your target audience, you can position your firm effectively within the competitive financial landscape.

Acquiring the necessary licensing and qualifications, crafting a robust business plan, and establishing key partnerships will set the foundation for a successful and sustainable wealth management firm. This approach will pave the way for long-term success and prominence in the industry.

Defining Your Value Proposition

When launching a wealth management firm, one of the first crucial steps is to define your value proposition. Your value proposition is the unique offering that differentiates your firm from competitors and clearly communicates the benefits you provide to clients.

Identifying Your Target Market

Identifying your target market is the foundation of building a successful wealth management firm. By understanding who your ideal clients are, you can tailor your services and value proposition to meet their specific needs and preferences.

Here are key steps to identify your target market:

Conduct thorough market research to analyze demographics, psychographics, and financial goals of potential clients.

Consider specialization and niche markets that align with your expertise and interests.

Segment your target market based on factors such as age, income, occupation, and investment preferences.

Identify the pain points or challenges that your target market faces in managing their wealth.

Determining Your Unique Offering

Once you have identified your target market, it’s important to determine your unique offering that sets you apart from other wealth management firms. Your unique offering should highlight the value you bring to clients and address their specific needs.

Here are some strategies to determine your unique offering:

Evaluate your expertise and experience to identify what sets you apart from competitors.

Consider specialized services or investment strategies that cater to your target market’s unique needs.

Focus on providing exceptional customer service and personalized attention to clients.

Implement innovative technology solutions to enhance the client experience.

Taking the time to define your value proposition, identify your target market, and determine your unique offering will give your wealth management firm a competitive edge and attract the right clients. With a clear value proposition, you can effectively communicate the benefits clients will receive by choosing your firm, ultimately driving growth and success.

Creating A Robust Business Plan

Create a strong business plan to successfully launch your wealth management firm. Craft a detailed strategy that outlines your target market, services, and financial projections to attract investors and achieve long-term growth.

Creating a robust business plan is a critical first step in launching a wealth management firm. A well-crafted plan will serve as your roadmap, outlining the goals and objectives you aim to achieve, conducting necessary market research, and determining a pricing model that aligns with your value proposition. This article will break down each component, providing you with practical steps to develop a comprehensive business plan that will set your wealth management firm up for success.

Setting Clear Goals And Objectives

Setting clear goals and objectives is fundamental to the success of your wealth management firm. Identify what you want to accomplish and articulate it concisely. Consider factors such as the target market, revenue targets, the range of services you will offer, and the level of expertise you bring to the table. Keep your goals specific, measurable, achievable, relevant, and time-bound (SMART). By clearly defining your objectives, you establish a roadmap for your firm’s growth and ensure all your efforts are aligned towards a common purpose.

Conducting Market Research

Market research plays a pivotal role in understanding the competitive landscape and identifying opportunities for your wealth management firm. Begin by analyzing the various segments within the market, including the size, demographics, and needs of your target clients. Identify your unique selling proposition (USP) and conduct a competitor analysis to understand how your firm can differentiate itself. By gathering relevant data and insights, you can make informed decisions about how to position your firm in the market and create strategies that resonate with your target audience.

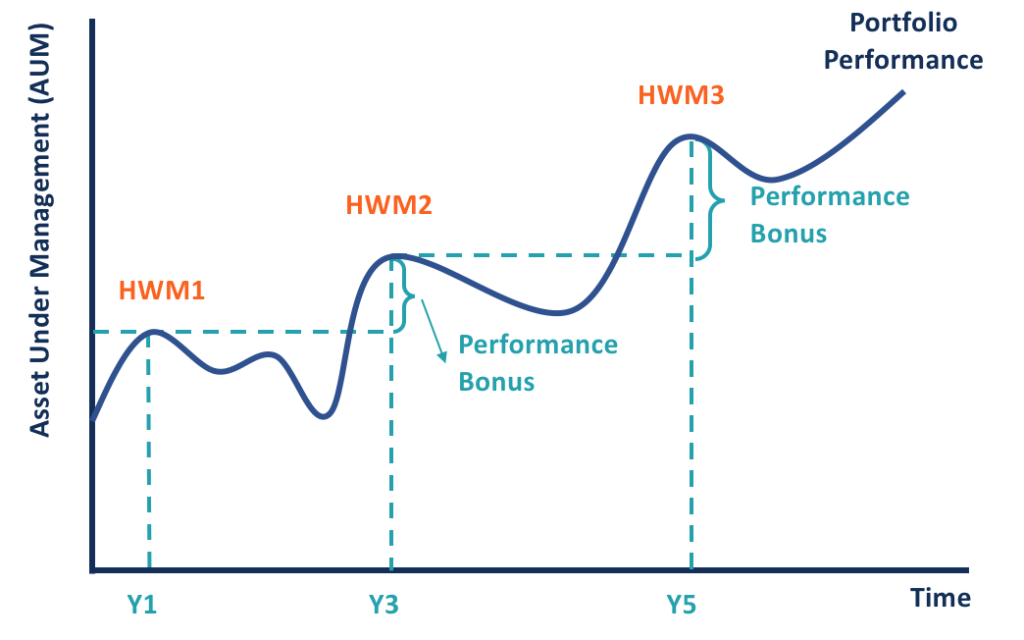

Determining Your Pricing Model

Determining your pricing model is crucial in creating a sustainable and profitable wealth management firm. Consider the value you are delivering to clients and the costs associated with providing your services. Will you charge a percentage of the assets under management (AUM), a flat fee, or a combination of both? Assess both the market expectations and your firm’s financial goals to establish a pricing structure that is competitive yet profitable. Additionally, leverage your market research to understand the pricing strategies of your competitors and find the balance between offering value to clients while maintaining a viable business model.

In conclusion, creating a robust business plan for your wealth management firm is essential. By setting clear goals and objectives, conducting thorough market research, and determining an appropriate pricing model, you can lay a solid foundation for your firm’s success. Remember to regularly revisit and adjust your business plan as your firm evolves, aligning your efforts towards achieving your long-term goals and delivering exceptional wealth management services to your clients.

Obtaining Necessary Licenses And Registrations

Launching a wealth management firm involves obtaining the necessary licenses and registrations to comply with regulatory requirements. Understanding these requirements and applying for the appropriate licenses and registrations are vital steps in establishing a credible and compliant wealth management firm. In this section, we will explore these two aspects in detail.

Understanding Regulatory Requirements

Before jumping into the process of obtaining licenses and registrations, it is crucial to grasp the regulatory requirements that govern the wealth management industry. These requirements vary based on the jurisdiction in which you intend to operate, and it is essential to educate yourself about the specific regulations that apply to your firm.

Regulatory bodies such as the Securities and Exchange Commission (SEC) or the Financial Industry Regulatory Authority (FINRA) provide guidelines that dictate the licensing and registration processes for wealth management firms. Familiarize yourself with these guidelines to ensure compliance and avoid any potential legal issues down the line.

Applying For The Appropriate Licenses And Registrations

Once you have a solid understanding of the regulatory landscape, it’s time to apply for the necessary licenses and registrations. This step involves a meticulous and often time-consuming process to demonstrate your firm’s qualifications and meet the regulatory standards. Below are some key steps to guide you:

Identify the specific licenses and registrations required for your wealth management firm. Common examples include investment advisor registration or broker-dealer licenses.

Gather all the necessary documentation, including information about your firm’s structure, key personnel, and financial statements.

Prepare a comprehensive business plan that outlines your firm’s goals, strategies, and compliance procedures.

Complete the required application forms provided by the relevant regulatory bodies.

Submit your application along with the supporting documentation and applicable fees.

Once you have submitted your application, expect a period of review from the regulatory authorities. During this time, they will evaluate your firm’s qualifications and compliance with the regulations. It is essential to be patient and thorough throughout this process, ensuring that you address any inquiries or requests for additional information promptly.

Obtaining the necessary licenses and registrations is a critical milestone in launching your wealth management firm. By adhering to the regulatory requirements and following the application process diligently, you can establish a credible and compliant foundation for your business.

Building A Talented Team

When it comes to launching a successful wealth management firm, one of the key factors to consider is building a talented team. Your team will be the foundation of your firm, responsible for providing high-quality services to your clients and driving growth. Hiring experienced professionals and creating a supportive and collaborative work environment are crucial steps in this process.

Hiring Experienced Professionals

Hiring experienced professionals is essential to ensure that your wealth management firm has the expertise needed to navigate the complexities of the financial industry. Look for candidates who have a strong track record in wealth management and are well-versed in investment strategies, financial planning, and risk management.

To attract top talent, clearly define the roles and responsibilities of each position and clearly communicate your firm’s values, mission, and vision. Utilize online job boards, professional networks, and industry events to reach out to potential candidates. When conducting interviews, ask targeted questions to assess their knowledge and experience, and don’t forget to check their references.

Once you have identified the right candidates, make sure your compensation package is competitive and includes incentives for performance. This will attract and retain top talent, ensuring the growth and success of your wealth management firm.

Creating A Supportive And Collaborative Work Environment

Creating a supportive and collaborative work environment is crucial to foster teamwork, employee engagement, and productivity. When your team members feel valued and supported, they are more likely to contribute their best efforts and work together towards achieving common goals.

Encourage open communication and idea-sharing by establishing regular team meetings and brainstorming sessions. Create opportunities for professional development, such as training programs, certifications, and industry conferences. This will not only enhance individual skills but also strengthen your firm’s expertise as a whole.

To promote collaboration, provide your team members with the necessary tools and technology to collaborate effectively. Foster a culture of trust and respect, where feedback is given constructively and recognized achievements are celebrated. By creating a positive work environment, you will attract top talent and retain them in the long run, contributing to the success of your wealth management firm.

Developing A Strong Marketing Strategy

Launching a wealth management firm is an exciting venture that requires careful planning and strategizing. One of the key elements of success is developing a strong marketing strategy. In today’s digital age, having a robust online presence and utilizing traditional marketing channels are vital. Additionally, forming strategic partnerships can help you connect with your target audience and establish credibility in the market. In this section, we will explore these three crucial aspects of developing an effective marketing strategy for your wealth management firm.

Building Your Online Presence

A solid online presence is essential in today’s digital landscape. It enables you to reach a wider audience and establish your brand as a trusted source of financial expertise. To build your online presence, consider the following:

Create a website that showcases your firm’s services, team, and expertise. Ensure that it is visually appealing, user-friendly, and optimized for search engines.

Regularly publish high-quality blog posts and articles that provide valuable insights and guidance on wealth management topics.

Engage with your audience on social media platforms, such as Twitter, LinkedIn, and Facebook. Share relevant content, respond to comments, and participate in industry-related discussions.

Implement Search Engine Optimization (SEO) techniques to improve your website’s visibility in search engine rankings. This includes using relevant keywords, optimizing meta tags, and building high-quality backlinks.

Utilizing Traditional Marketing Channels

While the digital space offers immense opportunities, traditional marketing channels should not be overlooked. Consider the following traditional marketing strategies:

Host educational seminars or workshops to educate your target audience about wealth management. Take advantage of these events to establish yourself as an industry expert.

Participate in relevant industry conferences and tradeshows to network with potential clients and industry professionals.

Collaborate with local newspapers and magazines to contribute articles or be featured as a guest columnist, enhancing your credibility and visibility.

Distribute printed materials, such as brochures and business cards, at networking events or community gatherings.

Consider direct mail campaigns to target a specific demographic within your market.

Developing Strategic Partnerships

Forming strategic partnerships can greatly benefit your wealth management firm by expanding your reach and enhancing your reputation. Consider the following approaches:

Collaborate with complementary businesses, such as tax consultants or estate planners, to offer bundled services to clients.

Establish relationships with influential individuals or organizations in the financial industry, such as local business associations or professional networking groups.

Sponsor relevant events or charitable causes to increase your firm’s visibility and demonstrate your commitment to the community.

Engage in strategic cross-promotions with businesses that share a similar target audience, providing mutual benefits.

Frequently Asked Questions Of How To Launch A Wealth Management Firm?

Can I Start My Own Wealth Management Firm?

Yes, you can start your own wealth management firm. It requires proper planning, knowledge of financial markets, registration, and compliance with regulatory requirements. Advise clients on investments, financial planning, retirement, and estate planning to manage and grow their wealth.

How Do I Set Up A Wealth Management Firm?

To set up a wealth management firm, create a business plan, obtain necessary licenses, hire experienced professionals, build a client base, and establish strategic partnerships. Additionally, invest in reliable technology and maintain compliance with industry regulations.

How Much Money Do You Need To Start Wealth Management?

To start wealth management, the amount of money needed varies depending on your financial goals and investment preferences. It is recommended to have a decent sum, typically around $250,000 or more, to ensure effective management and diversification of your assets.

Conclusion

After implementing the strategies outlined in this blog post, you are well on your way to successfully launching a wealth management firm. By thoroughly researching your target market, establishing strong client relationships, providing comprehensive services, and leveraging technology, you can differentiate yourself in this competitive industry.

Remember to continuously adapt to industry changes and consistently analyze your performance to ensure long-term success. Launching a wealth management firm may seem daunting, but with the right approach and determination, you can achieve your goals and build a thriving business.

Mergers and acquisitions can significantly impact a company. They can lead to changes in leadership, organizational structure, and even company culture.

Mergers and acquisitions can have a profound effect on a company’s operations, financial stability, and market positioning. These transactions can result in increased market share and revenue, as well as expanded customer base and access to new technologies and resources.

However, they can also bring about challenges such as integration issues, cultural clashes, and workforce restructuring. Furthermore, they may lead to changes in brand identity, customer relationships, and competitive landscape. Understanding the potential impacts of mergers and acquisitions is crucial for both the companies involved and their stakeholders as they navigate through these transformative processes.

Effect On Organizational Culture

When it comes to mergers and acquisitions, one of the crucial aspects that often gets overlooked is the impact on organizational culture. The amalgamation of two distinct cultures can lead to various workplace integration and cultural alignment challenges, significantly affecting the overall dynamics of the company.

Workplace Integration

Mergers and acquisitions result in the consolidation of employees from different backgrounds, work practices, and beliefs. This can lead to a clash of work styles and communication barriers, making it essential for the company to proactively facilitate integration through team-building activities, cross-departmental collaboration, and open communication channels.

Cultural Alignment Challenges

Cultural alignment challenges often arise when employees from the merging entities have differing values, beliefs, and attitudes. This can disrupt the harmony within the organization, impacting productivity and employee morale. It’s crucial for the leadership to foster a culture of inclusivity and diversity, promoting understanding and empathy among employees. Clear communication about the company’s vision and values is imperative to ensure a smooth transition and alignment of cultures.

Impact On Financial Performance

Mergers and acquisitions can significantly affect a company’s financial performance, leading to shifts in revenue, expenses, and overall profitability. This impact can result from cost synergies, increased market share, or a more diversified product offering, ultimately influencing the company’s bottom line.

Impact on Financial Performance

Merger and acquisition activities can significantly impact a company’s financial performance. These changes can directly affect the earnings and revenue, as well as offer cost synergy opportunities. Let’s explore how these factors come into play in the context of mergers and acquisitions.

Earnings And Revenue Changes

Earnings and revenue changes are common outcomes of mergers and acquisitions. The consolidation of businesses can lead to an increase or decrease in the combined company’s earnings and revenue. In some cases, the new entity may experience a boost in earnings and revenue due to expanded market reach and increased economies of scale. Conversely, challenges in integrating operations can lead to temporary decreases in earnings and revenue.

Cost Synergy Opportunities

Mergers and acquisitions often bring about cost synergy opportunities. These opportunities arise when the combined entity is able to eliminate redundant functions, consolidate operations, and negotiate better deals with suppliers. This can lead to significant cost savings for the merged company, potentially improving its overall financial performance. However, realizing these synergies often requires strategic planning and effective execution to ensure they are fully leveraged.

In conclusion, the impact of mergers and acquisitions on a company’s financial performance can be profound. Changes in earnings and revenue, as well as the pursuit of cost synergy opportunities, can significantly influence the financial health and success of the newly combined entity.

Influence On Employee Morale

When a company goes through a merger or acquisition, one of the most critical aspects to consider is the influence it has on employee morale. The transition period can be turbulent for employees, leading to concerns about job security, integration, and communication within the new structure.

Job Insecurity Concerns

Mergers and acquisitions often spark a sense of job insecurity among employees. The fear of potential layoffs or restructuring causes anxiety and unease, impacting their motivation and productivity.

Integration And Communication

The integration of two organizations can bring about challenges in communication and workflow alignment. Employees may face difficulties in adapting to new systems, processes, and hierarchies, leading to decreased morale and job satisfaction.

Effect On Market Position

Competitive Landscape

Mergers and acquisitions can significantly impact a company’s competitive landscape. When two companies merge or one acquires another, the resulting entity may become a stronger competitor in the market. This can lead to a shift in the competitive dynamics, altering the market share and positioning of the involved companies. The combined resources, expertise, and customer base can boost the overall competitiveness of the newly formed entity, creating challenges for other players in the industry.

Customer Reaction

Customers play a crucial role in determining the success of a merger or acquisition. The way customers perceive and react to the transaction can heavily influence the market position of the companies involved. A positive customer reaction can lead to increased loyalty and trust, while a negative response can result in a loss of customers and market share. Companies must carefully manage customer communication and experience to ensure a smooth transition and favorable customer sentiment following a merger or acquisition.

Frequently Asked Questions Of How Mergers And Acquisitions Can Affect Company

What Is The Impact Of Merger On Organization?

A merger can impact an organization by leading to changes in leadership, structure, and culture. It may also affect employees and stakeholders’ morale and job security.

How Can Mergers And Acquisitions Benefit A Company?

Mergers and acquisitions benefit a company by increasing market share, expanding into new markets, gaining access to new technologies, and reducing competition. This leads to improved operations, increased efficiency, and potentially higher profits, enhancing the company’s overall competitiveness and position in the industry.

What Is A Negative Impact Of A Merger Or Acquisitions?

A negative impact of a merger or acquisition can be a clash of company cultures, leading to employee dissatisfaction and reduced productivity.

Conclusion

Mergers and acquisitions can significantly impact a company’s financial potential and position in the market. Understanding the potential risks and benefits of this process is crucial for companies navigating these waters. It’s important to carefully analyze the potential repercussions and opportunities that come with mergers and acquisitions to ensure long-term success and stability.

Profitability refers to the ability of a business to generate a profit over time, considering expenses and investments. Profit, on the other hand, is the actual amount of money a company earns after deducting all expenses from its total revenue.

Understanding the difference between profitability and profit is essential for businesses to make informed decisions regarding their financial performance. While profit is the actual amount earned, profitability measures the efficiency and sustainability of the business operations. By analyzing both aspects, companies can gauge their overall success and identify areas for improvement.

This distinction helps in shaping long-term strategies to ensure sustained financial health and growth. We will delve deeper into the disparity between profitability and profit and explore their significance in the business world.

Profitability Vs. Profit

Profitability vs. Profit: Understanding the framework of business success entails delving into the crucial distinction between profitability and profit. While both terms are interconnected, they pertain to distinct aspects of a company’s financial health. This blog post aims to elucidate the disparities between profitability and profit, as well as their inherent significance in driving sustainable business growth.

Defining Profit And Profitability

Profit is the tangible surplus earned after subtracting all costs and expenses from total revenue. In contrast, profitability encompasses the capacity of a business to generate sustainable returns relative to investments and operational efficiency.

Key Differences Between Profit And Profitability

Profit represents the absolute financial gain derived from business activities, while profitability gauges the efficiency and effectiveness of these activities in generating returns.

Profits are influenced by short-term sales and cost fluctuations, whereas profitability focuses on long-term viability and value creation.

Importance Of Profit And Profitability

Both profit and profitability are integral metrics that indicate the financial well-being and sustainability of a business. While profit signifies immediate revenue, profitability steers the course for long-term growth and success, serving as a pivotal measure of a company’s financial strength.

Strategies To Improve Profit And Profitability

Enhancing operational efficiency and cost management to bolster profitability.

Implementing targeted marketing and sales tactics to drive revenue growth and maximize profits.

Frequently Asked Questions For What Difference Between Profitability And Profit

What Is The Difference Between Profit And Profitability A Level Business?

Profit is the revenue a business earns, while profitability is the measure of how efficiently a business uses its resources to generate profit. Profit is the actual amount earned, while profitability assesses the relationship between profit and resources utilized.

Why Is Profitability A Better Measure Than Profit?

Profitability is a better measure than profit because it evaluates the efficiency of a company’s operations. It considers the resources used to generate profit, providing a more comprehensive insight into the financial performance. This metric helps assess the sustainability and growth potential of a business.

What Do You Mean By Profitability?

Profitability refers to a company’s ability to generate earnings. It is a measure of how efficiently a business turns its sales into profits. Companies aim to maximize profitability by increasing revenue and minimizing costs.

Conclusion

Understanding the distinction between profitability and profit is crucial for businesses to make informed decisions. Profitability encapsulates the overall financial health, encompassing revenue, expenses, and efficiency. On the other hand, profit is the surplus income after deducting costs. Both are essential metrics to gauge success and ensure sustainable growth in a competitive market.

High Water Mark: Understanding and Preparing for Extreme Floods

In recent years, the increase in extreme weather events has heightened the need for comprehensive preparation and understanding of potential flood risks. High water marks play a crucial role in assessing and managing flood events. This article aims to explain what high water marks are, their significance, and how individuals and communities can prepare for these extreme events.

Credit: corporatefinanceinstitute.com

What are High Water Marks?

In simple terms, a high water mark is the level reached by floodwaters during an extreme or record-setting flood event. It serves as a visual indicator of the highest water level reached and provides valuable information to hydrologists, emergency management agencies, and property owners.

High water marks are commonly measured using permanent markers and are often etched or painted on bridges, buildings, or other structures near bodies of water. These markers help assess the severity of past flood events, study flood patterns, and plan for future flood mitigation measures.

The Significance of High Water Marks

High water marks hold significant importance for several reasons:

1

Historical Data: High water marks provide historical data on the height and intensity of previous floods. This information helps identify flood-prone areas and assists in creating floodplain maps and zoning regulations, ensuring that buildings and infrastructure are appropriately designed and located.

2

Risk Assessment: Knowledge of past flood events allows for better risk assessment and flood modeling. By understanding where the water reached during previous floods, scientists and engineers can estimate potential damage and plan accordingly to protect lives and property.

3

Insurance Claims: High water marks assist in determining flood insurance claims. Insurance companies rely on these markers to verify the water levels and validate insurance claims for individuals and businesses affected by floods.

https://www.youtube.com/watch?v=zr3CDsdFcrk

Preparing for High Water Marks and Extreme Floods

As the frequency and severity of extreme flood events increase, it is essential to be prepared and take preventive measures. Here are some steps individuals and communities can take:

1. Educate Yourself

Learn about the flood risk in your area by accessing local floodplain maps and studying information from hydrological surveys. Understand the different flood warning levels and the actions you need to take at each stage.

2. Develop An Emergency Plan

Prepare an emergency plan that includes evacuation routes, assembly points, and contact information for local authorities. Educate your family members and discuss the plan regularly to ensure everyone knows what to do during a flood event.

3. Maintain Flood Insurance Coverage

Consider obtaining flood insurance coverage if you live in a flood-prone area. Review your policy and make sure it adequately covers your property and belongings. Keep copies of important documents in a safe, waterproof place.

4. Protect Your Property

Raise critical utilities, such as electrical panels, switches, and appliances, above the predicted flood levels. Install backflow valves in plumbing fixtures to prevent sewage backups. Secure important items and furniture on higher levels, or consider elevating them if possible.

5. Stay Informed

Stay updated with the latest weather forecasts, flood warnings, and evacuation orders. Monitor local news, radio, and social media for real-time information. Have a battery-powered or hand-cranked radio as a backup communication device.

6. Engage With The Community

Participate in community-based flood preparedness initiatives. Join local committees or organizations that focus on flood management and collaborate with neighbors to collectively mitigate flood risks in your area.

7. Consult Professionals

Seek guidance from professionals, such as floodplain managers, engineers, and insurance agents, to assess the flood risk to your property accurately. They can provide recommendations regarding flood protection measures, retrofitting options, and improvements to minimize future flood damage.

Credit: twitter.com

Conclusion

Understanding high water marks and their significance is crucial in preparing for extreme flood events. By leveraging historical data, conducting risk assessments, and implementing preventive measures, individuals and communities can stay safe and minimize the impact of floods. Remember, early preparation and swift action are key to reducing the devastating effects of floods and ensuring the well-being of ourselves and our environment.