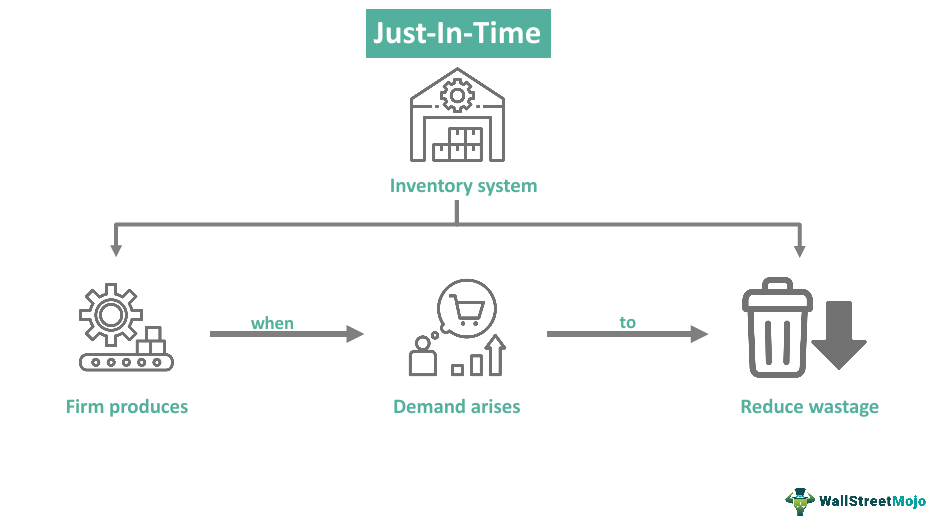

Just In Time (JIT) is a popular inventory management strategy that aims to streamline production processes by minimizing inventory levels and bringing materials or products to the production line exactly when they are needed. This method was first introduced by Toyota in the 1970s and has since been adopted by many industries worldwide.

Credit: www.netsuite.com

How does the Just In Time method work?

The Just In Time method focuses on reducing waste, improving efficiency, and increasing productivity. It involves close coordination with suppliers, as materials are only delivered when they are needed for production. By minimizing inventory levels, companies can free up capital that would otherwise be tied up in inventory costs.

The JIT method relies on accurate demand forecasting and a well-coordinated supply chain. It requires suppliers to have the ability to deliver materials quickly and in small quantities. This enables companies to respond rapidly to changes in customer demand, reduce storage costs, and eliminate the risk of holding obsolete or slow-moving inventory.

Credit: twitter.com

Benefits of the Just In Time method

The Just In Time method offers several benefits to companies who implement it effectively:

Reduced Inventory Costs: By keeping inventory levels low and eliminating the need for excessive storage space, companies can significantly reduce inventory carrying costs.

Improved Cash Flow: With less capital tied up in inventory, companies can allocate their resources to other areas of their business, improving cash flow and financial stability.

Reduced Waste: JIT helps to minimize waste by avoiding overproduction, excess inventory, and unnecessary movement of materials.

Increased Efficiency: By delivering materials or products just in time, companies can optimize production processes and reduce lead times, ultimately increasing overall efficiency.

Enhanced Quality: JIT emphasizes the importance of quality control at each stage of production, reducing the risk of defects and improving overall product quality.

Potential Challenges with JIT

While the Just In Time method offers numerous advantages, it is important to be aware of potential challenges that may arise when implementing this strategy:

Challenge

Solution

Supplier Reliability

Implement effective supplier management and establish strong relationships with reliable suppliers.

Accuracy of Demand Forecasting

Invest in advanced forecasting methods and adopt a data-driven approach to demand planning.

Production Interruptions

Implement contingency plans to address potential production disruptions and ensure backup suppliers are available if needed.

Tightly Coordinated Supply Chain

Ensure effective communication and collaboration between all stakeholders in the supply chain.

By addressing these challenges and implementing appropriate strategies, companies can overcome potential hurdles and fully leverage the benefits of the Just In Time method.

Conclusion

The Just In Time method is an effective approach to inventory management that focuses on reducing waste, improving efficiency, and increasing productivity. By minimizing inventory levels and delivering materials or products just in time, companies can significantly reduce costs, improve cash flow, and enhance overall operational performance. However, it is crucial to carefully plan, coordinate, and address potential challenges to ensure successful implementation of JIT.

Fringe benefits refer to the extra perks employees receive in addition to their regular salary or wages. These benefits are usually offered by employers as a way to attract and retain top talent. They can range from health insurance and retirement plans to flexible work schedules and employee discounts. In this article, we will explore the importance of fringe benefits and why they matter for both employers and employees.

1. Attracting and Retaining Employees

Offering a comprehensive package of fringe benefits can help employers attract and retain skilled employees. In a competitive job market, candidates often consider the overall compensation package when choosing between job offers. Companies that offer desirable benefits have a higher chance of attracting top talent and encouraging employee loyalty.

2. Improved Employee Satisfaction and Morale

Fringe benefits contribute to overall employee satisfaction and morale. When employees feel valued and supported by their employer, they are more likely to be engaged and motivated at work. Benefits such as flexible work hours, paid time off, and wellness programs can enhance work-life balance, reduce stress, and increase job satisfaction.

3. Increased Productivity and Performance

Providing fringe benefits can have a positive impact on employee productivity and performance. Employees who have access to benefits like health insurance and retirement plans tend to have better physical and mental well-being. This, in turn, leads to reduced absenteeism, improved focus, and higher productivity levels.

Credit: fastercapital.com

4. Tax Advantages for Employers and Employees

Both employers and employees can benefit from tax advantages associated with fringe benefits. For employers, certain fringe benefits may be tax-deductible, lowering their overall tax burden. Employees, on the other hand, may enjoy tax exclusions on certain benefits, such as health insurance premiums, reducing their taxable income.

5. Competitive Advantage in the Job Market

Companies that offer attractive fringe benefits gain a competitive advantage in the job market. This is especially true in industries where the demand for skilled workers is high. A comprehensive benefits package can help set employers apart from their competitors, attracting top talent and positioning the company as an employer of choice.

6. Employee Health and Well-being

Fringe benefits that promote employee health and well-being can have long-term benefits for both the employee and the employer. Health insurance coverage, wellness programs, and access to fitness facilities or discounts encourage employees to prioritize their health. This, in turn, reduces healthcare costs, decreases absenteeism, and improves overall employee well-being.

7. Enhancing Work-Life Balance

Flexible work schedules, paid time off, and family-friendly policies are important components of a comprehensive fringe benefits package. These benefits allow employees to balance their work and personal lives effectively. Employees who have a good work-life balance tend to be less stressed and more satisfied, leading to increased loyalty and higher retention rates.

8. Employee Engagement and Loyalty

When employees feel valued and appreciated through fringe benefits, they are more likely to be engaged and loyal to their employer. This translates into lower turnover rates, reduced recruitment and training costs, and a more stable and productive workforce. Employees who receive attractive benefits are also more likely to recommend their company to others.

Credit: www.nitsotech.com

9. Cost Savings for Employees

Fringe benefits can lead to cost savings for employees, particularly in areas such as healthcare and retirement planning. By providing access to group insurance plans and retirement savings programs, employers help employees save money compared to purchasing individual plans. This improves employees’ financial security and overall well-being.

10. Compliance with Employment Laws

Offering fringe benefits ensures compliance with relevant employment laws and regulations. Employers are required to provide certain benefits, such as social security contributions and workers’ compensation, as mandated by law. By offering a comprehensive package of benefits, employers can easily meet legal obligations while also demonstrating their commitment to employees’ welfare.

Conclusion

In conclusion, fringe benefits play a vital role in attracting and retaining employees, improving job satisfaction, enhancing productivity, and gaining a competitive advantage. From a tax perspective, both employers and employees can enjoy advantages associated with these benefits. By offering a comprehensive package of fringe benefits, companies can create a positive work environment, promote employee well-being, and ensure legal compliance.

The secondary market provides liquidity and price discovery for already issued securities. It helps investors to buy and sell securities after the initial offering, enabling a more efficient allocation of capital and reducing transaction costs.

The secondary market plays a crucial role in the financial ecosystem by allowing investors to exit or adjust their positions, providing price transparency, and promoting market efficiency. In today’s dynamic financial landscape, the need for a well-functioning secondary market cannot be overstated.

It serves as a vital platform for investors to trade securities, facilitating the flow of capital and enabling market participants to make informed investment decisions. As a result, the secondary market is essential for maintaining financial stability and ensuring the effective functioning of the overall economy. Understanding the significance of the secondary market is essential for investors and businesses seeking to capitalize on investment opportunities and manage their financial risks effectively.

Importance Of Secondary Market

Importance of Secondary Market:

“`

In the financial world, the secondary market holds significant importance due to its role in providing liquidity and efficiency as well as facilitating price discovery. These aspects make the secondary market essential for investors, companies, and the overall functioning of the economy.

“`html

Liquidity And Efficiency

“`

The secondary market plays a crucial role in providing liquidity, allowing investors to easily buy and sell their securities. This liquidity ensures that investments can be converted to cash without causing significant price changes, which in turn fosters efficiency in the overall financial system. Investors are able to realize the value of their investments quickly, enabling them to react to changing market conditions or to take advantage of new opportunities.

“`html

Price Discovery

“`

An important function of the secondary market is price discovery, which refers to the process of determining the fair market value of securities. Through the trading activities in the secondary market, the prices of securities are constantly being adjusted based on supply and demand dynamics, providing transparent and accurate pricing information. This allows investors to make informed decisions and contributes to the efficient allocation of capital within the economy.

In summary, the secondary market is crucial for providing liquidity and efficiency, as well as facilitating price discovery. These functions contribute to the overall vibrancy and effectiveness of the financial system, making the secondary market an essential component of the investment landscape.

Role In Capital Formation

Why Do We Need Secondary Market: Role in Capital Formation

Access to Capital: When companies issue stocks and bonds in the primary market, it helps them raise initial capital. However, the secondary market plays a crucial role in allowing investors to buy and sell these securities. This liquidity provides companies with ongoing access to capital, as it encourages initial investors to invest in the primary market, knowing they can later sell their holdings if necessary. In turn, this access to capital contributes to economic growth and innovation.

Investor Confidence

Investor confidence is crucial for a well-functioning secondary market. When investors can easily buy and sell securities, it promotes transparency and trust in the market. This confidence leads to greater investment, which further fuels capital formation and economic development.

Impact On Economic Growth

A secondary market plays a crucial role in boosting economic growth by enhancing liquidity and efficiency in the financial markets. It provides investors with an opportunity to buy and sell securities, thus contributing to price discovery and capital formation. Additionally, the secondary market helps in reallocating resources and reducing investment risk, fueling economic progress.

Impact on Economic Growth

The secondary market plays a crucial role in driving economic growth. Its functions have a direct impact on the economy as a whole, influencing job creation and wealth distribution.

Job Creation

The secondary market fosters job creation by providing opportunities for businesses to raise capital for expansion and innovation. Companies can access additional funding by selling securities, subsequently enabling them to invest in new projects and ventures. This expansion drives the need for more employees, contributing to overall job growth.

Wealth Distribution

The secondary market also impacts wealth distribution within the economy. By offering opportunities for individuals to invest and participate in the market, it allows for the distribution of financial resources. This widens the scope for wealth accumulation and fosters a more equitable distribution of economic prosperity.

In summary, the secondary market exerts a significant influence on economic growth through its role in job creation and wealth distribution, ultimately contributing to a more dynamic and prosperous economy.

Regulatory And Supervisory Importance

The secondary market plays a crucial role in ensuring market stability, investor protection, and regulatory oversight. It provides a platform for the trading of existing financial assets, allowing investors to buy and sell securities. The regulatory and supervisory aspects of the secondary market are vital to maintain a fair and transparent trading environment.

Market Stability

The secondary market contributes to market stability by facilitating the efficient allocation of capital and resources. Through the trading of existing securities, it enables investors to adjust their portfolios, thereby enhancing market liquidity. This liquidity helps prevent excessive price volatility and promotes a more stable financial market environment.

Investor Protection

Effective regulatory oversight in the secondary market is essential for investor protection. Regulatory measures such as enforcing transparency in trading, preventing market manipulation, and ensuring fair practices safeguard investors from potential risks and fraudulent activities. This oversight fosters trust and confidence among investors, contributing to the overall integrity of the financial system.

Frequently Asked Questions Of Why Do We Need Secondary Market

What Is The Importance Of Secondary Market?

The secondary market is important for providing liquidity and price discovery for existing securities. It allows investors to buy and sell assets, promoting market efficiency and attracting new capital. This helps companies raise funds and allows investors to exit their positions when needed.

What Is The Main Objective Of Secondary Market?

The main objective of the secondary market is to provide a platform for buying and selling already issued securities. It enables investors to trade stocks, bonds, and other financial instruments, facilitating liquidity and price discovery.

What Is The Primary Benefit Of The Secondary Market?

The primary benefit of the secondary market is the opportunity to buy and sell previously issued securities. This provides liquidity and flexibility for investors.

Conclusion

To sum up, the secondary market plays a crucial role in maintaining liquidity and promoting market efficiency. It provides investors with an avenue to buy and sell securities after their initial issuance. The ability to trade existing assets contributes to price discovery, reduces price volatility, and stimulates overall market activity.

Embracing the secondary market is essential for a thriving economy.

Basel Accords: Strengthening Global Financial Stability

The Basel Accords are a set of international banking regulations aimed at enhancing the stability and integrity of the global financial system. Established by the Basel Committee on Banking Supervision (BCBS), these accords provide a framework for banks to assess and manage various types of risks they face.

Basel I: The Foundation of Regulatory Framework

Basel I, introduced in 1988, was the first international regulatory framework that focused on establishing minimum capital requirements for banks. It required banks to hold capital equivalent to at least 8% of their risk-weighted assets. This simple risk-based approach was a major step forward in addressing concerns about inadequate capitalization and risk management.

Basel II: A More Comprehensive Approach

Basel II, implemented in 2004, aimed to improve the accuracy and risk sensitivity of the capital adequacy framework. It introduced three pillars:

Pillar 1: Minimum capital requirements based on the level of credit, market, and operational risks

Pillar 2: Supervisory review process to ensure banks have adequate capital to cover all risks

Pillar 3: Increased disclosure and transparency to enhance market discipline

These pillars provided a more holistic approach to banking supervision and risk management.

Basel III: Strengthening the Global Financial System

Basel III, introduced as a response to the 2007-2008 financial crisis, focused on further strengthening the resilience of banks and the global financial system. It introduced a range of new measures:

Higher minimum capital requirements: Banks are required to hold more and better-quality capital to withstand financial shocks.

Leverage ratio: A supplementary measure to limit excessive leverage and strengthen risk control.

Liquidity requirements: Banks must maintain sufficient liquidity buffers to withstand periods of stress.

Countercyclical buffer: A tool to increase capital requirements during periods of excessive credit growth to prevent future crises.

Basel III aimed to reduce the probability and impact of future financial crises by promoting stability, risk management, and the soundness of financial institutions.

https://www.youtube.com/watch?v=ukJXHbs7HOw

Credit: www.mdpi.com

Impact on the Global Financial Landscape

The Basel Accords have had a significant impact on the global financial landscape. By establishing common international standards, they promote a level playing field for banks worldwide and reduce the potential for regulatory arbitrage.

However, critics argue that the Basel Accords may have unintended consequences. Some banks may try to lower their risk-weighted assets or engage in regulatory arbitrage to circumvent the requirements.

Credit: fastercapital.com

Conclusion

The Basel Accords play a crucial role in strengthening global financial stability. They provide a framework for banks to assess and manage risks, ensuring that they maintain sufficient capital buffers to withstand economic downturns. While there are ongoing discussions on potential improvements, the accords have significantly enhanced the resilience and risk management capabilities of banks worldwide.

A Certified Reverse Mortgage Professional is an expert who has undergone specialized training and certification to assist individuals in navigating the complexities of reverse mortgages. With their knowledge and expertise, they can provide guidance and support throughout the reverse mortgage process, ensuring clients make informed decisions that align with their financial goals and circumstances.

What Is A Certified Reverse Mortgage Professional?

Certified Reverse Mortgage Professional

A Certified Reverse Mortgage Professional (CRMP) is a knowledgeable and experienced individual who has undergone specific training and met stringent requirements in the field of reverse mortgages. They play a crucial role in assisting seniors in understanding and utilizing reverse mortgage options for their financial needs.

Qualifications And Training

CRMPs undergo thorough training and must pass a rigorous exam to acquire certification. They are required to have a minimum of two years of experience in the reverse mortgage industry and demonstrate their commitment to ethical conduct and professional standards. Additionally, they must participate in continuing education to maintain their CRMP designation, ensuring that they stay updated with industry regulations and best practices.

Role And Responsibilities

CRMPs are responsible for guiding seniors through the complexities of reverse mortgages. They provide expert advice on the various options available, conduct assessments to determine suitability, and educate clients on the potential benefits and risks associated with reverse mortgages. Furthermore, they assist in the application process and ensure compliance with all relevant laws and regulations, ultimately empowering seniors to make informed decisions about their financial future.

Benefits Of Hiring A Certified Reverse Mortgage Professional

When it comes to navigating the complex landscape of reverse mortgages, working with a Certified Reverse Mortgage Professional can provide invaluable expertise and peace of mind. These professionals are well-equipped with the knowledge and skills to guide you through the intricacies of reverse mortgage transactions, ensuring a seamless and compliant process.

Expert Advice

Certified Reverse Mortgage Professionals offer expert advice tailored to your specific financial needs. They possess in-depth knowledge of reverse mortgage products and can provide personalized guidance to help you make informed decisions about your financial future. With their expertise, you can navigate the complexities of reverse mortgage transactions with confidence and clarity.

Ensuring Compliance

When engaging the services of a Certified Reverse Mortgage Professional, you can rest assured that your transaction will adhere to the highest compliance standards. These professionals stay abreast of regulatory changes and ensure that all aspects of the reverse mortgage process comply with industry regulations. By entrusting your transaction to a certified professional, you minimize the risk of compliance-related issues and enjoy a smooth, worry-free experience.

https://www.youtube.com/watch?v=vCN0zXIoTNs

Choosing The Right Certified Reverse Mortgage Professional

Certified Reverse Mortgage Professionals play a crucial role in providing expert guidance and support to seniors seeking to unlock the equity in their homes through reverse mortgages. It’s vital to choose the right professional who possesses the experience, expertise, and client testimonials that instill confidence in their ability to assist in this complex financial decision.

Experience And Expertise

When selecting a Certified Reverse Mortgage Professional, it’s essential to prioritize experience and expertise. Look for individuals who have a proven track record in the industry and possess a deep understanding of reverse mortgages. Experience indicates the proficiency to navigate the complexities of reverse mortgage transactions, while expertise demonstrates a comprehensive understanding of the various options available and the ability to provide tailored solutions to meet individual needs.

Client Testimonials

Client testimonials offer valuable insights into the quality of service provided by a Certified Reverse Mortgage Professional. These testimonials reflect the experiences of real individuals who have benefited from the guidance and support of the professional. Seek professionals with a strong portfolio of client testimonials that highlight their commitment to client satisfaction and their ability to deliver positive outcomes in the realm of reverse mortgages.

The Future Of Certified Reverse Mortgage Professionals

As the financial landscape continues to evolve, so do the roles and responsibilities of certified reverse mortgage professionals. The future holds exciting opportunities for professionals in this field, with industry trends indicating a growing demand for their expertise and an array of potential growth avenues. Let’s explore the promising future of certified reverse mortgage professionals and the opportunities that lie ahead.

Industry Trends

Keeping abreast of industry trends is crucial for certified reverse mortgage professionals as it enables them to adapt to changing market dynamics and align their strategies with current demands. The future will witness a surge in demand for customized reverse mortgage solutions, driven by evolving consumer preferences and the need for tailored financial products.

Opportunities For Growth

Certified reverse mortgage professionals can look forward to an array of opportunities for growth, with an increasing focus on personalized financial planning and retirement solutions. The rise of digital platforms and technological advancements also presents avenues for professionals to streamline processes and enhance customer experiences, leading to greater market penetration and client acquisition.

Frequently Asked Questions Of Certified Reverse Mortgage Professional

Who Is The Best Person To Talk To About Reverse Mortgages?

You should talk to a licensed mortgage professional about reverse mortgages. They can provide personalized guidance and advice.

What Is The Average Commission On A Reverse Mortgage?

The average commission on a reverse mortgage is typically around 2% of the home’s value. This fee covers lender costs and is negotiable.

What Suze Orman Says About Reverse Mortgages?

Suze Orman advises caution with reverse mortgages due to high fees and risks involved. She suggests exploring other options first.

Conclusion

In a nutshell, working with a Certified Reverse Mortgage Professional gives you peace of mind. Their expertise ensures a smooth and trustworthy process, leaving you confident in your financial decisions. With their guidance, you can make the most of your home equity, securing a comfortable and stable future.

In the digital age, the concept of network effect has gained significant importance. With the rapid growth of technology and the internet, understanding the network effect has become crucial for businesses and individuals alike. In this article, we dive deep into the concept of network effect, its impact, and how it can influence the success of different platforms and businesses.

What is Network Effect?

Network effect, also known as network externality, is a phenomenon that occurs when the value of a product or service increases as more people use it. In simpler terms, it’s the idea that the more users or participants a network has, the more valuable it becomes to each individual user.

Let’s take social media platforms as an example. When Facebook started, it was merely a platform for college students to connect and share information. However, as more users joined the platform, the value for each user increased exponentially. With a larger user base, Facebook became more attractive for individuals to connect with friends, join groups, and share content. This led to more growth, attracting even more users, resulting in a positive feedback loop.

Credit: www.linkedin.com

Credit: medium.com

Types of Network Effects

There are different types of network effects, and understanding them is key to harnessing their power:

Direct Network Effects: This occurs when the value of a product or service increases for users as more users join the same network. Examples include social media platforms, where more users mean a better experience for everyone.

Indirect Network Effects: In this case, the value of a product or service increases as more complementary products or services become available. For example, the value of a video game console increases as more game developers create games for it, attracting more users.

Two-Sided Network Effects: This occurs when a platform benefits from having two distinct user groups that interact with each other. An example of this is a credit card network, which needs both cardholders and merchants for successful transactions to take place.

Local Network Effects: In certain situations, network effects can be limited to a specific geographical area. Ride-sharing services like Uber and Lyft rely on local network effects, where more drivers and riders in a specific city lead to improved availability and convenience.

Benefits of Network Effects

The network effect brings numerous benefits to businesses and platforms:

Increased User Base: As more users join a network, it attracts even more users, leading to exponential growth potential.

Higher Value: With a larger user base, the value of a product or service increases for both existing and new users.

Competitive Advantage: Businesses that harness network effects can establish a significant competitive advantage, making it challenging for competitors to replicate their success.

Lock-In: Once a network effect is established, it becomes difficult for users to switch to an alternative platform, creating a sense of “stickiness” and reducing churn.

Challenges and Considerations

While network effects can be immensely beneficial, there are certain challenges and considerations to keep in mind:

Critical Mass: Achieving critical mass, the point where network effects truly kick in, can be challenging. It often requires significant investment, marketing efforts, and patience.

Competition: If a strong competitor with a well-established user base already exists in a certain market, breaking into that market can be difficult, even with the network effect theory in mind.

Platform Maintenance: As a network grows, maintaining and scaling the platform becomes increasingly complex. Ensuring seamless user experiences and avoiding network congestion requires continuous investment and infrastructure development.

Conclusion

The network effect is a powerful concept that plays a significant role in the success of platforms and businesses in the digital age. Understanding and leveraging network effects can drive exponential growth, increase value, and establish a competitive advantage. However, it’s important to consider the challenges and efforts required to achieve critical mass and sustain the network effect over time.