Robo-advisors are indeed the future, offering automated investment services and personalized financial advice. In today’s rapidly evolving financial landscape, the rise of robo-advisors has been remarkable.

With their ability to provide automated investment services and personalized financial advice, robo-advisors have emerged as a crucial component of the future of finance. These technology-driven platforms utilize algorithms to analyze vast amounts of data and make investment decisions based on individual risk preferences and goals.

By eliminating the need for human intermediaries, robo-advisors offer cost-effective and efficient investment solutions for both novice and experienced investors. Moreover, they provide convenient access to diversified portfolios and rebalancing options. As technology advances and more investors seek convenient, reliable and affordable financial services, the popularity and significance of robo-advisors are bound to grow. Their immense potential to democratize investment management and promote financial inclusion makes them a vital player in shaping the future of finance.

Credit: upsiide.com

Understanding The Role Of Robo-Advisors In The Modern World

Robo-advisors have emerged as a game-changer in the modern world, revolutionizing the way we invest. These automated platforms utilize complex algorithms to provide personalized financial advice without the need for human intervention. The concept of robo-advisors has evolved over the years, paving the way for technological advancements and improved user experiences.

One of the significant benefits of using robo-advisors for investors is the accessibility and affordability they offer. With lower fees and minimum investment requirements, robo-advisors have opened up investment opportunities to a broader range of individuals. Furthermore, robo-advisors address common misconceptions surrounding automated investing, such as concerns about the lack of human touch and expertise.

The truth is, these platforms combine the best of both worlds by incorporating technology with human oversight. Robo-advisors are here to stay, providing efficient and reliable investment solutions for the future.

Robo-Advisors Vs Traditional Financial Advisors: Examining The Key Differences

Robo-advisors and traditional financial advisors have some key differences in investment management. While automated platforms use algorithms to guide investment decisions, human advisors provide personalized guidance. It’s important to analyze the costs involved before choosing between the two. Robo-advisors often have lower fees compared to traditional advisors, making them more cost-effective for many investors.

However, factors such as complexity of financial goals and the need for human interaction should also be considered. When it comes to selecting an advisor, it’s essential to evaluate your investment needs, risk tolerance, and desired level of involvement. By comparing the benefits and drawbacks of both robo-advisors and traditional advisors, investors can make an informed decision that aligns with their specific requirements.

Whether the robo-advisors will dominate the future or not, that remains to be seen.

Exploring The Future Potential Of Robo-Advisors

Robo-advisors are gaining traction as a potential future in the world of investing. With advancements in technology, these automated platforms are leveraging artificial intelligence and machine learning to enhance investment strategies. The potential impact of robo-advisors extends beyond individual investors to the entire financial industry.

These platforms have the capability to analyze vast amounts of data and provide personalized investment advice at lower costs compared to traditional financial advisors. As the market continues to embrace digitalization, robo-advisory services have the opportunity to reshape the way people manage their finances.

By leveraging technology, robo-advisors can offer efficient and convenient investment solutions, appealing to a broad range of investors. The future appears promising for these automated systems, bridging the gap between technology and finance, and democratizing investment opportunities.

Regulatory Challenges And Consumer Protection In The Robo-Advisory Space

Robo-advisors have gained popularity in recent years as a technology-driven solution for financial management. However, the regulatory challenges surrounding these platforms cannot be ignored. The regulatory framework surrounding robo-advisory services needs to ensure transparency and accountability. It is essential to safeguard investors’ interests and protect them from potential risks.

Consumer protection agencies play a crucial role in monitoring and enforcing regulations in the robo-advisory space. They aim to create a secure environment that fosters trust between investors and these automated platforms. By examining the regulatory framework and understanding the role of consumer protection agencies, we can ensure the future viability of robo-advisors as a convenient and reliable investment option.

The Human Touch In A Digitized World: Blending Traditional And Robo-Advisory Services

Robo-advisors have gained significant attention as potential players in the future of wealth management. However, to maintain the human touch, it is essential to blend traditional advisory services with these digital platforms. By adopting hybrid approaches, financial professionals can capitalize on the benefits of both robo-advisors and human advice, ensuring a personalized and customized experience for clients.

Robo-advisory platforms offer a range of options, empowering investors to make informed decisions based on their unique goals and risk tolerance. As these platforms continue to evolve, the role of financial professionals has also shifted. They now play a crucial role in providing guidance and expertise, helping clients navigate the complex investment landscape.

Embracing the incorporation of robo-advisors allows for operational efficiency and improved scalability while maintaining the necessary human element. In an age where technology shapes our lives, it is essential to strike a balance between digitization and personalized service in wealth management.

Are Robo-Advisors The Future? Key Takeaways

The future of robo-advisors in the financial world is uncertain but promising. Investors must consider the advantages and limitations of robo-advisory services before embracing this technology. On one hand, robo-advisors offer convenience, low fees, and a streamlined investment process. They provide personalized recommendations based on algorithms and data analysis.

On the other hand, robo-advisors lack the human touch and personalized advice that traditional advisors offer. Investors should also consider the potential risks associated with relying solely on automated investment platforms. Factors such as market volatility, limited investment options, and the potential for technical glitches should be considered.

While robo-advisors have gained traction in recent years, it remains to be seen whether they will replace traditional financial advisors entirely. Nonetheless, it is wise for investors to evaluate their risk tolerance and financial goals before deciding whether to embrace this emerging technology.

Frequently Asked Questions Of Are Robo-Advisors The Future?

Are Robo-Advisors Safe To Use?

Robo-advisors are generally safe to use as they employ advanced security measures to protect your personal and financial information. However, it’s essential to choose a reputable platform that is regulated and has a solid track record in the industry.

How Do Robo-Advisors Work?

Robo-advisors use algorithms and artificial intelligence to automate the investment process. They analyze your financial goals, risk tolerance, and investment horizon to create a diversified portfolio of low-cost exchange-traded funds (etfs). They also handle portfolio rebalancing and offer ongoing investment advice.

Can Robo-Advisors Outperform Human Financial Advisors?

While robo-advisors can provide low-cost and efficient investment solutions, they may not offer the personalized touch and human expertise that human financial advisors provide. Human advisors can adapt to market changes, offer tailored advice, and build relationships, which may give them an edge, especially during uncertain times.

Conclusion

Robo-advisors have undoubtedly emerged as a game-changer in the financial industry. With their advanced algorithms, personalized recommendations, and low fees, they offer a convenient and affordable solution for investors of all levels. As technology continues to advance, it is highly likely that robo-advisors will become an integral part of the future of investing.

In the ever-evolving world of finance, it is essential to embrace the opportunities that technology brings. Robo-advisors have proven their effectiveness at streamlining the investment process and making it accessible to a wider audience. With their ability to automate asset allocation, rebalancing, and tax optimization, they provide a level of efficiency that traditional advisors often struggle to match.

However, it is worth noting that while robo-advisors offer numerous benefits, they may not be suitable for everyone. Investors with complex financial situations or those who value the human touch may still prefer the guidance of a traditional advisor. Nonetheless, it is clear that robo-advisors have revolutionized the industry and will continue to shape the future of investing.

The rise of robo-advisors signals a paradigm shift in the way individuals approach investing. By leveraging technology and automation, these platforms have democratized access to professional investment advice. As technology continues to advance and consumer preferences evolve, robo-advisors are poised to become an integral part of the financial landscape.

Whether you are a novice investor or an experienced one, it is worth considering the benefits that robo-advisors can offer in terms of convenience, cost-effectiveness, and personalized recommendations. However, it is important to note that robo-advisors may not suit everyone’s needs, and there will always be a place for traditional advisors.

Ultimately, the choice between robo-advisors and traditional advisors depends on individual preferences and financial goals.

In a progressive move that resonates with the government’s commitment to the well-being of its citizens, Bangladesh has introduced the Universal Pension Scheme (UPS). This groundbreaking initiative marks a significant stride towards securing financial stability and social protection for a diverse range of individuals across the country. As we delve into the intricacies of this comprehensive pension system, it becomes apparent that UPS brings forth a plethora of benefits that hold the potential to transform lives, uplift communities, and contribute to a more secure future for all.

Benefits of UPS in Bangladesh

Addressing the Imperative for Social Security: As demographic shifts continue to redefine societies worldwide, the need for a robust social security framework becomes increasingly evident. Bangladesh is no exception to this trend, with an aging population necessitating comprehensive measures to ensure financial stability for its citizens, particularly in their old age. The UPS responds to this imperative by offering a well-structured pension system that caters to the needs of various segments of the population, encompassing individuals engaged in diverse occupations and income levels.

Demographic Changes and Aging Population: The demographic landscape of Bangladesh is undergoing significant transformations. The average life expectancy has risen to 73 years, reflecting improved socio-economic conditions. However, this increased longevity also highlights the vulnerability of the elderly population, particularly in the absence of an old-age support mechanism. The elderly are often left financially unstable due to reduced earning capacity post-retirement. This situation is further compounded by the prevalence of low-income and informal sectors, where traditional pension options are scarce. The UPS addresses these vulnerabilities, offering a safety net that empowers citizens engaged in various professions to retire with dignity and financial security.

Inclusivity at the Core: One of the standout features of UPS is its commitment to inclusivity. The system is designed to cover citizens across a wide age range, starting from 18 years old. This inclusivity ensures that individuals from diverse backgrounds and stages of life can access the benefits of the scheme. Moreover, UPS extends its reach beyond national borders, accommodating expatriate Bangladeshis who contribute significantly to the country’s economy. This recognition of the diaspora’s contributions underscores the government’s dedication to safeguarding the interests of all citizens, regardless of their geographic location.

Tailored Schemes for Diverse Needs: The UPS is not a one-size-fits-all solution. Instead, it offers four distinct pension schemes that cater to the specific requirements of different occupational categories. The Progoti, Probash, Shurokkha, and Samata schemes provide varying levels of monthly pensions, ensuring that individuals from private sectors, expatriates, self-employed individuals, informal sector workers, and even the ultra-poor can find a scheme that suits their needs. This tailored approach emphasizes the government’s commitment to promoting economic well-being across all segments of society.

Empowerment and Security for the Elderly: The elderly population often faces financial instability due to reduced earning capacity and lack of pension options. The UPS tackles this challenge head-on by offering survivor benefits. In the unfortunate event of a pensioner’s passing before the age of 75, the nominee of the pensioner is entitled to receive a monthly pension for the remaining period. This provision not only supports the pensioner’s dependents but also ensures that their financial contributions do not go to waste.

Flexibility for Late Entrants: Recognizing that some individuals might join the scheme later in life, the UPS accommodates citizens above the age of 50 under special consideration. These late entrants can still participate in the scheme and, upon meeting certain conditions, receive a lifetime pension. This flexibility acknowledges the diverse circumstances of individuals and ensures that the benefits of the UPS are accessible to as many citizens as possible.

Tax Benefits and Long-Term Stability: The UPS offers tax benefits that encourage individuals to engage with the scheme as a form of investment. The monthly pension received from the scheme is exempt from income tax, enabling pensioners to fully enjoy their contributions during retirement. Additionally, the individual pension accounts allocated to each participant ensure transparency, accountability, and a sense of ownership, contributing to the long-term stability of the system.

A Comprehensive Vision Realized: The inauguration of the UPS is not just a symbolic gesture; it signifies the government’s dedication to securing the financial well-being of its citizens across diverse occupations and life stages. This visionary initiative aligns with the government’s commitment to social security, economic stability, and inclusive development. By providing a safety net for the elderly and those engaged in low-income and informal sectors, the UPS addresses pressing socio-economic challenges and paves the way for a more secure and prosperous future.

As Bangladesh takes its place among nations prioritizing the welfare of their citizens, the Universal Pension Scheme emerges as a beacon of hope, empowerment, and progress. This all-encompassing system has the potential to transform lives, provide financial security, and contribute to the nation’s journey towards becoming an advanced and equitable society. The UPS isn’t just a pension scheme; it’s a testament to the government’s commitment to its people and a powerful step towards a better and more secure future for all.

Fostering Inter-Generational Solidarity: The introduction of the Universal Pension Scheme in Bangladesh serves as a bridge between generations, promoting inter-generational solidarity. As younger citizens witness the government’s commitment to ensuring a secure future for the elderly, a culture of care and support is nurtured. This scheme not only uplifts the lives of the elderly but also instills a sense of responsibility and empathy among the younger population, fostering a harmonious society where citizens collectively contribute to the well-being of all age groups.

Reducing Dependence on Family Support: The UPS provides an essential safety net for individuals who may otherwise be dependent on their families for financial support during old age. By offering a reliable source of income post-retirement, the scheme lessens the burden on younger family members, enabling them to pursue their own goals and aspirations without the constant worry of providing for their elderly relatives.

Enhancing Gender Equality: The UPS plays a significant role in promoting gender equality. Women, particularly those engaged in informal sectors, often face financial vulnerabilities due to the absence of pension options. By extending the benefits of the UPS to women, the government empowers them to retire with dignity and security. This step towards gender inclusivity not only enhances economic equality but also contributes to a more equitable society.

Stimulating Economic Growth: The UPS holds the potential to stimulate economic growth in Bangladesh. As elderly citizens receive a steady pension, their purchasing power remains intact, contributing to local economies. This increased spending power can boost demand for goods and services, subsequently creating opportunities for businesses to expand and thrive. This virtuous cycle of economic growth and stability benefits individuals, communities, and the nation as a whole.

Boosting Entrepreneurship: The financial security provided by the UPS can encourage individuals to explore entrepreneurial ventures without the fear of financial instability during retirement. Aspiring entrepreneurs from diverse backgrounds can embark on business ventures, contributing to job creation, innovation, and economic diversification. This, in turn, supports the government’s broader goals of fostering economic development and reducing unemployment.

Promoting Health and Well-Being: Financial stress during old age can have a negative impact on an individual’s overall health and well-being. The UPS addresses this concern by offering a consistent source of income that alleviates financial worries, allowing pensioners to focus on maintaining their health and enjoying their retirement years. By promoting better health outcomes, the scheme contributes to reducing the burden on the healthcare system.

Ensuring Peace of Mind: One of the most significant intangible benefits of the UPS is the peace of mind it offers to citizens. Knowing that they have a reliable pension to rely on during their retirement years provides a sense of security and tranquility. This peace of mind extends beyond the pensioner to their families, creating a positive ripple effect that enhances the overall quality of life for all involved.

Building Trust in the Government: The implementation of the UPS reinforces citizens’ trust in the government’s commitment to their welfare. This groundbreaking initiative showcases the government’s responsiveness to the changing needs of its people and its dedication to ensuring a secure future for all citizens. By delivering on its promises, the government fosters a stronger bond with the population, enhancing overall governance and social cohesion.

Inspiring Long-Term Planning: The UPS encourages citizens to engage in long-term financial planning. As individuals contribute to their pension accounts, they become more attuned to the importance of saving for their future. This newfound awareness of financial planning can extend beyond the pension scheme, influencing other aspects of individuals’ financial decisions, such as investment and asset management.

Elevating Bangladesh’s Global Standing: The introduction of the UPS positions Bangladesh as a nation that prioritizes social welfare, economic inclusivity, and progressive policies. This commitment to citizens’ well-being contributes to the nation’s international reputation and can attract foreign investment, partnerships, and collaborations that align with Bangladesh’s dedication to a prosperous and equitable society.

Incentivizing Non-Resident Bangladeshis (NRBs): The Universal Pension Scheme’s benefits extend even to non-resident Bangladeshis (NRBs). The scheme offers NRB participants an attractive incentive of an additional 2.5% on their contributions if they choose to contribute in foreign currencies. This incentive mirrors the practice in place for remittances through formal channels. By providing this incentive, the government aims to encourage more expatriate Bangladeshis to join the pension scheme. This forward-looking approach not only secures the financial future of expatriates but also augments the inflow of foreign exchange into the country. The scheme, therefore, plays a dual role in ensuring the well-being of expatriates and boosting Bangladesh’s foreign exchange reserves.

Catalyzing Foreign Exchange Reserves: Expatriate Bangladeshis hold a pivotal role in contributing to the country’s foreign exchange reserves. Through their remittances, they support their families and communities back home. By introducing the Universal Pension Scheme, the government leverages this dynamic to enhance the country’s forex reserves further. Expatriates’ contributions to the scheme, particularly in foreign currencies, bolster the national forex reserves. This strategy aligns with the government’s comprehensive approach to economic stability and reinforces Bangladesh’s resilience in times of global economic fluctuations.

Flexible Participation for Citizens Above 50: The Universal Pension Scheme addresses the unique needs of citizens above the age of 50 who were initially excluded from pension benefits at the age of 60. Under the new rules, individuals above 50 have an opportunity to participate in the program. While they won’t receive pension benefits at 60 like others, they are eligible for lifelong pensions after contributing for 10 years. This inclusivity acknowledges the diverse circumstances of citizens and ensures that no one is left behind. It underscores the government’s commitment to offering a safety net for individuals at various stages of life, promoting financial security and dignity for all.

Encouraging Long-Term Planning and Lifelong Pensions: The Universal Pension Scheme encourages citizens to adopt a long-term perspective on their financial well-being. By contributing consistently from the age of 18 to 60, individuals receive a pension that reflects their dedication to securing their future. Those initiating contributions at a later age, such as 30, can still accumulate a significant pension by the time they reach 60. Additionally, the scheme allows individuals who begin contributing at 60 to start receiving pensions at 70. This flexible approach underscores the importance of planning for the long term and rewards individuals for their commitment to financial security.

Promoting Financial Discipline and Tax Efficiency: The scheme’s provision for an 8% annual interest on contributions acts as an incentive for citizens to save and invest in their future. This disciplined approach to saving fosters financial literacy and responsibility among citizens, instilling a culture of long-term planning. Furthermore, the scheme recognizes the contributions as investments, allowing participants to enjoy tax benefits. Not only do individuals secure their financial future, but they also enjoy tax rebates on their contributions, making the scheme a holistic financial planning tool.

Incorporating these additional benefits into the Universal Pension Scheme enriches its scope and impact, making it a comprehensive and dynamic initiative that addresses the multifaceted financial needs of Bangladesh’s citizens. As the scheme’s launch approaches, its influence is set to resonate across the nation, empowering individuals, families, and communities to embrace a more secure and prosperous future.

In conclusion, the Universal Pension Scheme in Bangladesh goes beyond providing mere financial security; it enriches lives, strengthens communities, and paves the way for a more inclusive and harmonious society. By addressing vulnerabilities, empowering individuals, and promoting economic growth, the UPS becomes a catalyst for positive change. As the nation embarks on this transformative journey, the benefits of the UPS ripple through the fabric of society, touching every citizen and contributing to a brighter and more secure future for all.

As Bangladesh undergoes economic transformation and demographic changes, the need for a comprehensive social security system becomes increasingly pronounced. The Universal Pension Scheme (UPS) has gained attention as a potential solution to address the financial needs of senior citizens. However, implementing such a scheme is not without its challenges. This study delves into the challenges of UPS in Bangladesh, shedding light on the obstacles that need to be navigated.

Challenges of UPS in Bangladesh

The Universal Pension Scheme (UPS) is a government-run pension program that aims to provide financial security for the elderly in Bangladesh. However, there are a number of challenges to the implementation of the UPS, including weak governance, a lack of digitization, and a diverse population.

Qualitative research methods were employed to delve into the challenges of implementing the UPS. In-depth interviews were conducted with relevant personnel who possess insights into public financial management reforms and social welfare initiatives. Some insights were collected from social media to get opinions from the people. The challenges were categorized into three groups:

Challenges from Participants and Recipients

Registration and Trust Issues: The challenge of registration and building trust is multifaceted. Bangladesh’s history of administrative complexities and discrepancies in resource distribution has led to skepticism among the population. Many citizens have experienced difficulties accessing benefits from previous welfare programs due to flawed registration processes. Therefore, instilling trust in the new UPS system is paramount. Clear and transparent registration processes, along with effective communication campaigns to inform citizens about the scheme’s benefits and eligibility criteria, are necessary.

Informal Sector Dominance: A significant portion of Bangladesh’s workforce operates in the informal sector, characterized by cash-based transactions and irregular income patterns. Convincing individuals from this sector to commit a portion of their income to a pension scheme can be challenging. The irregular nature of their income might lead them to prioritize immediate needs over long-term savings. To address this challenge, the UPS needs to offer flexible contribution options that align with the income patterns of the informal sector. Moreover, financial literacy campaigns can play a crucial role in educating informal sector workers about the long-term benefits of pension savings.

Private Sector Participation: Encouraging private sector enterprises to contribute to the UPS has proven difficult due to various reasons, including financial constraints and a lack of awareness about the scheme’s advantages. Offering incentives such as tax benefits or government contributions to match those of private enterprises could make participation more attractive. Collaborative efforts between the government and private sector stakeholders are essential to drive participation and ensure a sustainable pension system for employees in the private sector.

Mental Shift on Savings: Changing the mindset of Bangladeshi citizens regarding savings and retirement planning is a significant challenge. Historically, savings have been associated with immediate needs and emergencies rather than long-term security. To overcome this challenge, educational campaigns and workshops should focus on the importance of retirement planning and the benefits of contributing to the UPS. Stories of successful retirees who have benefited from pension schemes can serve as inspiring examples.

Gender and Demographic Diversity: Bangladesh’s demographic landscape is characterized by gender disparities and varied life expectancies. Women tend to outlive men, and their participation in formal employment is lower. Therefore, the UPS must take these disparities into account by tailoring benefits to reflect gender-specific needs. Providing options for flexible retirement ages and addressing the financial needs of single and elderly women can ensure gender equality in social protection schemes.

Addressing Vulnerable Groups: Bangladesh faces the challenge of river erosion and natural calamities that lead to land loss, rendering many individuals landless and vulnerable. Identifying and incorporating these vulnerable groups into the UPS is crucial. Innovative approaches, such as leveraging community-based organizations and local government bodies, can aid in identifying and supporting these marginalized citizens. Customized pension schemes that provide higher benefits for vulnerable groups can ensure their inclusion in the UPS and provide a safety net against the uncertainties they face.

Navigating these challenges requires a multi-pronged approach that involves collaboration between government agencies, private sector entities, civil society organizations, and international development partners. By addressing these challenges systematically, Bangladesh can work towards the successful implementation of the Universal Pension Scheme and ensure a more secure and dignified retirement for its citizens.

Institutional and Governance Challenges

Accountability and Transparency: One of the prominent challenges in implementing the UPS in Bangladesh lies in ensuring accountability and transparency in fund management. The country has witnessed instances of mismanagement and corruption in the distribution of welfare benefits. To overcome this challenge, the government needs to establish robust mechanisms for monitoring the flow of funds, ensuring that the allocated resources reach the intended recipients without any leakages or irregularities. Implementing digital platforms for fund management, where beneficiaries can track their contributions and benefits, can enhance transparency and accountability.

Integration with Existing Reforms: Bangladesh has been undergoing various reforms in the public sector, including the adoption of digital platforms for financial management. Ensuring seamless integration between the UPS and these ongoing reforms is crucial. The challenge here is to align the pension scheme’s operational processes with the existing digitalization efforts. This requires careful coordination between different government departments and agencies involved in these reforms to create a unified and effective system.

Efficient Fund Management: Effective management of the pension fund is essential to ensure that contributions are invested prudently and generate reasonable returns. Bangladesh’s banking sector has faced challenges in terms of governance and efficiency. Therefore, it is imperative to establish stringent guidelines for fund investment, appoint experienced fund managers, and regularly monitor their performance. The development of a robust investment strategy and risk management framework will be critical to safeguarding pension funds and maximizing returns.

Digitization Challenges: While Bangladesh has been making strides towards digital transformation in public services, challenges remain. The successful implementation of the UPS hinges on a digitized infrastructure for registration, contribution collection, and benefit distribution. Ensuring that digital platforms are user-friendly, secure, and accessible to all citizens, including those in remote areas, is a significant challenge. Adequate training and support must be provided to both beneficiaries and administrators to effectively utilize the digital system.

Public Perception and Participation: The success of the UPS depends on the public’s perception of the scheme’s benefits and effectiveness. If citizens perceive the pension system as cumbersome or ineffective, it might deter their participation. Establishing a positive image of the UPS requires effective communication campaigns that highlight the scheme’s advantages and address misconceptions. Engaging with citizens, civil society organizations, and community leaders to gain their trust and involvement is crucial for the scheme’s long-term sustainability.

Religious Challenges of the Universal Pension Scheme (UPS) in Bangladesh:

The introduction of the Universal Pension Scheme (UPS) in Bangladesh marks a commendable effort towards providing financial security to citizens during their retirement years. However, it’s important to address the religious challenges that arise from the current structure of the scheme, particularly in the context of Islamic principles.

1. Concerns of Riba (Usury) and Garar: One of the main religious challenges associated with the UPS in Bangladesh is the concern of riba, which refers to usurious transactions involving interest. Islamic finance principles strictly prohibit engaging in transactions that involve riba. The conventional structure of the UPS, which involves citizens depositing money at a fixed rate and receiving additional money in the form of a pension, resembles an interest-based transaction.

2. Need for Interest-Free Alternative: Given that a significant portion of the population in Bangladesh adheres to Islamic beliefs and principles, there is a genuine need for an interest-free alternative to the current UPS structure. The participation of devout Muslims in a scheme that involves riba would be in conflict with their religious values. To ensure the inclusivity of the scheme and cater to the religious sensitivities of the population, an interest-free alternative is essential.

3. Islamic Banking Preference: Bangladesh has witnessed the rise of Islamic banking and finance due to the strong preference of many Muslims to avoid engaging in usurious activities. Islamic banks in the country have attracted a substantial customer base, reflecting the demand for financial products and services that adhere to Islamic principles. This trend underscores the importance of considering the religious preferences of citizens when designing financial schemes such as the UPS.

4. Ensuring Universality: The concept of universality implies that a scheme should be accessible and applicable to a wide range of individuals, regardless of their backgrounds or beliefs. The current structure of the UPS, which raises concerns of riba, might hinder the participation of a significant segment of the population. If a substantial portion of the population refrains from participating due to religious reasons, the scheme might not achieve its intended universal coverage.

5. Seeking Guidance from Ulama: To address these religious challenges, it’s crucial for the government to seek guidance from learned ulama (Islamic scholars) who specialize in Islamic finance and jurisprudence. These scholars can provide insights and recommendations on how to structure an interest-free pension scheme that aligns with Islamic principles while still achieving the goals of the UPS. Their input would be essential in ensuring that the scheme is widely accepted and embraced by the population.

6. Importance of Inclusivity: The success of any pension scheme, including the UPS, lies in its ability to encompass a broad spectrum of participants. By offering an interest-free alternative, the government can ensure that the scheme truly reflects the aspirations and values of the majority of the population. This inclusivity not only respects religious beliefs but also strengthens the overall participation and effectiveness of the scheme.

So, while the introduction of the Universal Pension Scheme in Bangladesh is indeed a commendable initiative, it’s important to acknowledge and address the religious challenges posed by the current structure. By designing an interest-free alternative that adheres to Islamic principles and seeking guidance from Islamic scholars, the government can create a more inclusive and universally accepted pension scheme that caters to the diverse beliefs of the population.

Addressing these institutional and governance challenges will require a comprehensive strategy that involves collaboration between government bodies, financial institutions, technology experts, and civil society organizations. Learning from both domestic and international best practices can guide the development of effective solutions tailored to Bangladesh’s unique context. By addressing these challenges head-on, Bangladesh can establish a robust and well-governed Universal Pension Scheme that ensures the financial security and dignity of its aging population.

Conclusion

Implementing the Universal Pension Scheme (UPS) in Bangladesh presents multifaceted challenges that require careful consideration and comprehensive planning. From ensuring proper registration and trust-building among beneficiaries to addressing issues related to institutional governance and efficient fund management, each challenge requires a tailored approach. Successful implementation hinges on a collaborative effort between various stakeholders, the integration of reform initiatives, and a proactive approach to address the unique demographics and cultural context of Bangladesh. By taking these challenges into account, policymakers and relevant authorities can pave the way for a more secure and dignified retirement for the country’s senior citizens.

The recent announcement of the Universal Pension Scheme (UPS) by the Bangladeshi government marks a crucial step towards supporting the elderly population. As the country’s average life expectancy rises to 73 years, the need for an old-age support system becomes increasingly urgent. The implementation of the UPS on August 17, 2023, is promising, but its success hinges on addressing several key factors. Let’s explore how to make the UPS successful in Bangladesh.

How to make the UPS successful?

Introducing the Universal Pension Scheme (UPS) in Bangladesh holds great promise to support the growing elderly population. To ensure its success, a strategic approach is crucial, involving careful considerations such as fiscal sustainability, transparent governance, robust institutional frameworks, and effective fund management.

1. Addressing Financial Constraints: Implementing the Universal Pension Scheme (UPS) faces the challenge of balancing increased government expenditure with limited fiscal space. The government needs to allocate funds for the scheme while managing other financial commitments, including infrastructure projects. A clear plan for funding the UPS, especially in the context of low revenue collection, is essential.

2. Ensuring Accountability and Good Governance: Considering instances of mismanagement in social safety net programs, accountability and good governance are critical. Transparent mechanisms should be put in place to prevent misappropriation of resources. Rigorous oversight and monitoring mechanisms are needed to ensure that the funds are used for their intended purpose and reach the intended beneficiaries.

3. Designing a Robust Institutional Framework: Creating a strong institutional and legal framework for the UPS is crucial. Defining the authority and responsibilities of the pension scheme, as well as the operational modalities, is essential for smooth functioning. Establishing a dedicated authority to manage the scheme and ensuring the quality of services provided to beneficiaries are important aspects to consider.

4. Effective Fund Management: Proper management of the pension fund is a critical factor in the success of the UPS. Learning from successful models in other countries, the fund should be invested in profitable ventures to generate income. However, this requires addressing governance-related challenges within Bangladesh’s banking sector. Institutional reforms and a transparent investment strategy are necessary to ensure a steady income stream for pensioners.

5. Prioritizing Transparency: Transparency is key to gaining public trust and confidence in the UPS. Clear communication about fund investment, profit distribution, operational costs, and updates should be provided to beneficiaries. Implementing a robust supervision and monitoring system will help prevent wastage and ensure the scheme’s integrity. The use of automated systems can enhance transparency and accessibility for pension account holders.

6. Inclusive Beneficiary Identification: Creating a comprehensive and accurate database of eligible beneficiaries is essential. To avoid exclusion and ensure equity, the process of identifying and enrolling pensioners should be transparent, fair, and well-documented. Engaging local communities and civil society organizations can help verify and validate beneficiary information.

7. Adequate Investment Diversification: Diversifying the investment portfolio of the pension fund is crucial to mitigate risks and enhance returns. Instead of relying solely on one type of investment, such as banking, the fund could explore opportunities in various sectors, including stocks, bonds, and real estate. This approach can contribute to sustained growth and stable income for pensioners.

8. Education and Outreach: Creating awareness among the population about the UPS and its benefits is vital. Educational campaigns, workshops, and information sessions can help citizens understand how the scheme works, the importance of contributing, and the long-term benefits. This outreach can promote voluntary participation and debunk misconceptions.

9. Technological Integration: Leveraging technology can streamline administrative processes and enhance the scheme’s efficiency. Developing user-friendly digital platforms for registration, contribution tracking, and benefit disbursement can simplify operations and reduce administrative overhead. Ensuring the security of digital systems and providing training for users is essential.

10. Continuous Review and Adaptation: The UPS should not remain static but evolve over time based on changing demographics, economic conditions, and societal needs. Regular evaluations and adjustments to the scheme’s parameters, investment strategies, and operational procedures are necessary to ensure its relevance and effectiveness in the long run.

Conclusion,

The introduction of the Universal Pension Scheme aligns with Bangladesh’s aspirations for socio-economic growth. However, its success depends on meticulous planning and execution. By addressing fiscal challenges, establishing transparent governance practices, designing a robust institutional framework, ensuring effective fund management, learning from global best practices, and embracing technological integration, Bangladesh can create a pension system that supports its aging population while upholding principles of transparency, accountability, and efficiency. The success of the UPS will not only contribute to the welfare of senior citizens but also serve as a milestone on the path toward national development goals.

In a historic move aimed at providing financial security and social protection to a significant portion of the population, It is the launching of the universal pension scheme in Bangladesh today. This groundbreaking initiative, spearheaded by the government, aims to encompass approximately 10 crore people from various socio-economic backgrounds. The pension scheme is poised to address the needs of the elderly and those engaged in low-income and informal sectors, marking a significant step towards ensuring the well-being of the nation’s citizens.

The journey towards implementing the universal pension system began with the initiation of the late Finance Minister Abul Mal Abdul Muhith in 2015. A concept paper was developed in 2016, and after a hiatus, the concept gained momentum in 2022. On January 31 of the current year, the National Pension Authority was established under the Universal Pension Management Act. Here’s a comprehensive overview of this innovative pension system.

The Need for a Universal Pension System

In the face of significant demographic shifts and an aging population, the imperative for a comprehensive social security framework has never been more evident. Bangladesh, like many countries, is witnessing a transformation in its population structure, which underscores the necessity of introducing a robust universal pension system. This imperative arises from the increasing number of elderly citizens and the government’s commitment to ensuring the welfare of its people.

Demographic Changes and Aging Population

Over the past few decades, Bangladesh has experienced notable demographic changes characterized by a growing proportion of elderly individuals. The Finance Department of the Ministry of Finance has meticulously studied this trend and predicts a substantial increase in the elderly population over the upcoming years. In 2020, the elderly population stood at 1 crore 2 million, and this number is projected to swell to a staggering 3 crore 10 million by the year 2041. This remarkable demographic shift reflects longer life expectancies and changes in birth rates, creating a scenario where a significant portion of the population is entering their senior years.

Challenges and Vulnerabilities

As the aging population expands, a host of challenges and vulnerabilities emerge. Elderly citizens often face financial instability due to reduced earning capacity after retirement. Moreover, many individuals are engaged in low-income and informal sectors, where traditional pension options are often unavailable. The lack of a sustainable social security framework can lead to economic hardships for seniors who lack reliable financial support during their retirement years.

Empowering the Informal Sector

Recognizing the demographic changes and the prevalence of low-income and informal sectors, the government acknowledges the need to provide a safety net for its citizens. Many individuals engaged in rickshaw pulling, farming, labor, artisanal work, fishing, weaving, and other informal professions often lack access to pension plans through traditional employment channels. Addressing the financial insecurities faced by these individuals is central to the goal of promoting economic well-being across all segments of society.

Sustainable and Organized Pension System

In response to these challenges, the government is introducing a universal pension system. This innovative system aims to create a sustainable and organized framework that caters to the needs of citizens from all walks of life, particularly those engaged in informal and low-income sectors. By offering a comprehensive pension scheme, the government seeks to ensure that elderly individuals can retire with dignity, financial security, and the peace of mind that comes from having a dependable support system in place.

The introduction of a universal pension system in Bangladesh signifies the government’s commitment to address the evolving needs of its citizens in the face of demographic changes. This forward-looking initiative aims to provide a safety net for individuals engaged in informal sectors and low-income professions, empowering them to enjoy a secure and comfortable retirement. By acknowledging the challenges posed by an aging population and implementing a comprehensive pension system, Bangladesh takes a significant step towards promoting social security, economic stability, and a better quality of life for all its citizens.

Background and History of UPS in Bangladesh

The journey towards implementing the Universal Pension Scheme (UPS) in Bangladesh is rooted in the commitment made by the government back in 2008. This commitment was an integral part of the government’s broader vision for social security and elderly welfare. Over the years, the concept of the UPS has evolved to address the challenges posed by a growing elderly population and the need for a well-organized and sustainable social security framework.

2008: The Commitment and Aspiration

In 2008, during the general elections, the ruling party articulated its commitment to introduce a universal pension scheme as part of its election manifesto. This marked the first significant step towards recognizing the importance of providing support to the senior citizens of the country. The commitment was made in the backdrop of Bangladesh’s evolving socio-economic landscape, characterized by an increasing average life expectancy and a demographic shift.

Initiation of the Implementation Process

The initiative to implement the UPS gained renewed momentum in the subsequent years, as the government recognized the pressing need to address the insecurities faced by the elderly population. While the initial discussions took place in 2015, under the leadership of the late Finance Minister Abul Mal Abdul Muhith, it was during this period that the foundations of the UPS were laid. A team from the Finance Department’s visit to India in 2016 resulted in the development of a concept paper that envisioned a comprehensive pension system.

2022 and Beyond: Reviving the Vision

The concept of the UPS resurfaced with greater urgency in 2022, reflecting the growing concerns surrounding the elderly population’s financial security. A new concept paper was drafted by the Finance Department, highlighting the importance of creating an integrated, participatory, and well-structured pension system to protect citizens during their old age.

Formation of the National Pension Authority

A crucial milestone was reached when, on January 31, 2023, the National Pension Authority was established under the Universal Pension Management Act. This institutional framework laid the groundwork for the implementation of the pension system, streamlining management and administration.

Budget Speach (2023): In the budget speech of the current financial year, the Finance Minister reiterated the government’s commitment to introducing a universal pension system. This underscored the alignment of the pension scheme with the government’s broader social security goals.

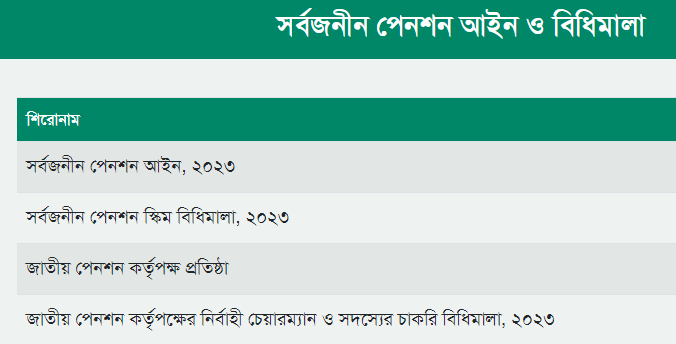

Four Schemes for Diverse Needs

The UPS was thoughtfully designed to cater to the diverse needs of different segments of the population. The migration, progress, protection, and equality schemes were crafted to ensure that various occupational categories and income groups could access the benefits of the pension system.

Website Launch and Registration (2023): The National Pension Authority’s website, www.upension.gov.bd, was launched to facilitate the registration process for the UPS. This online platform serves as the gateway for individuals to enroll in the pension scheme.

Implementation and Looking Ahead

August 17, 2023, is a gigantic day for the people of Bangladesh as UPS starts its implementation journey. The journey towards implementing the UPS in Bangladesh is a testament to the government’s commitment to the welfare of its citizens, particularly the elderly population. The initial promise made in 2008 set the stage for the subsequent evolution of the concept and the creation of an institutional framework. As the scheme takes effect, its success will be measured by its ability to provide financial security to the elderly, realizing the aspiration that was set forth in the government’s commitment more than a decade ago.

Universal Pension System Inauguration

In a momentous and visionary step towards ensuring a better life for every citizen, Prime Minister Sheikh Hasina inaugurated Bangladesh’s Universal Pension System through a virtual link from her official residence, Ganabhaban, on Thursday, August 17th, 2023. With the aim of uplifting the lives of citizens above 18 years of age, the inauguration marked a significant milestone in the country’s commitment to social welfare and inclusive development.

Prime Minister Sheikh Hasina articulated the significance of the universal pension system as a means to uplift the quality of life for every individual across the nation. As she inaugurated the system, she underlined the government’s dedication to creating an environment where all citizens could thrive and prosper. The visionary essence of the initiative lay in its ambition to encompass every individual within its protective embrace.

With unwavering determination, the Prime Minister announced the launch of four out of the six schemes that constitute the universal pension system: Pragati, Sukhara, Samata, and Pravasi. These initial schemes symbolized the government’s dedication to taking incremental steps towards a comprehensive and all-encompassing system of financial support for citizens. The remaining two schemes are set to be introduced at a later stage, underlining the commitment to phased implementation.

Prime Minister Sheikh Hasina’s words echoed the legacy of the Father of the Nation, Bangabandhu Sheikh Mujibur Rahman, whose lifelong dedication was focused on ensuring a better life for every citizen. The universal pension system’s launch during a month of mourning added a layer of reverence and dedication to the program. In invoking the memory of Bangabandhu Sheikh Mujibur Rahman and Mother Banga, the Prime Minister emphasized that their visionary spirits would find solace in witnessing the government’s efforts to uplift the lives of the people.

Acknowledging the uniqueness of the occasion, the Prime Minister expressed her intention to establish the pension scheme exclusively during her party’s rule. This exclusivity was born from a genuine concern that future administrations might not undertake such a monumental program. The Prime Minister’s foresight underlined her understanding of the transformational impact that the universal pension system could bring to the lives of citizens.

The inaugural program was not confined to national boundaries; it transcended geographical distances to connect with local public representatives, beneficiaries from districts including Gopalganj, Bagerhat, and Rangpur, and the Consulate General of Bangladesh in Jeddah, Saudi Arabia. Through a video conference, these stakeholders joined hands to celebrate the launch of a program that symbolized hope, inclusivity, and progress.

The occasion was graced by key figures instrumental in the formulation and execution of the universal pension system. Finance Minister AHM Mustafa Kamal and Bangladesh Bank Governor Abdur Rauf Talukdar shared their perspectives, underlining the economic and financial dimensions of the initiative. Senior Secretary of the Finance Division, MoF, contributed her insights, adding a versatile perspective to the event.

The launch event was skillfully moderated by Tofazzel Hossain Mia, underscoring the importance of effective facilitation in realizing such transformative initiatives. A pivotal moment during the program was the screening of a video documentary on the Universal Pension System. This documentary encapsulated the system’s essence, goals, and journey that led to its inauguration, providing attendees with a comprehensive overview of the initiative.

Prime Minister Sheikh Hasina, in her closing remarks, expressed profound gratitude to all stakeholders who contributed to the inception of the universal pension system. She singled out former Finance Minister Abul Mal Abdul Muhith and the current Finance Minister for their relentless efforts in making this vision a reality. Their dedication and commitment were essential pillars in the foundation of a program that aspires to touch the lives of millions, uplift communities, and steer the nation towards a brighter and more prosperous future.

Inaugurating the universal pension system was not just a symbolic gesture; it was a declaration of the government’s unyielding dedication to the welfare of its citizens. It was a step forward in building a society that values and safeguards the well-being of its members, ensuring that every individual, regardless of age, socio-economic background, or location, has the opportunity to lead a life of dignity and security.

What are the Four Pension Schemes

Bangladesh’s Universal Pension System is a government-run pension scheme that is open to all citizens of Bangladesh, regardless of their employment status or income level.

The scheme offers four different packages, each with its own monthly contribution and pension benefits tailored to address the diverse needs of different groups:. The packages are:

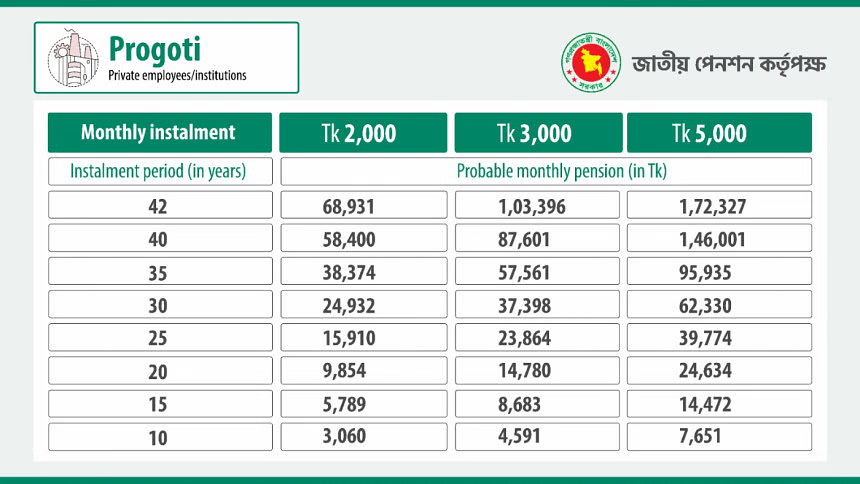

Progoti: This package is for private sector employees and offers a monthly pension of Tk 2,000, Tk 3,000, or Tk 5,000, depending on the monthly contribution.

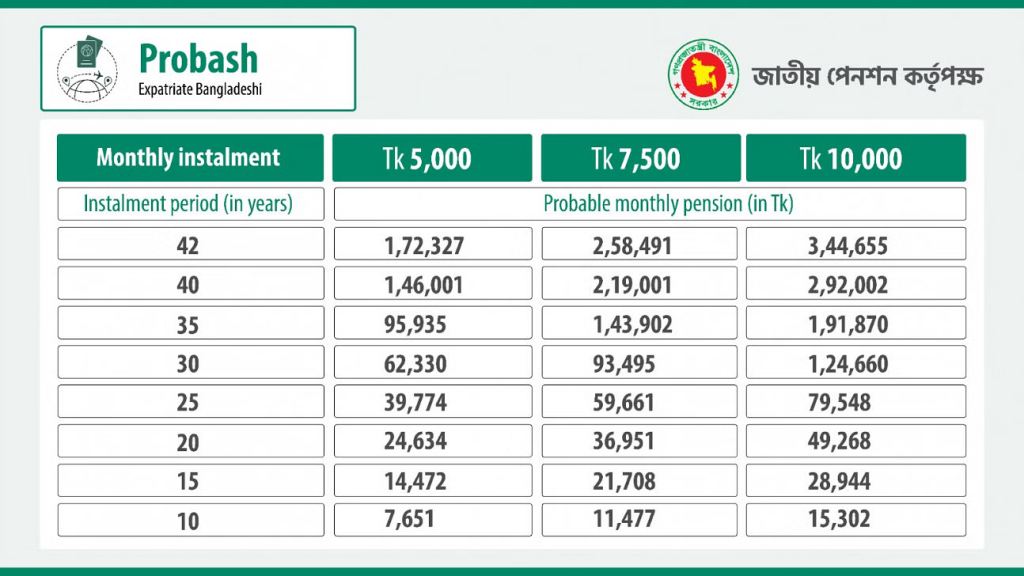

Probash: This package is for expatriate Bangladeshis and offers a monthly pension of Tk 5,000, Tk 7,500, or Tk 10,000, depending on the monthly contribution.

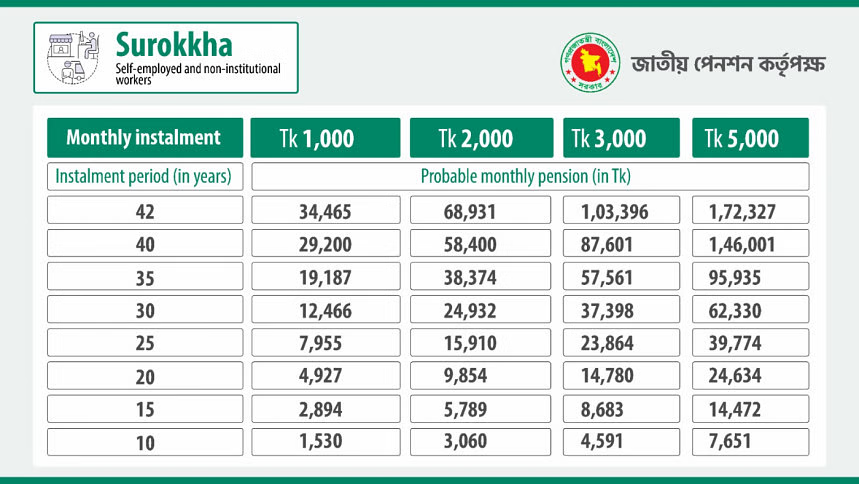

Shurokkha: This package is for the self-employed and informal sector workers and offers a monthly pension of Tk 1,000, Tk 2,000, Tk 3,000, or Tk 5,000, depending on the monthly contribution.

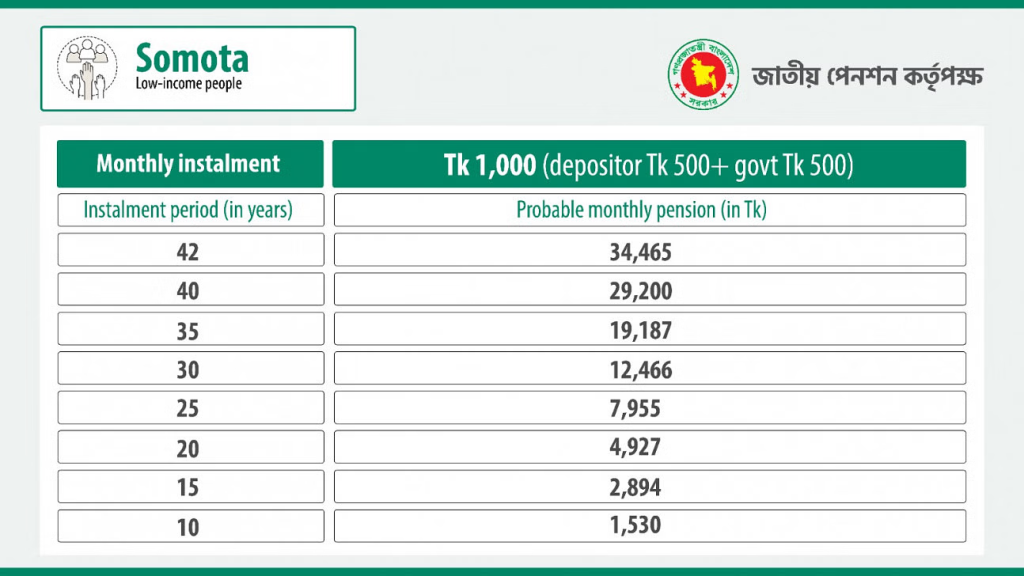

Samata: This package is for the ultra-poor and offers a monthly pension of Tk 1,000, with the government contributing Tk 500 and the beneficiary contributing Tk 500.

Administration and Implementation

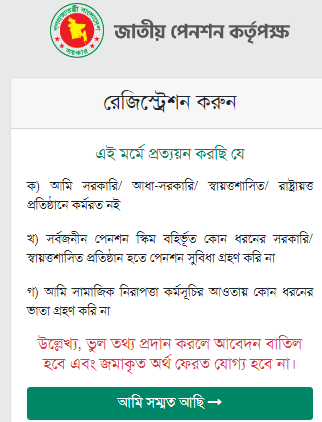

The National Pension Authority, operating under the Finance Department, is responsible for managing and implementing the pension system. The authority’s official website, www.upension.gov.bd, was launched to provide essential information and facilitate the registration process for interested individuals. The legal aspects include the following:

Eligibility and Registration

To be eligible for the universal pension system, individuals must be above the age of 18 and not employed by the government. National Identity Card (NID) holders can register directly, while expatriates lacking an NID can register using their passport information. The registration process involves selecting one of the four schemes and providing personal, professional, and banking details.

Pension Features

The Universal Pension Scheme (UPS) in Bangladesh has been meticulously designed to address the financial security needs of its citizens, particularly those in their old age. This innovative scheme is characterized by several key features that ensure inclusivity, flexibility, and long-term stability:

1. Inclusive Age Range: The UPS opens its doors to all Bangladeshi citizens aged between 18 and 50 years. This wide age range reflects the government’s commitment to provide pension coverage to a significant portion of the population and cater to individuals at various stages of their lives.

2. Flexibility for Citizens above 50: While the standard eligibility range is between 18 and 50 years, the UPS also accommodates citizens above the age of 50 under special consideration. These individuals can participate in the scheme and, upon meeting certain conditions, receive a lifetime pension. This provision acknowledges the diversity of situations and ensures a safety net for those entering the scheme later in life.

3. Inclusion of Expatriate Workers: The UPS goes beyond national borders by allowing Bangladeshi workers employed abroad to be included in the program. This recognition of the contributions made by expatriates highlights the government’s commitment to protecting the interests of its citizens regardless of their geographic location.

4. Individual Pension Accounts: Each participant in the UPS is allocated a distinct and separate pension account. This individualized approach ensures transparency and accountability, allowing contributors to keep track of their pension contributions and the growth of their funds over time.

5. Survivor Benefits: The UPS addresses the uncertainty of life by offering survivor benefits. In the unfortunate event of a contributor’s passing before reaching 75 years of age, the nominee of the pensioner is entitled to receive a monthly pension for the remaining period up to the age of 75. This provision assures the well-being of the pensioner’s dependents.

6. Refund Option: To account for unforeseen circumstances, the scheme provides a safeguard for contributors. If a subscriber passes away at least 10 years before the completion of their subscription period, the deposited money will be returned to their nominee along with accrued profits. This feature guarantees that the funds invested in the scheme do not go to waste.

7. Tax Benefits: The UPS acknowledges the financial realities of its participants by considering the fixed pension contribution as an investment. This not only encourages savings but also offers potential tax deductions, providing an added incentive for individuals to engage with the scheme. Moreover, the monthly pension received from the scheme is exempt from income tax, ensuring that the pensioners can fully benefit from their contributions during retirement.

In essence, the Universal Pension Scheme exemplifies the government’s dedication to securing the financial well-being of its citizens throughout their lives. By offering comprehensive coverage, flexibility, and beneficial features, the scheme contributes to the larger goal of ensuring social welfare and protection for all members of society.

The registration process for the UPS involves multiple steps to ensure accurate and comprehensive enrollment:

Agreement to Eligibility Criteria: The first step requires applicants to certify that they are not employed by any government, semi-government, autonomous, or non-government organization. They must confirm that they are not receiving benefits from any sources other than the public pension scheme or social security program.

Scheme Selection: Applicants then proceed to select the appropriate scheme among the four options: Immigration, Equality, Protection, or Progression. This step allows individuals to choose the scheme that aligns with their occupational category and needs.

Personal Information: The applicant’s National Identity Card (NID) number, photo, Bengali and English names, parent’s names, current and permanent addresses are automatically populated based on the NID provided.

Occupation and Income Details: Applicants enter their annual income and select their occupation from a list of options, including teachers, private employees, small traders, laborers, professionals, and more.

Bank Account Information: Individuals provide their bank account details, including the account number, type (savings or current), routing number, bank name, and branch name. This information ensures the proper deposit of contributions and pension disbursements.

Nominee Information: Applicants enter the nominee’s National Identity Card number, date of birth, mobile number, and relationship with the nominee. In case of multiple nominees, the availability rate is also specified.

Confirmation and Submission: The final step involves reviewing all provided information. If accurate, applicants agree to the terms and conditions and submit the application. The option to download the completed application is also provided.

FAQs for Universal Pension Scheme in Bangladesh

What is the Universal Pension Scheme (UPS)?

Answer: The Universal Pension Scheme is a pioneering initiative launched by the government of Bangladesh to provide financial security and social protection to citizens, aiming to encompass around 10 crore people from diverse socio-economic backgrounds.

What is the main goal of the UPS?

Answer: The main goal of the Universal Pension Scheme is to ensure the well-being of citizens, particularly the elderly and those engaged in low-income and informal sectors, by offering a sustainable and organized pension framework.

How did the journey towards implementing the UPS begin?

Answer: The journey began with the commitment of the government in 2008, and over time, it evolved into an inclusive and comprehensive system to address the challenges posed by an aging population and the need for social security.

What are the four pension schemes under the UPS?

Answer: The four pension schemes are Progoti, Probash, Shurokkha, and Samata. Each scheme is tailored to cater to different categories of individuals, such as private sector employees, expatriate Bangladeshis, self-employed individuals, informal sector workers, and the ultra-poor.

Who is responsible for the management and implementation of the UPS?

Answer: The National Pension Authority is responsible for managing and implementing the Universal Pension Scheme.

What is the eligibility criterion for joining the UPS?

Answer: Individuals above the age of 18 who are not employed by the government are eligible to join the UPS. Both National Identity Card (NID) holders and expatriates can register.

What benefits does the UPS offer to individuals above the age of 50?

Answer: While the standard eligibility range is 18 to 50 years, citizens above the age of 50 can also participate under special consideration and receive a lifetime pension upon meeting certain conditions.

How is the UPS designed to support expatriate workers?

Answer: The UPS allows Bangladeshi workers employed abroad to enroll, ensuring that citizens regardless of their geographic location can benefit from the pension scheme.

What is the registration process for the UPS?

Answer: The registration process involves confirming eligibility criteria, selecting a scheme, providing personal and occupation details, bank account information, and nominating beneficiaries.

What are the key features of the UPS that ensure inclusivity and flexibility?

Answer: The UPS offers an inclusive age range, flexibility for citizens above 50, inclusion of expatriate workers, individual pension accounts, survivor benefits, a refund option, and potential tax benefits to encourage savings and ensure financial security during retirement.

Conclusion

Bangladesh’s universal pension system marks a significant milestone in the country’s efforts to provide comprehensive social security and financial stability to its citizens. With distinct schemes catering to different segments of the population and a streamlined registration process, this initiative holds the potential to positively impact the lives of millions, fostering a more secure and prosperous future for all. The launch of this system underscores the government’s commitment to creating an inclusive and resilient social security framework, setting the stage for enhanced quality of life and dignified retirement for its citizens.

Robo-advisors make money through fees charged for their services, such as management fees and account maintenance fees. These fees are typically based on a percentage of the assets under management (aum) or a flat fee per account.

Additionally, some robo-advisors may generate revenue through interest earned on cash holdings or by offering premium services with higher fees. With their automated and efficient approach to investing, robo-advisors have gained popularity among investors looking for low-cost and accessible investment options.

But how do these digital platforms actually make money? Let’s delve deeper into the revenue model of robo-advisors and explore the various ways they generate income.

Credit: moneywise.com

The Basics Of Robo-Advisors

Robo-advisors have become increasingly popular in recent years due to their innovative approach to investing. These automated platforms provide investors with a variety of services and charge fees for their services. The basics of robo-advisors involve utilizing algorithms and digital technology to create and manage investment portfolios.

This eliminates the need for human financial advisors and reduces costs for investors. Robo-advisors typically generate revenue through a combination of management fees, account fees, and potentially by lending out customer funds. They offer several advantages, including lower fees compared to traditional advisors, accessibility to a wider range of investors, and automated asset allocation based on individual risk preferences.

Additionally, robo-advisors use advanced algorithms to monitor and rebalance portfolios, ensuring they remain aligned with the investor’s goals. Overall, robo-advisors provide a convenient and cost-effective way for individuals to invest their money in the stock market.

How Do Robo-Advisors Work?

Robo-advisors make money through various means. They work by utilizing algorithmic strategies to create investment portfolios. These portfolios are designed based on factors such as risk tolerance, investment goals, and time horizon. The algorithm considers these factors and creates a diversified portfolio tailored to each individual investor.

Robo-advisors also make use of technology in their operations and decision-making processes. Technology helps them automate tasks like rebalancing portfolios and tax-loss harvesting. It also enables them to provide real-time updates and personalized recommendations to investors. By charging a management fee or a percentage of the assets under management, robo-advisors generate revenue.

This fee structure ensures that they are compensated for their services and can continue to provide automated investment management to a broad range of investors. So, in summary, robo-advisors work by employing algorithmic strategies, considering various factors, leveraging technology, and charging fees for their services.

https://www.youtube.com/watch?v=n66k-NL6_I8

Revenue Models Of Robo-Advisors

Robo-advisors generate revenue through various methods. One primary way is by charging fees for their services. These fees can be categorized into management, advisory, and additional fees. Management fees are generally a percentage of the total assets under management, while advisory fees are charged for specific advice or portfolio management.

In addition to these fees, robo-advisors may offer different account structures, like freemium and premium accounts, with varying features and costs. This helps them cater to different types of investors. Robo-advisors can also explore potential additional revenue streams, like referral fees and partnerships.

These partnerships could be with other financial institutions or service providers. By diversifying their revenue sources, robo-advisors can ensure profitability and sustainability in the long run.

Key Factors Affecting Robo-Advisor Profitability

Robo-advisors make money primarily by increasing their assets under management (aum). A larger aum allows them to generate more revenue. The competition among robo-advisors also plays a crucial role in their profitability. Differentiation and market positioning are key factors in gaining an edge over competitors.

To stay ahead, robo-advisors need to adopt trends and advancements in technology, which can impact their cost structure. By leveraging technology effectively, they can optimize their operations and offer competitive pricing to clients. Overall, increasing aum, competition, and technological advancements are the key factors influencing the profitability of robo-advisors.

Regulatory Considerations For Robo-Advisors

Robo-advisors generate revenue through various channels. In each jurisdiction, they must adhere to specific regulatory requirements to operate legally. These regulations aim to protect investors and maintain the integrity of the financial industry. Compliance costs can impact the profitability of robo-advisor firms, but they are a necessary investment to maintain trust and credibility.

Adhering to a rapidly changing regulatory landscape presents challenges and potential risks. Robo-advisors must adapt to new regulations and ensure their technology and operations remain compliant. Failure to do so could result in penalties or loss of customers’ trust. Thus, it is crucial for robo-advisors to stay updated on the regulatory requirements of the jurisdictions they operate in.

By doing so, they can continue to serve investors effectively and profitably while navigating the complexities of regulatory compliance.

Comparison With Traditional Financial Advisors

Robo-advisors and traditional financial advisors differ in their fee structures and levels of personalization. Robo-advisors, being technology-driven, often have lower fees compared to human advisors. However, the personalized approach of a human advisor can be more advantageous in certain situations.

Robo-advisors are disrupting the financial advisory industry by providing accessible and affordable investment options. Their automated platforms allow easy portfolio management for investors, reshaping the traditional advisory model. Despite their advantages, robo-advisors also have some drawbacks. They lack the ability to understand complex financial situations and provide personalized advice tailored to individual needs.

Human advisors, on the other hand, offer expertise, emotional support, and a deeper understanding of a client’s unique circumstances. As the financial industry evolves, a combination of robo-advisors and human advisors may be the optimal solution for investors seeking a balance between cost-efficiency and personalized guidance.

Strategies For Robo-Advisors To Enhance Revenue Generation

Robo-advisors drive revenue by exploring diversification into additional financial services and products. They extend upselling and cross-selling opportunities to their existing customers. Leveraging data analytics, they make personalized recommendations to enhance customer engagement and retention. These strategies ensure a steady stream of income for robo-advisors.

By expanding their offerings and tailoring investment advice, they attract more clients and generate higher profits. With their advanced technology and low-cost investment options, robo-advisors have redefined the wealth management industry. They provide accessible and automated financial services, making investing easier and more affordable for the masses.

Through continuous innovation and customer-centric strategies, robo-advisors continue to disrupt the traditional financial advisory space. As the industry evolves, robo-advisors adapt and thrive, making money while democratizing finance for all.

Frequently Asked Questions On How Do Robo-Advisors Make Money?

How Do Robo-Advisors Make Money?

Robo-advisors make money through fees charged for managing investment portfolios. They typically charge a percentage of assets under management, usually between 0. 25% to 0. 50%. Some robo-advisors also earn money through partnerships with financial institutions or by offering additional premium services for a fee.

Are Robo-Advisors Reliable?

Robo-advisors have gained credibility over the years and are considered reliable. They use algorithms to build and manage investment portfolios, which are based on data analysis and market trends. However, it is always recommended to research the reputation and track record of a robo-advisor before investing.

What Are The Benefits Of Using Robo-Advisors?

Robo-advisors offer several benefits, including lower fees compared to traditional financial advisors, convenience, ease of use, and automated portfolio rebalancing. They also provide access to diversified investment options and personalized advice based on an individual’s financial goals and risk tolerance.

Can I Trust Robo-Advisors With My Money?

Robo-advisors use automated algorithms and data analysis to make investment decisions, which are based on proven investment strategies. While there is always a level of risk involved in any investment, many people trust robo-advisors with their money due to their transparent and systematic approach to investing.

How Do Robo-Advisors Choose Investments?

Robo-advisors use a combination of proprietary algorithms and data analysis to choose investments for their clients. They consider various factors such as an individual’s financial goals, risk tolerance, time horizon, and market trends to build a diversified portfolio of low-cost etfs (exchange traded funds) or index funds.

Are Robo-Advisors Suitable For Beginners?

Yes, robo-advisors are suitable for beginners as they provide a user-friendly and simplified investing experience. They offer guidance in setting up personal financial goals and automatically allocate investments based on risk tolerance. Additionally, robo-advisors provide educational resources and customer support to help beginners navigate the investing world.

Conclusion

Robo-advisors have revolutionized the investment landscape by offering low-cost and accessible financial services to individuals. By leveraging sophisticated algorithms and automation, these platforms have streamlined the investment process, making it more efficient and convenient for users. But how do robo-advisors make money?

The primary revenue generation model for robo-advisors is through management fees charged to clients based on their invested assets. While the fees may vary from platform to platform, they are typically lower compared to traditional investment advisors. Additionally, some robo-advisors may also generate revenue through referral fees or partnerships with financial institutions.

However, it is important for investors to carefully evaluate the fee structure and understand the potential trade-offs between cost and services offered. As the demand for robo-advisory services continues to grow, it is expected that these platforms will further innovate and offer additional value-added services to diversify their revenue streams and enhance the overall user experience.

Investors should keep a close eye on this rapidly evolving industry and stay informed to make the most of the opportunities presented by robo-advisors.