In the dynamic world of business, expenses are not always visible on balance sheets. While many entrepreneurs focus on traditional costs like marketing, production, and employee salaries, there is a silent and often underestimated expense wreaking havoc on businesses: the invisible cost of ignorance. This hidden cost, often overlooked, plays a significant role in hindering real profit and success. This article sheds light on The Invisible Debt That Turns Businesses Bankrupt.

Unmasking the Invisible Cost

Consider for a moment, what truly constitutes the most substantial cost in a business? Some argue it’s marketing, others point to production expenses, and some may highlight employee costs. However, beyond these, there exists an invisible cost that, if left unaddressed, can lead businesses down the path of bankruptcy: the cost of ignorance.

The invisible expense in business is the lack of knowledge on how to scale and multiply income. In simpler terms, it’s an “ignorance debt” that many entrepreneurs accumulate without realizing its impact on their bottom line.

Debt That Turns Businesses Bankrupt

Ignorance debt is the gap between your expected income and your current income. It represents the cost incurred due to not knowing how to make your business scalable and profitable. The concept is rooted in the idea that learning in business comes with a cost, and the cost of ignorance remains hidden, making it harder to identify and rectify.

Let’s break it down using a hypothetical scenario:

Ignorance Debt = (Your Expected Income – Your Current Income)

For instance, if your business is anticipated to make a profit of Rs 5 lakh per month, but you’re currently generating only 2 lakh rupees, you are essentially incurring an invisible expense or an ignorance debt of 3 lakh rupees every month. This debt persists until you develop the necessary skills to bridge the gap and reach your expected income.

The Solution: Skill Development and Guidance

The most straightforward way to eradicate ignorance debt is to seek guidance from someone who has already achieved success in your desired field. Learning from those who have already walked the path helps you acquire the skills needed to grow and make informed decisions. As Eric Partaker puts it, “Everything you need to know is already in someone’s head. Your job is to get that knowledge out of someone’s head.”

Remember, your business is a reflection of you, and many business and financial problems are, in reality, personal skill problems in disguise. The solution lies in recognizing your weaknesses and actively working on developing the necessary skills.

The Cost of Ignorance vs. Enlightenment

Ignorance often costs more than enlightenment, yet this reality often goes unnoticed. To address the income problem in your business, it’s crucial to acknowledge and tackle the underlying skill problem. Whether it’s improving sales, product quality, team management, or leadership, the key is to identify weaknesses and actively develop the corresponding skills.

A participant in a business management course highlighted the impact of ignorance debt, stating, “I would not have understood that my ignorance debt is such a large number if I had not joined Brave Program. In fact, my business does not see the face of profit because of my mistake.”

In such programs, skills and strategies are shared to help businesses grow tenfold in a year, emphasizing that the solution to ignorance debt lies in continuous learning and skill development.

Overcoming Ignorance Debt: A Journey to Business Mastery

The Skill Dilemma: Your Business Reflects You

It’s a common adage that your business is a reflection of you. Often, business and financial challenges are intertwined with personal skill gaps. Recognizing this connection is pivotal. If sales are lagging, it’s not just an income problem; it’s a skill problem in sales. If your product quality is underwhelming, it’s a skill problem in product development. The essence lies in pinpointing these skill deficiencies and actively working towards honing them.

Bridging the Gap: The Power of Skill Development

Addressing ignorance debt requires a proactive approach to skill development. Rather than viewing business challenges as insurmountable obstacles, entrepreneurs should see them as opportunities to learn and grow. Embracing a mindset that values continuous improvement is key to overcoming ignorance debt. This involves seeking out the necessary knowledge and skills to bridge the gap between current and expected income.

Seeking Guidance: Learning from the Masters

As the saying goes, “If you’re the smartest person in the room, you’re in the wrong room.” Seeking guidance from those who have already achieved success is a game-changer. Mentorship and coaching programs, such as the ‘Brave’ program offered by Coach Kanchan Academy, provide entrepreneurs with the insights and strategies needed to catapult their businesses to new heights. Learning from those who have navigated the intricacies of entrepreneurship can significantly accelerate the journey to success.

Skill Debt in Action: A Practical Example

Consider a scenario where an entrepreneur anticipates a monthly profit of BDT 5 lakh but is currently generating only 2 lakh rupees. The difference of 3 lakh rupees represents the ignorance debt – the cost incurred due to a lack of skills and knowledge. This debt persists until the entrepreneur actively invests in skill development to achieve the expected income. It’s not merely a financial gap; it’s a skills gap that needs to be addressed.

Enlightenment vs. Ignorance: The True Cost

The cost of ignorance often goes unnoticed because it’s not a line item on a financial statement. Yet, it’s one of the most significant costs a business can incur. The value of education and skill development cannot be overstated. Ignorance may seem cost-free, but the price is paid in missed opportunities, stalled growth, and unrealized potential. Enlightenment, on the other hand, is an investment that pays dividends in the form of increased competency, strategic decision-making, and sustained success.

The Journey to Mastery: A Continuous Cycle

Overcoming ignorance debt is not a one-time fix but a continuous cycle of learning, adapting, and applying newfound knowledge. It involves a commitment to personal and professional development, a willingness to embrace challenges as opportunities, and a recognition that mastery is an ongoing pursuit.

Final Thoughts: Ignorance Costs More Than We Realize

As entrepreneurs, it’s imperative to recognize that the invisible cost of ignorance can be a silent killer for businesses. The only way to overcome this challenge is through a commitment to continuous learning, skill development, and seeking guidance from those who have already achieved success. By addressing the root cause—the lack of necessary skills—you can eliminate ignorance debt, paving the way for sustained business growth and prosperity.

Marriage provides several economic benefits, including tax breaks, access to higher deductions and credits, the opportunity to combine incomes on tax returns, and the ability to benefit-shop for health insurance. Additionally, married couples can enjoy more Social Security benefits, retirement options, estate planning perks, and cheaper insurance.

Spouses can transfer money and assets between them tax-free, reducing overall tax bills. The financial benefits of marriage extend beyond short-term gains, as there are long-term advantages to joining resources and sharing financial responsibilities. With these economic advantages, marriage can provide stability and financial security for couples.

1. Financial Pros And Cons Of Marriage

Marriage offers numerous economic benefits, such as a higher chance of building wealth, increased financial accountability, and the possibility to piggyback on certain benefits. However, it’s important to consider potential drawbacks, including the potential financial stress of a wedding and a potentially larger tax burden.

Despite these cons, being married can provide a stronger financial foundation for couples.

Marriage is not just about love and companionship; it also has its economic advantages and drawbacks. Before taking the plunge, it is important to consider the financial pros and cons of marriage. Let’s explore some of these factors:

Pro: A Greater Chance At Building Wealth

One of the major financial advantages of marriage is the increased opportunity to build wealth. With two incomes, couples can save and invest more, leading to a stronger financial foundation for their future. Additionally, joint financial planning allows for better resource allocation and strategic decision-making.

Con: The Wedding Could Set You Back

While marriage can bring long-term financial benefits, it’s important to acknowledge the potentially hefty price tag of a wedding. Weddings can be expensive, and the cost may eat into your savings or create significant debt. Proper budgeting and financial planning are crucial to avoid starting your marriage on the wrong financial foot.

Pro: More Financial Accountability

When you tie the knot, you become accountable to your partner not just emotionally but also financially. This increased sense of financial responsibility can lead to better budgeting and spending habits. Working together towards shared financial goals can result in improved financial stability and security.

Con: Additional Money Stress

Combining finances may also introduce additional stress into the relationship. Disagreements about spending, saving, or financial priorities can create tension. Open and honest communication about money, along with regular financial check-ins, can help minimize conflicts and ensure a healthy financial relationship.

Con: You May Face A Bigger Tax Burden

Although marriage can offer certain tax benefits, it’s important to understand that it may also lead to a higher tax burden. Some married couples may face a “marriage penalty” where their combined income pushes them into a higher tax bracket. It’s crucial to consult with a tax professional to understand your specific tax situation and make informed decisions.

Pro: Unemployed?

If one partner is unemployed, marriage can offer a safety net. The working spouse can provide health insurance coverage, retirement benefits, and other financial support. This can help alleviate the stress that comes with unemployment and provide a sense of security during challenging times.

Pro: You Can Piggyback On Benefits

Marriage can bring access to various benefits, including health insurance, retirement plans, and social security benefits. Spouses often have the opportunity to piggyback on their partner’s benefits, taking advantage of lower costs and broader coverage. This can result in significant savings and financial security.

Pro: The Law May Protect You If Your Spouse Dies

In the unfortunate event of a spouse’s death, the law may offer protection to the surviving partner. This can include inheritance rights, Social Security benefits, and other legal protections. These safeguards provide a vital safety net, ensuring financial stability during a difficult period.

Overall, understanding the financial pros and cons of marriage is crucial before making the commitment. Open communication, financial planning, and a shared vision for the future can help navigate these economic considerations and build a strong foundation for a successful partnership.

Credit: www.experian.com

2. Tax Benefits Of Marriage

Marriage offers various economic benefits such as tax breaks, higher income thresholds, and access to each other’s health insurance plans. Additionally, married couples enjoy Social Security benefits, retirement options, estate planning perks, and cheaper insurance rates. These financial advantages make marriage a financially sensible decision.

Tax Breaks For Married Couples

Married couples who file their tax returns jointly may qualify for higher tax deductions and credits than single filers. This is beneficial because you’ll also be combining your incomes on a joint tax return. And if you own a home together, the exclusion for taxes on the proceeds of the sale is doubled.

Joint Tax Returns And Higher Deductions

When married couples file joint tax returns, they have the opportunity to claim higher deductions. This can significantly reduce their overall tax liability and potentially increase their tax refund. By combining their incomes and expenses, they may be eligible for tax benefits and deductions that would not be available to them if they were filing individually.

Tax Benefits For Homeowners

Married couples who own a home together can benefit from various tax advantages. For instance, they may be eligible for deductions on mortgage interest payments, property taxes, and home improvement expenses. These deductions can reduce their taxable income and potentially lower their tax burden.

Exclusion For Taxes On The Sale Of A Home

One of the major tax benefits for married homeowners is the exclusion for taxes on the sale of a home. Normally, individuals can exclude up to a certain amount of the profit from the sale of their home from their taxable income. However, when married couples file joint tax returns, this exclusion amount is doubled, providing them with even greater tax savings.

3. Health Insurance Benefits

One of the significant economic advantages of being married is the access to better health insurance plans. When couples are married, they often have the option to choose between two health insurance plans, allowing them to compare coverages, networks, and costs. This ability to benefit-shop for health insurance can lead to significant savings and better coverage options for both spouses.

A. Access To Better Health Insurance Plans

Marriage provides couples with the opportunity to access each other’s health insurance plans. This means that if one spouse has access to a more comprehensive or affordable health insurance plan, the other spouse can be added as a dependent. This access to multiple options gives married couples the flexibility to choose the most suitable plan for their specific needs.

B. Benefit-shopping For Health Insurance

Benefit-shopping for health insurance is a unique advantage that married couples have. They can compare and evaluate different health insurance plans offered by their employers or through private providers. By shopping around, they can find plans with lower premiums, better coverage for specific medical needs, or access to preferred doctors and hospitals. This ability to compare options and choose the most cost-effective and comprehensive plan can result in substantial savings.

C. Combining Incomes For Joint Tax Returns

Another financial benefit of marriage is the ability to combine incomes for joint tax returns. When married couples file their tax returns jointly, they often qualify for higher tax deductions and credits compared to single filers. This is particularly advantageous because it allows both spouses to benefit from the higher deductions, potentially resulting in lower overall tax liability.

D. Doubled Exclusions For Taxes On The Proceeds Of The Sale Of A Home

For married couples who jointly own a home, there is an additional tax advantage. The exclusion amount for taxes on the proceeds of the sale of a home is doubled for married couples compared to single individuals. This means that when selling their primary residence, married couples can exclude a larger portion of the capital gains from taxes, resulting in potential tax savings.

In summary, the health insurance benefits of marriage provide couples with access to better health insurance plans, the opportunity to benefit-shop for the most suitable coverage, and the ability to combine incomes for joint tax returns. Additionally, the doubled exclusions for taxes on the proceeds of the sale of a home further contribute to the economic advantages of being married.

4. Social Support And Mental Health

Marriage provides economic benefits by offering social support, which can positively impact mental health. Couples are more likely to follow medical advice, prioritize preventative care, and have a healthier lifestyle. This support helps to mitigate depression, isolation, and loneliness that singles without a similar support system may experience.

Marriage not only provides companionship and emotional support but also has several economic benefits. One such benefit is the social support married couples tend to have, which plays a crucial role in maintaining mental health and overall well-being.

Married Couples Tend To Have Social Support

Being in a committed relationship provides a strong social support system for couples. Spouses often rely on each other for emotional support, encouragement, and guidance. This support network helps individuals cope with stress and navigate challenging situations more effectively.

Moreover, married couples are more likely to have a wider circle of friends and family, providing additional sources of support. These relationships can offer advice, assistance, and a sense of belonging that contributes to improved mental health.

Support In Following Doctor’s Advice And Preventative Medical Appointments

In addition to emotional support, married couples often support each other in maintaining good health. This includes following doctor’s advice and attending preventative medical appointments.

Couples can remind and motivate each other to schedule their regular check-ups, screenings, and vaccinations. This collaborative effort increases the chances of early detection and prevention of potential health issues, leading to better overall well-being.

Married People Less Likely To Experience Depression, Isolation, And Loneliness

Research shows that marriage is associated with lower rates of depression, isolation, and loneliness compared to single individuals. This can be attributed to the social support and companionship provided by marriage.

When facing the ups and downs of life, having a spouse to share the joys and sorrows can significantly impact mental health. The emotional bond and support derived from a happy marriage contribute to decreased feelings of loneliness and isolation, resulting in improved mental well-being.

Increased Chances Of Surviving Cancer

Married people have been found to have better survival rates when it comes to fighting cancer. The emotional, practical, and financial support provided by a spouse during this difficult time can make a significant difference in the outcome.

Having a supportive partner who can attend medical appointments, provide comfort, and assist with caregiving allows patients to focus on their treatment and recovery. This support system enhances the chances of beating cancer and ensures a higher quality of life during the journey.

In conclusion, marriage not only offers emotional fulfillment but also provides economic benefits that contribute to better mental health. From social support to improved chances of surviving illnesses, being married plays a vital role in promoting overall well-being.

5. Economic Impact On Socioeconomic Patterns

Marriage and divorce have significant impacts on socioeconomic patterns, shaping the fabric of society. Trends in marriage and divorce rates can reflect broader economic conditions and cultural shifts. For instance, during times of economic prosperity, marriage rates tend to rise as people feel more financially secure and confident about their future. Conversely, in times of economic instability, such as recessions, divorce rates may increase as financial strain can put a strain on relationships.

Economics plays a crucial role in individuals’ decisions regarding marriage. Financial factors, such as income, employment stability, and wealth, often influence people’s readiness to commit to marriage. Economic prospects and perceived financial compatibility are essential considerations when choosing a life partner. Furthermore, economic considerations extend beyond the decision to marry and can impact marital satisfaction and longevity.

The stability of a marriage is influenced by various economic factors. One significant factor is income disparity between spouses. Research suggests that couples with significant income disparities may experience higher levels of marital dissatisfaction and are more likely to face conflicts related to financial matters. Unequal financial contributions can create power imbalances within the relationship, impacting overall satisfaction and stability. Additionally, economic downturns or sudden financial hardships can strain marriages and increase the likelihood of divorce.

Income disparity within a marriage can have lasting effects on marital satisfaction and longevity. Couples with similar income levels often report higher levels of satisfaction, as they experience a sense of financial parity and shared responsibilities. On the other hand, when there is a substantial income gap between spouses, it can lead to feelings of resentment, inequality, and strain on the relationship. Studies have shown that income disparity increases the likelihood of divorce, highlighting the profound impact of economic factors on marital stability.

Frequently Asked Questions Of Economic Benefits Of Marriage

Is There A Financial Benefit To Being Married?

Marriage provides financial benefits such as higher tax deductions and credits, access to each other’s health insurance plans, Social Security benefits, and the ability to transfer money and assets tax-free. Furthermore, married couples tend to support each other in making better financial decisions.

What Are Benefits Of Marriage?

Marriage provides social support, prevents loneliness, and helps in better health care. Couples can also enjoy financial benefits such as higher tax deductions, access to each other’s health insurance plans, and the ability to transfer money and assets tax-free.

What Are The Financial Pros And Cons Of Getting Married?

Financial pros of getting married include a higher chance of building wealth, more financial accountability, potential tax breaks, access to each other’s health insurance plans, and eligibility for higher income thresholds and tax deductions. On the other hand, cons may include potential wedding expenses, additional money stress, and a potentially bigger tax burden.

How Does Economics Affect Marriage?

Marriage has both financial benefits and drawbacks. Married couples can enjoy tax breaks, higher income thresholds, and joint access to health insurance plans. However, weddings can be expensive and may cause financial stress. Overall, economics can impact marriage by affecting financial stability, tax liabilities, and access to benefits.

Conclusion

Marriage not only brings emotional fulfillment but also several economic benefits. Couples who are married tend to support each other, leading to healthier lifestyles and lower healthcare costs. Additionally, married couples can take advantage of tax breaks and higher income thresholds, allowing for greater financial stability.

Social security benefits, retirement options, and cheaper insurance are other advantages that come with marriage. Overall, the economic advantages of marriage make it a wise financial decision for couples to consider.

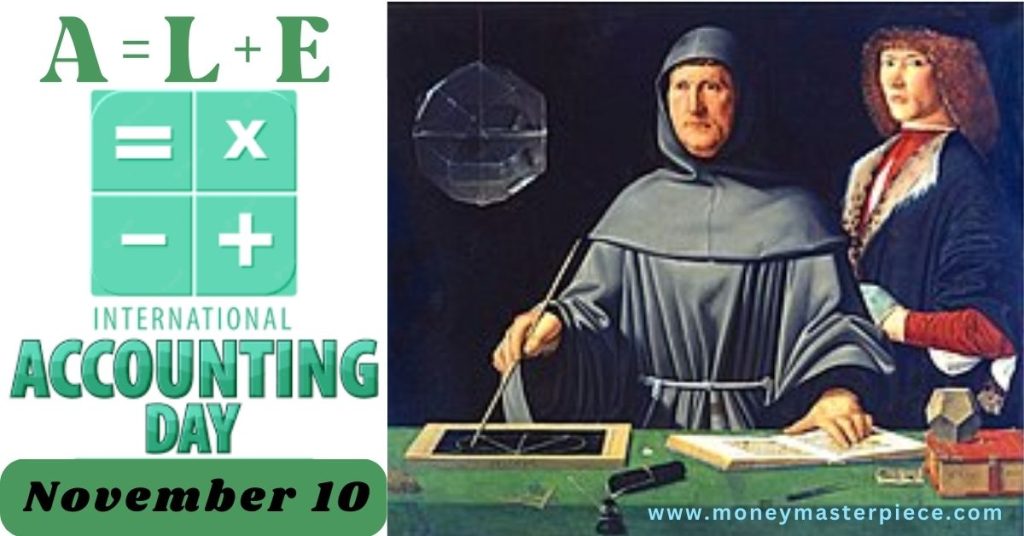

International Accounting Day, observed on November 10th each year, stands as a testament to the indispensable role accountants play in shaping the global economic landscape. This day serves as a celebration of the meticulous professionals who delve into the intricacies of financial records, and provide astute financial advice and audit statements with a commitment to precision. In essence, accountants form the bedrock of financial accountability, ensuring businesses and organizations navigate the complex web of laws and regulations with integrity.

History of Accounting

The history of accounting traces back thousands of years, with early systems documented in Mesopotamia around 5,000 B.C. Ancient Egypt, Babylonia, and Roman records reveal detailed financial calculations.

A pivotal moment occurred in Renaissance Italy when Luca Pacioli introduced double-entry bookkeeping in the late 15th century, earning him the title ‘the father of Accounting.’ International Accounting Day, celebrated on November 10th, commemorates Pacioli’s groundbreaking method. As corporations burgeoned during the Industrial Revolution, the demand for professional accountants surged. Today, accounting is a globally esteemed profession, over a $500 billion market in 2020, with expectations to reach $735.94 billion by 2025.

Luca Pacioli, a visionary thinker and mathematician, unveils the double-entry bookkeeping system, revolutionizing how merchants record financial transactions.

1851: Invention of the Arithmometer

Charles Xavier Thomas de Colmar invents the arithmometer, an ‘adding machine,’ marking the initial steps towards automated computation and streamlining accounting processes.

1930s: Forensic Accounting in Action

IRS accountant Frank Wilson utilizes forensic accounting to expose financial irregularities, leading to the arrest of notorious mafia boss Al Capone. This highlights the power of accounting in uncovering criminal activities.

1955: General Electric’s Computer Purchase

General Electric makes history by purchasing the first computer for accounting functions, emphasizing the growing role of technology in handling financial processes like payroll.

1854: Foundation of the First Professional Accountancy Organization

The Institution of Accountants, established in Glasgow, becomes the first professional accountancy organization, representing and governing the accounting profession.

2001: Enron Scandal and Regulatory Wave

The Enron scandal emerges as a watershed moment, exposing auditing failures and prompting a wave of regulatory changes in the accounting field. This event reshapes accounting practices for increased transparency and ethical standards.

History of International Accounting Day

International Accounting Day originated in 1972 when the San Diego chapter of the California Society of CPAs organized the event, with some attributing the Institute of Management Accountants as the initial planners. However, it officially gained widespread recognition in 1976, inviting various organizations to partake in the celebration. The primary objective was to inspire the younger generation to pursue accounting careers.

International Accounting Day: Elevating the Accounting Profession

International Accounting Day is an annual celebration dedicated to fostering the accounting profession’s growth and acknowledging the vital role accountants play in financial management worldwide. It serves as a platform for professionals to network, fostering a sense of community and offering opportunities for continued education in the dynamic field of accounting.

Beyond professional development, the day is a tribute to accountants’ indispensable contributions. Whether steering through tax complexities or maintaining the financial health of businesses, accountants play a pivotal role.

The celebration extends to those aspiring to join the profession, emphasizing the essential skills—IT proficiency, interpersonal communication, teamwork, organizational acumen, and integrity—required for a successful accounting career. As the day unfolds, it encourages individuals to explore educational paths, from university degrees to apprenticeships, solidifying the accounting industry’s robust future. International Accounting Day underscores not only the present significance of accountants but also the promising opportunities and enduring demand for skilled professionals in this ever-evolving sector.

How to Celebrate Modern Accounting?

International Accounting Day is more than just a time to acknowledge the crucial role accountants play; it’s an opportunity to embrace modern tools and technologies that are reshaping the accounting landscape. Here are some ways to celebrate modern accounting and acknowledge the vital contributions of accountants this International Accounting Day:

Explore Accounting Software:

Dive into the world of user-friendly accounting software that simplifies complex financial tasks. Platforms like QuickBooks, Xero, and FreshBooks offer intuitive interfaces, automating processes and making accounting enjoyable.

Embrace Cloud-Based Solutions:

Say goodbye to the traditional paperwork and embrace the convenience of cloud-based accounting solutions. This allows seamless collaboration between accountants and clients, providing real-time access to financial data.

Attend Webinars and Workshops:

Stay informed about the latest trends and innovations in accounting by attending webinars and workshops. Many organizations and software providers host online events to educate professionals and business owners on cutting-edge practices.

Master Data Analytics:

Take a deep dive into data analytics tools that empower accountants to extract valuable insights from financial data. Understanding data trends and patterns is a modern skill that enhances decision-making processes.

Appreciate Automation:

Celebrate the power of automation in accounting processes. From invoicing to expense tracking, automation reduces manual workload, minimizes errors, and allows accountants to focus on strategic financial planning.

Support the Accounting Community

Get involved in your local or state accounting association. Supporting these organizations fosters a sense of community among accountants and provides a platform for networking, knowledge-sharing, and professional development. Additionally, consider contributing to charities that champion the growth and well-being of the accounting profession.

Engage in Online Communities:

Connect with fellow accountants, finance professionals, and business owners in online communities. Platforms like LinkedIn or specialized accounting forums provide spaces to discuss modern accounting practices, share insights, and learn from each other.

Promote Financial Literacy:

Use International Accounting Day as an opportunity to promote financial literacy. Share resources, articles, or organize virtual sessions to educate individuals about basic accounting principles and the importance of financial management.

Acknowledge Cybersecurity Measures:

In the digital age, protecting financial data is paramount. Acknowledge the significance of cybersecurity measures in accounting. Stay updated on the latest security protocols and ensure that the tools you use prioritize data protection.

Explore Blockchain Technology:

Venture into the realm of blockchain technology, which is making waves in accounting for its transparency and security features. Understand how blockchain can revolutionize processes like auditing and transaction tracking.

Continuous Learning

Embrace the opportunity to delve deeper into the world of accounting. Consider taking a class, reading a book, or watching educational videos to gain a better understanding of the profession. By expanding your knowledge, you not only enhance your appreciation for the field but also contribute to a more financially literate society.

Brush up on current events in the accounting industry – It is always a good idea to make sure that you are up-to-date with all of the latest headlines in the sector so that you will be able to join in the conversation with ease when at an accounting event.

Spread Awareness

Use your voice and platform to spread the word about International Accounting Day. Share information on social media, discuss the importance of accountants with friends and family, and contribute to the broader conversation on the significance of financial accountability.

Express Gratitude to Accountants:

Lastly, take a moment to express gratitude to the accountants in your life. Whether you’re a business owner benefiting from their expertise or an accountant yourself, acknowledging the hard work and adapting to modern tools contributes to a positive and innovative accounting community.

By celebrating modern accounting practices, International Accounting Day becomes a dynamic and forward-looking occasion, showcasing how technology and innovation continue to shape the accounting profession.

International Accounting Day serves as more than just a date on the calendar. It is a reminder of the principles and standards that govern the accounting profession. It underscores the need for ethical practices, transparency, and accountability in financial matters. In an era marked by technological advancements and evolving standards, this day encourages a reflection on the role of accountants in adapting to change while upholding the integrity of their profession.

Wrap Up

As we celebrate International Accounting Day, let us recognize the unsung heroes behind the numbers, the professionals who work diligently to ensure financial clarity and compliance. By doing so, we contribute to a society that values accountability and understands the pivotal role accountants play in steering businesses and organizations towards success.

The wedding industry is a significant contributor to the U.S. Economy, with various small enterprises involved in different sectors such as catering, wedding consulting, and dress manufacturing. Despite its relatively smaller share compared to other sectors, the wedding industry plays a substantial role in the economy.

The industry has experienced a boom in recent times, with an increase in demand colliding with supply constraints and rising inflation, leading couples to cut expenses in certain areas. As a result, businesses within the wedding industry are facing challenges in meeting the requirements of couples while maintaining profitability.

However, the industry continues to evolve, adapting to changing trends and consumer preferences. We will explore the economics of the wedding industry, including its size, profitability, and the impact of various factors on its growth.

Market Size And Growth

The wedding industry is a significant contributor to the U. S. economy, consisting of various enterprises such as caterers, wedding consultants, and dress providers. Its market size and growth make it a profitable industry for businesses involved in wedding services and products.

Current Size Of The Wedding Industry

The wedding industry is a significant sector within the larger event-planning industry, playing a vital role in local economies and contributing to overall economic growth. In the United States alone, the wedding industry is valued at over $70 billion annually, showcasing its scale and importance. This industry consists of various businesses, including wedding planners, caterers, photographers, florists, bridal boutiques, and more. With couples increasingly seeking more elaborate and personalized weddings, the demand for professional wedding services continues to rise.

Trends And Projections For Future Growth

The wedding industry has experienced consistent growth over the years and is expected to continue expanding in the foreseeable future. With changing societal norms and cultural influences, weddings have become more than just a union; they have transformed into an event that reflects the couple’s unique style and personality. This shift has opened up new avenues for businesses within the industry and created opportunities for innovation and creativity.

According to industry experts and market research, the wedding industry is projected to grow at a compound annual growth rate (CAGR) of X% over the next five years. This growth can be attributed to several factors, including a rising number of couples getting married, an increase in average wedding budgets, and the growing popularity of destination weddings. Furthermore, as economies continue to recover from the impact of the COVID-19 pandemic, there is an expected surge in postponed weddings, contributing to the industry’s growth.

Factors Driving The Growth Of The Industry

Several key factors drive the growth of the wedding industry. Firstly, the rising disposable income of individuals and families has enabled couples to allocate larger budgets for their weddings. This increased spending capacity allows them to invest in more lavish venues, premium services, and unique experiences. Moreover, social media platforms have played a significant role in shaping the wedding industry. The ability to showcase extravagant weddings and the rise of wedding influencers have influenced couples to aspire to create their dream weddings, driving the demand for specialized services.

Another factor contributing to the growth of the wedding industry is the trend of couples prioritizing experiences over material possessions. Many modern couples prefer to invest in creating memorable experiences for themselves and their guests rather than accumulating material goods. This shift in mindset has led to an increased demand for experiential elements such as destination weddings, unique wedding themes, and interactive entertainment.

Impact Of Covid-19 On The Wedding Industry

The COVID-19 pandemic had a significant impact on the wedding industry worldwide. Government-imposed restrictions, travel limitations, and health concerns resulted in the postponement or cancellation of countless weddings. This sudden halt in operations severely impacted businesses within the industry, such as venues, caterers, and event planners.

Fortunately, as the vaccination rollout progresses and restrictions ease, the wedding industry is poised for a strong comeback. The pent-up demand for weddings, combined with couples’ resilience and determination to celebrate their special day, is expected to fuel a rapid recovery. As a result, the wedding industry is projected to experience a surge in bookings and a renewed sense of excitement as postponed weddings finally take place.

In conclusion, the wedding industry is a thriving sector with a substantial market size and projected future growth. It is fueled by multiple factors such as rising disposable income, the desire for unique experiences, and the influence of social media. Despite the temporary setback caused by the pandemic, the industry is poised to regain its momentum and continue to contribute to the economy in the years to come.

Economic Impact Of Weddings

Weddings have a significant economic impact on various sectors and industries. From generating revenue to job creation and stimulating local economies, the wedding industry plays a crucial role in supporting and boosting economic growth. Let’s explore the various ways weddings contribute to the economy:

Revenue Generated By Weddings

Weddings are big business, with couples spending a substantial amount of money on their special day. The revenue generated by weddings includes expenses on venues, catering, photography, videography, flowers, decorations, wedding attire, and many other services. According to industry statistics, the wedding industry in the United States alone is worth billions of dollars annually. This significant revenue contributes to the overall economic growth of the country.

Job Creation And Employment Opportunities

The wedding industry creates numerous job opportunities. From wedding planners and coordinators to photographers, florists, caterers, musicians, and more, weddings provide employment to a diverse range of professionals. These job opportunities span across various sectors, contributing to a healthy job market. Additionally, weddings also create seasonal temporary employment for individuals, such as event staff and support personnel.

Stimulating Local Economies

Weddings have a substantial impact on local economies. When couples plan their weddings, they often choose local vendors and suppliers. This support for local businesses injects money into the community, helping small businesses thrive. From wedding venues to local caterers, florists, bakers, and other service providers, weddings contribute to the growth and prosperity of local economies.

Supporting Various Sectors And Industries

The wedding industry supports various sectors and industries, creating a ripple effect in the economy. When couples plan their weddings, they rely on a wide range of services and products. This includes rental companies for event supplies, beauty salons for hair and makeup services, transportation services, stationary suppliers, and more. The demand for these services ensures a steady stream of business for these sectors, further driving economic growth.

All in all, weddings play a vital role in the economy by generating revenue, creating jobs, stimulating local economies, and supporting various sectors and industries. The economic impact of weddings reaches far beyond the bride and groom, making the wedding industry an essential contributor to overall economic growth.

Cost Of Weddings

Weddings are joyous occasions that bring people together to celebrate love and commitment. However, planning a wedding can also be a costly endeavor. From the venue to the flowers, every aspect of a wedding comes with a price tag. In this article, we will explore the various factors that contribute to the cost of weddings, strategies for cost savings in the wedding industry, and provide an overview of average wedding costs and a breakdown of wedding expenses.

Average Wedding Costs

Weddings can vary significantly in cost depending on several factors, including location, size, and level of extravagance. On average, couples in the United States spend around $30,000 to $40,000 on their wedding day. This amount includes expenses related to the ceremony, reception, attire, and other essential elements.

Breakdown Of Wedding Expenses

Let’s take a closer look at how couples allocate their wedding budget:

Expense

Percentage of Budget

Venue

30%

Food and Beverage

20%

Attire

10%

Decorations

10%

Photography and Videography

10%

Entertainment

5%

Flowers

5%

Stationery

5%

Miscellaneous

5%

Factors Influencing Wedding Costs

The cost of a wedding can be influenced by various factors, such as:

Location: Weddings in metropolitan areas or popular destinations often come with a higher price tag due to increased demand.

Guest Count: The number of guests you invite can significantly impact the cost of the venue, catering, and other expenses.

Season: Getting married during peak wedding season may be more expensive, as vendors are in high demand.

Level of Luxury: The more elaborate and luxurious the wedding details, the higher the overall cost.

Strategies For Cost Savings In The Wedding Industry

While weddings can be costly, there are several strategies couples can use to save money without compromising on their special day:

Plan Ahead: Giving yourself ample time to research and book vendors can help you find better deals and negotiate prices.

Guest List Management: Carefully consider your guest list and prioritize inviting close friends and family. By keeping the guest count lower, you can save on catering costs and venue expenses.

DIY Projects: Embrace your creative side by taking on DIY projects for decorations, favors, or even wedding invitations. Not only does this add a personal touch, but it can also save you money.

Off-Peak Season and Midweek Weddings: Consider getting married during off-peak seasons or on a weekday. Many vendors offer discounted rates during these times to attract more business.

Consider All-Inclusive Packages: Opting for all-inclusive wedding packages can help streamline the planning process and potentially save you money compared to booking each element separately.

Credit: www.reuters.com

Small Business Opportunities In The Wedding Industry

The wedding industry offers a multitude of small business opportunities, including caterers, wedding consultants, and dressmakers. With a substantial role in the economy, the wedding industry is a lucrative field for entrepreneurs.

Growth Potential For Small Businesses In The Wedding Industry

The wedding industry is a vast and lucrative market, offering numerous opportunities for small businesses to thrive and grow. With the increasing demand for unique and personalized weddings, small businesses can tap into this growing market and cater to the specific needs and preferences of couples. From wedding planners and photographers to caterers and florists, there is ample room for small businesses to establish themselves and carve out a niche in the wedding industry.

The growth potential for small businesses in the wedding industry is immense. According to industry statistics, the wedding industry in the United States is valued at billions of dollars, with couples spending a significant amount on their special day. This presents small businesses with the opportunity to tap into a large customer base and offer specialized services that meet the evolving demands of modern couples. By focusing on niche segments such as eco-friendly weddings or LGBTQ+ weddings, small businesses can attract clients who are in search of personalized experiences.

Challenges Faced By Small Businesses In The Market

While the wedding industry offers great potential for small businesses, it is not without its challenges. One of the main challenges faced by small businesses is fierce competition. The market is saturated with established wedding vendors and industry giants, making it difficult for small businesses to stand out and gain visibility. However, with a unique selling proposition and a well-defined target audience, small businesses can differentiate themselves and attract clients who are looking for fresh and innovative wedding services.

Another challenge faced by small businesses in the wedding industry is managing finances. Wedding businesses often require upfront investments in equipment, supplies, and marketing efforts. Furthermore, fluctuations in demand throughout the year can make it difficult for small businesses to maintain a steady cash flow. Effective financial planning and budgeting are essential to navigate these challenges and ensure the long-term sustainability of small wedding businesses.

Strategies For Success For Small Businesses

In order to succeed in the wedding industry, small businesses need to employ effective strategies that set them apart from the competition. Here are a few strategies that can help small businesses thrive in the wedding market:

Specialize and differentiate: Identifying a niche market within the wedding industry and offering specialized services can help small businesses stand out and attract clients who are looking for unique experiences.

Build a strong online presence: In today’s digital age, having a strong online presence is crucial for small wedding businesses. Creating a professional website, utilizing social media platforms, and engaging in search engine optimization (SEO) can help attract potential clients and increase visibility.

Network and collaborate: Building relationships with other wedding vendors and professionals can lead to collaborative opportunities and referrals. Networking at industry events and joining wedding associations can open doors to new business opportunities.

Provide exceptional customer service: Customer satisfaction is key to the success of any business. By providing exceptional customer service, going above and beyond to meet clients’ needs, and delivering memorable experiences, small businesses can build a strong reputation and generate positive word-of-mouth.

Case Studies Of Successful Small Wedding Businesses

Here are a few examples of small businesses that have achieved success in the wedding industry:

Business Name

Description

Success Factors

Blissful Blooms Floral Design

A boutique floral design studio specializing in romantic wedding florals.

A family-owned bakery offering custom-designed wedding cakes.

– Creative cake designs – Attention to detail – Collaborations with wedding planners

Enchanting Events Wedding Planning

A wedding planning company specializing in destination weddings.

– Expert knowledge of destination venues – Personalized planning services – Strong network of vendors

These case studies highlight the importance of specialization, exceptional customer service, and strategic collaborations in achieving success in the competitive wedding industry.

Wedding Industry And Local Economies

The wedding industry has a significant impact on local economies, contributing to increased tourism, revenue generation, infrastructure development, and long-term economic growth. Weddings are not only special moments for couples but also economic drivers for various businesses and industries. In this blog post, we will explore the importance of weddings for local economies and the lasting economic effects of the wedding industry.

Importance Of Weddings For Local Economies

Weddings play a vital role in boosting local economies in numerous ways. Here are some key reasons why weddings are important for local economies:

Weddings attract visitors from outside the area, creating a surge in tourism and providing a unique opportunity for local businesses to showcase their products and services.

Guests attending weddings often spend money on accommodation, dining, shopping, and entertainment, thereby stimulating the local economy.

The wedding industry itself creates employment opportunities for local vendors, caterers, wedding planners, florists, photographers, and various other service providers.

Increased Tourism And Revenue Generation

The wedding industry has a profound impact on tourism and revenue generation for local economies. When couples choose a specific location for their wedding, it attracts not only their friends and family but also visitors from other regions or even countries. This influx of wedding guests leads to increased spending on local accommodations, transportation, dining, and other recreational activities. As a result, local businesses experience a surge in revenue, thereby boosting the overall economic health of the region.

Infrastructure Development And Investment

Furthermore, the wedding industry drives infrastructure development and investment in local communities. To cater to the increasing demand for wedding venues and services, local municipalities often invest in the development and improvement of infrastructure. This includes the construction of new wedding venues, renovation of existing event spaces, enhancement of transportation networks, and improvement of public facilities like parks and gardens. These investments not only benefit the wedding industry but also contribute to the overall growth and development of the region.

Long-term Economic Impact Of The Wedding Industry

The long-term economic impact of the wedding industry extends far beyond the immediate boost in tourism and revenue generation. Here are some ways in which the wedding industry continues to positively impact local economies:

The wedding industry creates a ripple effect, as the money spent by wedding guests flows into various sectors of the economy, supporting other local businesses and industries.

Successful weddings can enhance the reputation of a location as a desirable wedding destination, attracting more couples and businesses to the area over time.

Local businesses that thrive in the wedding industry can expand and create additional job opportunities, further stimulating economic growth.

Overall, the wedding industry plays a crucial role in bolstering local economies by increasing tourism, generating revenue, promoting infrastructure development, and fostering long-term economic growth.

FAQs

What Is The Economic Impact Of Weddings?

The wedding industry has a significant economic impact, with multiple smaller enterprises contributing to different sectors. It plays a substantial role in the US economy, although its share may be relatively less significant compared to other sectors. The industry is currently facing challenges due to supply constraints and inflation, leading couples to cut expenses.

How Profitable Is The Wedding Industry?

The wedding industry is highly profitable, with multiple smaller enterprises involved in different sectors such as catering, wedding consulting, and dressmaking. It plays a substantial role in the US economy, although its share is relatively less significant compared to other sectors.

The industry is currently experiencing a boom in demand, but it is also facing challenges due to supply constraints and rising costs.

Is There Money In The Wedding Industry?

The wedding industry is financially lucrative, with various enterprises like caterers, wedding consultants, and dressmakers contributing to its success. It plays a significant role in the US economy, although its share may be comparatively smaller. However, the industry is currently facing challenges due to inflation and limited supply.

Couples are cutting expenses, especially on beauty services, officiants, and party favors for guests. Despite these challenges, the wedding industry continues to thrive.

How Big Of An Industry Is The Wedding Industry?

The wedding industry is large and thriving made up of multiple small enterprises. It includes various sectors such as caterers, wedding consultants, and dress designers. It plays a substantial role in the economy, although its share is relatively less significant compared to other sectors.

Conclusion

The wedding industry is a thriving sector with significant economic impact. From caterers and wedding consultants to dressmakers and various suppliers, the industry encompasses multiple smaller enterprises. Couples’ spending patterns have shifted due to inflation and constrained supply, resulting in adjustments to wedding budgets.

However, despite these challenges, the industry continues to boom, creating opportunities for businesses and contributing to the overall economy. As weddings make a comeback after the pandemic, the wedding industry shows resilience and adaptability.

The economic aspects of marriage involve partners providing economic support to each other, pooling resources and income to meet family needs, and improving their standard of living through combined income. Marriage also contributes to the stability of society.

The Economic Aspects Of Marriage

Marriage serves important economic functions, such as pooling resources and income to fulfill family needs, improving the partners’ standard of living, and contributing to the stability of society. Additionally, marriage can promote economic equality between men and women through labor division based on sex.

Understanding the Economic Functions of Marriage

Marriage is not only a union of two individuals but also a partnership that involves various aspects, including economic functions. In this section, we will dive deeper into the economic aspects of marriage and how they contribute to the overall stability and prosperity of both the couple and society as a whole.

Economic Help And Support In Marriage

One of the fundamental economic functions of marriage is the provision of help and support between partners. In a marriage, both individuals contribute to the family’s financial well-being through their earnings and resources. This mutual support system ensures that each partner has the necessary financial assistance, creating a sense of security and stability.

Pooling Of Resources And Income

To fulfill the various needs of a family, marriage involves the pooling of resources and income. When a couple combines their financial assets, they are able to effectively allocate their resources to meet shared goals and obligations. This pooling of resources allows for a more efficient management of finances, enabling the couple to navigate through life’s challenges and achieve mutual prosperity.

Fulfilling Family Needs Through Combined Income

By pooling their income, married couples are better equipped to meet the needs of their family. Whether it’s providing for children’s education, healthcare expenses, or day-to-day necessities, the combined income of spouses provides a stronger financial foundation. This allows the family to enjoy a higher standard of living and access opportunities that might otherwise be unattainable with separate incomes.

Improved Standard Of Living

Marriage plays a crucial role in improving the standard of living for both partners. With the combined efforts, financial resources, and division of labor, married couples are often able to achieve a higher quality of life compared to individuals who are not in a marital partnership. This higher standard of living encompasses not only material possessions but also access to better healthcare, education, and leisure activities that contribute to overall well-being.

Contribution To The Stability Of Society

Beyond the individual benefits, marriage also serves as a pillar of stability for society as a whole. When couples enter into a committed partnership, they commit to building a future together, contributing to the overall social fabric. Strong and stable marriages foster a sense of community, promote family values, and provide a stable environment for raising children. By nurturing stable and supportive relationships, marriage acts as a foundation for a flourishing society.

In conclusion, marriage goes beyond emotional and romantic aspects. It holds significant economic functions that contribute to the well-being of both individuals and society. From economic help and support to improved living standards, the pooling of resources and income in marriage plays a vital role in fostering stability and prosperity. By understanding and appreciating these economic aspects of marriage, we can acknowledge the multifaceted nature of this institution.

The Role Of Economic Transactions In Marriage

Marriage is not only a union of hearts, but it is also an economic institution. Economic transactions play a crucial role in marriage, shaping the dynamics and structure of relationships. These transactions come in various forms and have implications for power dynamics, gender roles, and economic equality. Let’s delve into some common forms of economic transactions in marriage.

Bride Price As A Common Form Of Economic Transaction

Bride price, also known as bridewealth or bride token, is a customary practice prevalent in many cultures. In this practice, the groom’s family provides goods, money, or other valuable assets to the bride’s family as compensation for marrying their daughter. The bride price serves as a show of appreciation and helps solidify the alliance between the two families. It can also serve as a measure of the groom’s ability to support his future wife.

Bride Service As An Alternative Form Of Economic Transaction

Another form of economic transaction in marriage is bride service. In this arrangement, the groom works for the bride’s family for a certain period as a form of compensation for the right to marry the bride. This work can range from chores to labor-intensive tasks. The purpose of bride service is often to prove the groom’s commitment and ability to provide for the bride and her family.

Labour Division Based On Sex For Economic Equality

Gender plays a significant role in economic transactions within marriages. In many societies, there is an established labor division based on sex, where men primarily engage in income-generating activities, and women are responsible for domestic tasks and caregiving. This division aims to achieve economic equality by ensuring that both partners contribute to the overall well-being of the household. However, it can also perpetuate gender inequalities and limit opportunities for women in the workforce.

To promote economic equality within marriages, it is essential to challenge traditional gender roles and encourage shared responsibilities in both income generation and domestic tasks. This shift can lead to more balanced and equitable relationships, where partners have equal opportunities to contribute financially and personally.

Marriage As A Structure For Fulfilling Needs

Marriage serves as a structure within which people’s various needs are fulfilled. Beyond economic transactions, marriage ensures the fulfillment of basic needs such as safety, food, clothing, and shelter. It provides a framework for individuals to rely on each other for support and shared resources. By pooling their economic resources, married couples can improve their standard of living and provide a stable foundation for their family.

In conclusion, economic transactions play a crucial role in marriage, shaping the dynamics of relationships and contributing to economic equality or inequality. Understanding the various forms of economic transactions in marriage allows us to analyze the societal norms and power dynamics surrounding unions. By promoting equitable labor division and challenging traditional gender roles, we can strive for more balanced and fulfilling marriages.

The Political Economy Of Marriage

Marriage is not just an institution based on love and companionship. It also has significant economic aspects that cannot be disregarded. One way to understand this is through the lens of the political economy of marriage. This perspective views marriage as a marketplace, where various economic transactions and exchanges take place.

Viewing Marriage As A Marketplace

When we view marriage as a marketplace, we can see that individuals, families, and even societies engage in economic decision-making processes when it comes to choosing a partner or arranging a marriage. Like any marketplace, there are specific criteria, preferences, and negotiations involved.

Seeking Educated And Employed Partners

In the marriage market, education and employment become crucial factors for both men and women. A well-educated and employed partner is often sought after because they offer economic stability and potential financial security for the future. This preference stems from the realization that a partner’s education and employment status can significantly impact the overall economic well-being of the marriage.

Payment And Exchange In The Marriage Market

Within the marketplace of marriage, various forms of payment and exchange occur. One such form is dowry, which can take different shapes and forms in different cultures. Dowry is an economic transaction where the bride’s family provides goods, wealth, or property to the groom’s family as a way of compensating for their daughter’s marriage.

Apart from dowry, other forms of economic transactions include bride price, bride service, exchange of females, gift exchange, and indirect dowry. These transactions serve as crucial aspects in the negotiation and establishment of a marriage contract.

Forms of Economic Transactions in Marriage

Dowry

Bride price

Bride service

Exchange of females

Gift exchange

Indirect dowry

These economic transactions not only shape the financial dynamics of the marriage but also reflect societal norms, power dynamics, and gender roles within a given culture or community.

Overall, understanding the political economy of marriage allows us to recognize the interconnectedness of economics and social institutions. Through this perspective, we can gain insights into how economic factors influence partner preferences, negotiations, and the overall economic well-being of married individuals and families.

The Economic Impact Of Marriage On Individuals And Society

Marriage is not only a sacred union between two individuals, but it also has significant economic implications. When two people decide to tie the knot, their financial lives become interwoven, which can have both advantages and disadvantages. In this section, we will delve deeper into the various economic aspects of marriage, shedding light on the financial advantages and disadvantages, the importance of economic considerations in choosing a spouse, the influence of marriage on career and earning potential, as well as the role of marriage in financial stability and social mobility. By understanding these economic dynamics, we can gain a clearer picture of how marriage impacts individuals and society as a whole.

Financial Advantages And Disadvantages Of Marriage

When it comes to finances, marriage can bring about both advantages and disadvantages. On the one hand, pooling resources and sharing expenses can lead to greater financial stability and the ability to achieve common financial goals. Couples can benefit from joint bank accounts, shared health insurance policies, and tax advantages. Additionally, married individuals may have access to better credit terms and eligibility for certain government benefits.

On the other hand, marriage can also lead to financial disadvantages. In cases where one spouse has a poor credit history or a significant amount of debt, it can impact the couple’s ability to secure loans or favorable interest rates. Moreover, if the couple decides to divorce, the division of assets and alimony payments can have a substantial financial impact on both parties.

Economic Considerations In Choosing A Spouse

When choosing a life partner, economic considerations can play a crucial role. While love and compatibility are essential, individuals often take into account the financial stability and earning potential of their potential spouse. This consideration is rooted in the desire for a secure financial future and the ability to achieve shared goals and aspirations.

Factors such as educational background, career prospects, and financial responsibility are often taken into account when making this decision. In some cases, individuals may prioritize finding a partner who can contribute to the household income or offer financial stability, while others may prioritize shared financial values and goals.

Influence Of Marriage On Career And Earning Potential

Marriage can significantly influence an individual’s career and earning potential. For instance, studies show that married men tend to earn higher wages compared to their single counterparts. This wage premium is often attributed to married men’s motivation to provide for their families and the increased responsibility that comes with marriage.

On the other hand, women’s career trajectories and earning potential can be affected by marriage in various ways. While some women may experience a “marriage penalty,” characterized by decreased labor force participation and lower wages, others may benefit from the “marriage bonus,” where marriage provides opportunities for shared household responsibilities and support in career advancement.

Navigating The Economic Challenges And Opportunities In Marriage

Marriage is not just a union of hearts and souls, but also a merging of financial responsibilities. Managing the economic aspects of marriage can be both challenging and rewarding. From shared expenses to financial planning, income disparities, and the economic implications of divorce, it’s important for couples to navigate these aspects to ensure a stable and prosperous future together.

Managing Finances As A Married Couple

When it comes to managing finances as a married couple, open communication and transparency are key. Both partners should be involved in financial decision-making and have a clear understanding of each other’s income, expenses, and financial goals. Here are some strategies to help manage finances effectively:

Create a joint bank account for shared expenses and savings goals.

Set a budget together to track monthly expenses and identify areas for savings.

Discuss financial priorities and establish short-term and long-term financial goals as a couple.

Regularly review your financial situation and make any necessary adjustments to stay on track.

Consider consulting a financial advisor to get professional guidance on investment strategies and retirement planning.

Shared Expenses And Financial Planning

Shared expenses play a crucial role in the economic dynamics of marriage. It’s important for couples to have open and honest conversations about their financial obligations and expectations. Here are some key considerations when it comes to shared expenses and financial planning:

Create a comprehensive list of shared expenses, including rent or mortgage payments, utility bills, groceries, and transportation costs.

Discuss how you will divide these expenses, taking into account each partner’s income and financial situation.

Consider establishing a joint account for shared expenses and contribute a predetermined amount each month.

Regularly review and adjust your shared expenses to ensure that your financial arrangement is fair and equitable.

Plan for unexpected expenses, such as medical emergencies or home repairs, by setting aside an emergency fund.

Economic Implications Of Divorce And Separation

While no one enters a marriage with the intention of divorce or separation, it’s important to be aware of the potential economic implications in case the relationship ends. Divorce involves the division of assets, spousal support, and potential child support payments. Here are some considerations regarding the economic implications of divorce and separation:

Consideration

Explanation

Asset division

Understanding the laws and regulations regarding the division of assets in your jurisdiction can help you prepare for a fair and equitable settlement.

Spousal support

Spousal support, also known as alimony, may be awarded to one partner depending on factors such as income disparity and duration of the marriage.

Child support

If you have children, it’s important to consider the financial responsibilities associated with child support, including education, healthcare, and other expenses.

Addressing Income Disparities In Marriage

Income disparities can arise in any marriage due to variations in education, career paths, or other factors. It’s crucial to address these disparities to ensure financial stability and equality within the relationship. Here are some strategies for addressing income disparities in marriage:

Openly discuss and acknowledge the income disparities between partners.

Explore ways to support and uplift the partner with the lower income, such as investing in education or career development.

Consider strategies to increase the overall household income, such as pursuing additional sources of income or starting a joint business venture.

Create a financial plan that takes into account both partners’ current income and future earning potential.

By addressing these economic aspects of marriage, couples can strengthen their financial foundation and enhance their overall well-being. Open communication, transparency, and mutual understanding are crucial in navigating the economic challenges and opportunities that come with marriage.

Credit: www.worldfinance.com

Frequently Asked Questions

What Are The Economic Functions Of Marriage In Sociology?

Partners in marriage provide economic support and pool resources to fulfill family needs, improving their standard of living and contributing to societal stability. Marriage also promotes economic equality and fulfills basic needs for safety, food, clothing, and shelter. Additionally, marriage involves economic transactions such as bride price, bride service, dowry, and gift exchange.

What Is The Most Common Form Of Economic Transaction At Marriage?

The most common form of economic transaction at marriage is bride price, where the groom’s family gives goods or money to the bride’s family as compensation.

What Is The Economic Function Of Marriage Anthropology?

The economic function of marriage in anthropology is to promote economic equality through the division of labor based on sex. Marriage provides a structure for fulfilling people’s needs for safety, food, clothing, and shelter. It also involves economic transactions such as bride price, bride service, dowry, and gift exchange.

What Is The Political Economy Of Marriage?

The political economy of marriage refers to the economic aspects and transactions involved in forming and maintaining a marriage. It can be seen as a marketplace where the bride’s family seeks an educated and well-earning groom and pays a price for doing so.

Conclusion

Marriage has long been recognized as having significant economic aspects. Partners in a marriage often contribute to each other’s financial needs and collectively improve their standard of living. Additionally, marriage plays a crucial role in the stability of society. By pooling resources and income, couples can navigate economic challenges more effectively.

Understanding the economic functions of marriage is essential in comprehending its impact on individuals and society as a whole. Overall, marriage serves as a foundation for financial support and contributes to the well-being of both individuals and the community.

The economics of marriage includes the economic analysis of household formation and break-up, production and distribution decisions within the household, and the financial benefits such as tax breaks, social security benefits, insurance savings, and access to benefits that come with being married. It is closely related to the law and economics of marriages and households.

Married adults have made greater economic gains over the past four decades than unmarried individuals, and applying economic principles such as cost-benefit analysis, moral hazard, and loss aversion to marriage can contribute to a successful partnership. Additionally, married couples share the responsibility of looking after their home, resulting in less time lost compared to those who live alone.

The Economic Benefits Of Marriage

Marriage offers various economic benefits, such as tax breaks, Social Security benefits, access to credit, insurance savings, and the ability to share costs. These advantages, however, vary depending on individual circumstances and are just one aspect of the financial picture.

Tax Breaks And Financial Incentives For Married Couples

Marriage comes with various economic benefits, and one significant advantage is the availability of tax breaks and financial incentives for married couples. When both partners join in matrimony, they can take advantage of certain tax deductions and credits. For example, married couples have the option to file their taxes jointly, combining their incomes and potentially lowering their overall tax burden. Additionally, they may qualify for a higher standard deduction, resulting in a more favorable tax outcome. These tax benefits can free up extra funds that couples can use for savings, investments, or other expenses.

Social Security Benefits And Insurance Savings

Another economic benefit of marriage is the access to Social Security benefits and potential insurance savings. In the United States, for instance, married individuals may be eligible to receive a portion of their spouse’s Social Security benefits, which can align with their retirement plans and provide essential financial support. Moreover, being married can lead to savings on insurance policies such as health, auto, and home insurance. Insurance companies often offer discounted rates for married couples due to perceived stability and reduced risks.

Access To Shared Benefits And Resources

Marriage allows for the pooling of resources and access to shared benefits. When couples marry, they often combine their finances and gain access to joint bank accounts, investments, and assets. This pooling of resources can lead to increased financial stability and the ability to pursue shared financial goals such as homeownership, education, or starting a business. Additionally, being married can provide access to employer-provided benefits such as health insurance, retirement plans, and flexible spending accounts, which may not be available to unmarried partners.

Individual Retirement Account Contributions

Marriage can also offer advantages when it comes to individual retirement account (IRA) contributions. In some countries, including the United States, married couples may be able to contribute to an IRA on behalf of their spouse, even if the spouse doesn’t have their own income. This can result in increased retirement savings for both partners and provide financial security in the later years of life.

Sharing Costs And Economic Efficiency

One of the most significant economic benefits of marriage is the ability to share costs and achieve economic efficiency. When couples marry, they often combine households and share expenses such as rent or mortgage payments, utility bills, groceries, and transportation costs. Sharing these costs can lead to significant savings compared to maintaining separate households and managing expenses individually. Additionally, couples can take advantage of bulk buying and discounts, further reducing costs.

In conclusion, marriage brings several economic benefits that can help couples build a stable financial future. From tax breaks and financial incentives to access to shared resources, these advantages can enhance financial security and stability. Furthermore, the ability to share costs and achieve economic efficiency can lead to increased savings and overall economic well-being.

Gary Becker’s Theory Of Marriage

Gary Becker’s Theory of Marriage, a prominent economic analysis of household formation and decisions within the household, explores the concept of marriage as an economic exchange. It emphasizes how individuals make rational choices based on costs, benefits, and incentives, similar to nations engaging in trade.

Understanding The Economic Motivations Behind Marriage