Financial struggles can be challenging, but helping someone navigate through them can make a significant impact on their life. In this guide, we’ll explore practical strategies and tips on how to assist someone who might be struggling with money management. Being ‘bad with money’ often stems from a lack of financial literacy or unforeseen circumstances. Let’s delve into how you can offer support in a constructive and empathetic manner.

How to Help Someone ‘Bad with Money’?

Understanding the Situation:

The first step in helping someone with financial challenges is to foster open communication. Create a safe space for them to discuss their situation without judgment. Identify specific financial pain points such as tracking spending habits, analyzing debt, and understanding their financial goals.

Understanding Their Money Story:

Everyone has a unique relationship with money shaped by their experiences and emotions. Rather than simplifying the issue to “being bad with money,” take the time to understand their money story. Pay attention to underlying feelings such as anxiety, inadequacy, or defiance that may be influencing their financial habits. By getting to the root causes, you can offer more tailored and effective support.

Education on Basic Financial Literacy:

Financial literacy is crucial for making informed decisions. Break down complex financial terms and introduce budgeting concepts. Guide them in creating a simple budget, differentiating needs from wants, and offer an overview of saving and investing.

Creating a Realistic Financial Plan:

Work together to set achievable short-term and long-term financial goals. Develop a step-by-step action plan that prioritizes paying off debts, building an emergency fund, and saving for specific milestones. This plan should be personalized to their unique situation.

Seeking Professional Guidance:

Introduce the concept of financial advisors and stress the importance of seeking expert advice. Professionals can provide personalized guidance, helping to create a comprehensive financial strategy that aligns with their goals.

Encouraging Behavioral Changes:

Identify spending triggers and work towards establishing healthy financial habits. Regularly reviewing financial status and learning from past mistakes can contribute to positive behavioral changes.

Encouragement as a Motivator:

Positive reinforcement is a powerful motivator. When they take positive steps, be their cheerleader. Acknowledge and celebrate even small wins, such as sticking to a budget for a week. Building financial discipline is a gradual process, and patience is key. Your encouragement can boost their self-efficacy and motivation, fostering a positive mindset toward financial responsibility.

Utilizing Technology and Tools:

Introduce budgeting apps and financial tools that can simplify the process. Automating savings and bill payments, as well as monitoring progress through tracking apps, can bring a sense of control and organization.

Building a Support System:

Encourage accountability by involving friends or family in the financial journey. Celebrate financial milestones, and provide ongoing encouragement to keep them motivated.

Dealing with Emotional Aspects:

Financial struggles often come with emotional stress. Address anxiety related to finances, provide emotional support, and connect financial well-being with overall well-being. Recognize the emotional toll money issues can take.

Listening Without Judgment: A Compassionate Approach to Financial Support

Financial challenges are deeply personal, often rooted in emotions and past experiences. Instead of approaching someone struggling with money with tough love or criticism, adopting a compassionate and open-minded stance can be more effective. Listening without judgment is a crucial first step.

Conclusion:

Assisting someone who is ‘bad with money’ requires a combination of education, empathy, and practical strategies. By fostering open communication, providing educational resources, and encouraging behavioral changes, you can make a positive impact on their financial journey. Remember, persistence and patience are key, and celebrating even small victories can contribute to long-term financial well-being. By offering support, you’re not just helping with money – you’re contributing to a brighter financial future.

Money, often perceived as a mere numerical entity, is, in reality, a dance between the cold arithmetic of spreadsheets and the complex emotions of human nature. In his book, “The Psychology of Money,” Morgan Housel unravels the intricate relationship between financial decisions and the intricate fabric of our lives. In this exploration, we’ll dissect key lessons from the book through the lenses of personal finance and productivity.

Lessons and Perspectives

Financial DNA: Unraveling Personal Histories

Our financial decisions are deeply rooted in our unique life experiences, forming our financial DNA. Housel emphasizes how events like stock market movements and inflation during our formative years shape our attitudes towards money. Understanding this, we can appreciate that people aren’t inherently “crazy” with their financial decisions; rather, they are navigating the world based on their personal life experiences and worldview.

Warren Buffett’s journey is a testament to the power of compounding. Starting to invest at a young age allowed him to harness the magic of compounding over time. This highlights the counterintuitive nature of compounding, where small, consistent investments can lead to substantial wealth. The lesson here is clear: start early, be consistent, and let time work its compounding magic.

Our inclination towards pessimism in financial matters is explored by Housel. While bad news tends to grab attention, the slow progress and positive changes over time often go unnoticed. Recognizing this bias is crucial for making sound financial decisions. It’s about striking a balance between being realistic about challenges and maintaining optimism about the gradual improvements that unfold over time.

Two Forgotten Elements: Luck and Risk

Success is a complex interplay of talent, luck, and risk. Housel illustrates this through the story of Bill Gates, Paul Allen, and Kent Evans. While Gates and Allen had exceptional talent and a unique advantage, Evans faced an unfortunate tail event. Understanding the role of luck and risk in financial decisions fosters humility and a broader perspective. It’s a reminder that success is a combination of factors, and acknowledging this complexity is key.

The Key to Happiness: Controlling Your Time

The pursuit of wealth often intertwines with the desire for happiness. Housel suggests that the true key to happiness lies in having control over your time. While financial success is a goal for many, it should not come at the expense of losing control over your life. This lesson emphasizes the importance of aligning financial pursuits with the ability to lead a fulfilling and balanced life.

Tail Events: Embracing the Unpredictable

Housel introduces the concept of long tails, where a small number of events can account for the majority of outcomes. Understanding and embracing the unpredictable nature of tail events is vital, especially in investing. The examples of art collecting, venture capital, and business highlight how a few outlier events can significantly impact overall success.

Distinguishing between being rich and being wealthy is a crucial lesson. True wealth lies in financial assets yet to be spent, emphasizing the importance of self-control and restraint. Accumulating wealth isn’t about showcasing possessions but about building assets and making prudent investment decisions for the future.

The Real Price: Accepting the Uncertainty

Investing, like climbing a mountain, comes with inherent uncertainty and risk. Recognizing and accepting the emotional price of volatility is crucial. Housel compares investing to buying a car, highlighting the need to pay the price, whether in dollars or emotions, for the potential rewards. Understanding that success in investing requires enduring the challenges is essential for a fruitful journey.

Hedonic Treadmills: Knowing When Enough Is Enough

The concept of Hedonic Adaptation warns against the never-ending pursuit of goals without recognizing when enough is enough. The examples of Bernie Madoff and Gupta emphasize that unlimited wealth doesn’t guarantee happiness. Knowing when to stop and finding contentment along the way is crucial for a balanced and fulfilling life.

Resource Recommendations

Before we delve into the detailed implementation of these lessons, let’s explore some additional resources that can complement and deepen your understanding of personal finance and productivity:

“Your Money or Your Life” by Vicki Robin and Joe Dominguez

This book offers a transformative approach to money and life. It encourages readers to examine their relationship with money, align their spending with their values, and achieve financial independence.

“Atomic Habits” by James Clear

James Clear explores the science of habit formation, providing actionable insights into building good habits and breaking bad ones. Understanding habits is crucial for maintaining consistent financial practices and increasing productivity.

“The Millionaire Next Door” by Thomas J. Stanley and William D. Danko

The authors analyze the habits and characteristics of millionaires, debunking common myths and providing practical advice on accumulating wealth. It’s a valuable resource for understanding the mindset of successful individuals.

Now, let’s dive into the practical application of the lessons from “The Psychology of Money.”

Implementation of Lessons

Assess Your Financial DNA

Reflect on your personal experiences with money. Identify any biases or beliefs that may be influencing your financial decisions. Understanding your financial DNA is the first step towards making intentional and informed choices.

Start Early, Invest Consistently

Encourage individuals to start investing early, even with small amounts. Emphasize the power of compounding and how consistent contributions over time can lead to significant wealth accumulation. Recommend resources on beginner-friendly investment strategies.

Balance Realism and Optimism

Educate individuals about the bias towards pessimism in financial matters. Highlight the importance of staying informed while maintaining a realistic but optimistic outlook on long-term financial trends. Share success stories that emphasize gradual improvements.

Acknowledge the Role of Luck and Risk

Discuss the interconnectedness of talent, luck, and risk in financial success. Encourage humility by recognizing that external factors play a role in one’s financial journey. Foster a mindset that embraces uncertainty while making informed decisions.

Prioritize Time Control Over Material Wealth

Guide individuals to assess their priorities. Help them understand that the pursuit of material wealth, without control over one’s time, may lead to dissatisfaction. Provide tools and strategies for achieving a balance between financial goals and personal well-being.

Embrace Tail Events in Investing

Explain the concept of long tails in investing. Encourage a diversified investment approach that acknowledges the potential impact of outlier events. Share case studies or examples where a small number of investments significantly influenced overall returns.

Distinguish Between True Wealth and Being Rich

Emphasize the importance of building financial assets for the future. Challenge the notion that visible possessions equate to true wealth. Provide guidance on saving, investing, and making decisions that contribute to long-term financial well-being.

Accept the Emotional Price of Investing

Prepare individuals for the emotional challenges of investing. Share stories of successful investors who endured market volatility. Highlight the importance of patience and long-term thinking. Recommend resources on managing investment-related stress and anxiety.

Recognize When Enough Is Enough

Discuss the concept of Hedonic Adaptation. Encourage individuals to define their financial goals clearly and recognize when they’ve achieved them. Promote contentment and mindfulness in financial decision-making, preventing the endless pursuit of unattainable goals.

Conclusion

As personal finance advisors and productivity coaches, understanding the psychology of money is paramount. Morgan Housel’s insights provide a roadmap for navigating the intricate dance between financial decisions and human nature. By applying these lessons, we can guide individuals toward intentional financial choices, fostering a harmonious relationship between wealth and well-being.

In a world inundated with choices, the decisions we make about our finances shape the narrative of our lives. Paula Pant, the insightful host of the “Afford Anything Podcast,” offers a refreshing and profound perspective: “You can afford anything, but not everything.” This mantra extends beyond the realm of money; it encompasses time, focus, and energy. In this blog post, we will delve into the essence of Pant’s philosophy and explore how it can transform your approach to both money and life.

First Principles Thinking: Unearth Your Values

Pant advocates for first principles thinking, urging us to delve deep into our values—the roots that anchor the tree of our lives. By understanding and identifying our core values, we establish a robust philosophy that guides our goals and objectives. From this foundational understanding, strategies emerge, leading to specific tactics and products. The key lies in recognizing that financial decisions are not isolated leaves but interconnected elements of a rooted system.

First principles thinking is about stripping away the superficial layers and understanding the fundamental truths that govern our lives. In the context of financial decision-making, it involves asking profound questions: What truly matters to me? What are my long-term goals? What kind of life do I want to lead? By addressing these questions, we develop a comprehensive understanding of our values, allowing us to make financial choices that align with our deepest convictions.

Financial Independence: Beyond Retirement

Pant reframes the concept of financial independence (FI) as a gateway to freedom, opportunity, and choice. It’s not merely about accumulating wealth for old age but creating a life of abundance and flexibility. Financial independence, as Pant envisions it, is achieved when passive income covers basic expenses, thereby unlocking a world of possibilities.

Traditionally, discussions around financial independence have been framed in the context of delayed gratification—saving now to enjoy life in retirement. Pant challenges this narrative, emphasizing that financial independence should be a tool for enjoying life today while still securing a comfortable future. She envisions a life where choices are made without worrying about the mundane, an existence fueled by the flourishing of freedom.

Simple Steps to Independence: Grow, Invest, Repeat

The pursuit of financial independence, according to Pant, boils down to three simple yet powerful steps: grow the gap, invest the gap, and repeat. Growing the gap involves either earning more or spending less. Pant suggests adopting a mindset that allows for the continuous expansion of the gap between income and expenses.

Pant’s philosophy introduces the 20% rule: she advocates for saving and investing at least 20% of one’s income. This encompasses contributions to retirement savings, investments in various financial instruments, and building up an emergency fund. The 20% rule serves as a practical guideline, encouraging individuals to save and invest a substantial portion of their income while still allowing for a comfortable lifestyle.

Importantly, Pant emphasizes that financial independence is not a destination but a lifelong practice of money management. It’s an ongoing journey that requires continuous attention and adaptation. Money management, in Pant’s view, is not just a means to an end but a skill that, when honed, contributes to a life well-lived.

Surviving a Scary Economy: Harness Fear for Financial Wisdom

In times of global volatility, Pant encourages embracing fear as a motivator for making wise financial decisions. Drawing parallels with historical uncertainties, she underscores the perpetual nature of change. Pant’s personal journey to financial independence was fueled by a desire to mitigate anxiety about the future, and she believes that fear can be a transformative force.

Rather than succumbing to fear, Pant suggests harnessing it as fuel for making intentional decisions about money, time, and effort. Fear, when approached with a proactive mindset, can be a powerful motivator for building resilience and making strategic choices that align with one’s values and goals.

Conclusion: Building a Life of Intention

Paula Pant’s philosophy extends beyond conventional financial advice; it serves as a guide to intentional living. By understanding first principles, reframing financial independence, and taking simple yet impactful steps toward financial freedom, Pant’s approach offers a roadmap for building a life aligned with one’s values.

In a world brimming with choices, Pant encourages us to prioritize what truly matters. Her philosophy fosters a sense of purpose and joy, emphasizing the importance of aligning financial decisions with a deeper understanding of our values and goals. Embracing the Afford Anything philosophy isn’t just about managing money; it’s about creating a life that reflects our most profound convictions and aspirations.

In the complex tapestry of life, every choice we make is a thread that weaves into the fabric of our existence. Imagine each decision as a note in the symphony of our journey, creating a melody unique to our experiences. At the heart of this intricate dance lies a fundamental truth: “You can afford anything, but not everything.” In this exploration, we will delve into the philosophy of intentional living, financial independence, and the art of decision-making.

Unveiling First Principles Thinking

Defining First Principles Thinking

At the core of wise decision-making is the concept of first principles thinking. It’s about peeling back the layers of complexity to uncover the fundamental truths. Picture it as a tree—its roots represent our values, the trunk embodies our philosophy of life, branches symbolize our strategies, and leaves are the tactics and products we choose. By understanding and aligning with our values, we create a solid foundation for intentional decision-making.

Reframing Financial Independence

Beyond Retirement

Financial independence (FI) is often misunderstood as a distant goal tied to retirement. However, let’s reframe this narrative. FI is the point where your passive income covers basic expenses, unleashing a world of opportunities and choices. It’s not just about retiring early; it’s about designing a life that aligns with your values, passions, and aspirations.

Simple Steps to Financial Independence: Grow, Invest, Repeat

Grow the Gap: Increasing Financial Breathing Room

The first step on the journey to financial independence is to “grow the gap” between what you earn and what you spend. Whether by increasing income, reducing expenses, or both, this step lays the groundwork for financial success. Aiming to save and invest at least 20% of your income is a practical guideline to achieve long-term financial stability.

The 20% Rule: A Blueprint for Financial Wellness

Saving and investing 20% of your income, encompassing debt payments, retirement savings, and other investments, is a powerful strategy. Incremental increases in your savings rate over time compound into substantial financial growth. Remember, financial independence is a lifelong practice—consistent effort leads to lasting results.

Harnessing Fear for Financial Wisdom

Embracing Fear as a Catalyst

Fear is an inevitable companion in life’s journey, especially when it comes to financial uncertainties. However, rather than succumbing to fear, we can harness it as a catalyst for wise decision-making. Personal finance often becomes a source of comfort and security, offering a psychological buffer against life’s uncertainties.

Survive a Scary Economy: Lessons from History

Reflecting on history, we realize that the world has always been volatile. From pandemics to wars, the global landscape has witnessed myriad challenges. Embracing fear can motivate us to make prudent decisions, aligning our spending, time, and effort with our values. By doing so, we build intentional and resilient lives.

Building a Life of Intention

Connecting the Dots: First Principles, FI, and Intentional Living

Summarizing the journey, we connect the dots between first principles thinking, reframing FI, and intentional living. When financial decisions align with our values and life goals, we create a symphony of purposeful and joyful living. The philosophy that “You can afford anything” becomes a guiding principle for crafting a life rich in meaning and fulfillment.

Conclusion

In the grand theater of life, where choices abound, the essence lies in aligning decisions with our values. “You can afford anything, but not everything” encapsulates the profound truth that choices, when intentional, lead to a life well-lived. As we navigate the complexities of decision-making, let us embrace first principles, redefine financial independence, and foster intentional living. The path to a fulfilling life begins with the choices we make today.

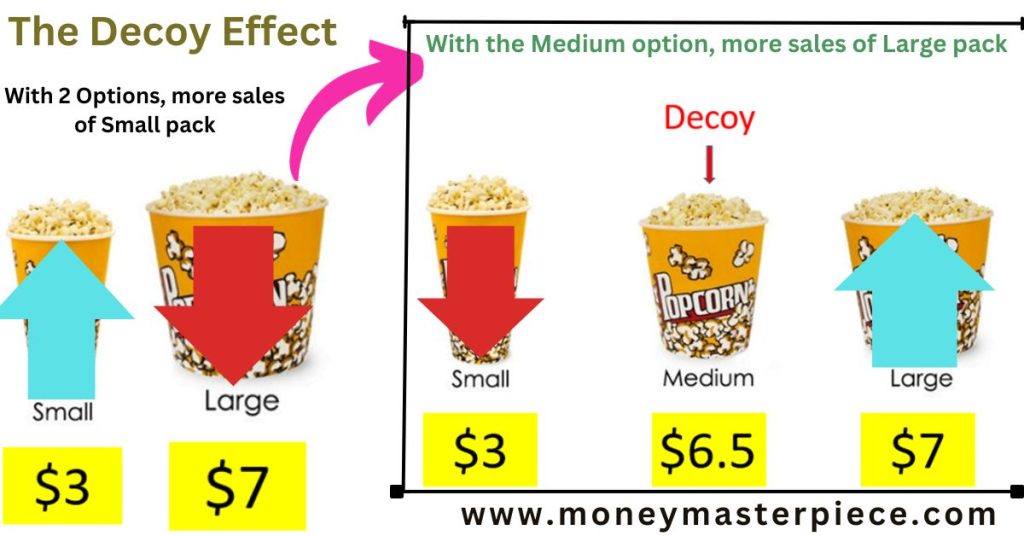

In the vast landscape of decision-making, our choices often play a pivotal role in shaping our financial future. One intriguing player in this arena is the Decoy Effect, a subtle yet powerful phenomenon that influences our perceptions and decisions. In this blog post, we will explore the intricacies of the Decoy Effect, examining why the introduction of a third, less attractive option can sway our choices and impact our personal finances.

Understanding the Decoy Effect:

The Decoy Effect occurs when adding a less attractive third option influences our perception of the original two choices. This asymmetrical dominance, where the decoy is inferior to one option (target) and partially inferior to the other (competitor), shapes decision-making dynamics.

Examples of the Decoy Effect: When you find the small at $3 and the large at $7, you usually end up in the small one. But if you see the small costs $3, the medium is $6.50, and the large is $7, you are likely to pick the large popcorn, as it’s a better deal than the medium.

How Does the Decoy Effect Work?

To illustrate the Decoy Effect in action, consider a scenario familiar to many – purchasing popcorn at a movie theater. You intend to buy a small bag, but when faced with options, the large popcorn seems like a better deal compared to the medium. The introduction of the medium popcorn as a decoy makes the larger size appear more appealing, leading you to make a choice that may not align with your initial preference.

The Naive Allocation of Resources: The Decoy Effect can cause us to allocate resources in a less optimal manner. When a decoy is present, decisions are often based on perceived advantages rather than a careful consideration of our needs. This bias can result in unnecessary spending and consumption, leading to financial implications in the long run.

Systemic Impact on Finances and Health: Businesses frequently employ decoys to nudge consumers into making choices that benefit the company. This practice can accumulate over time, impacting both our finances and health. Unhealthy food products, often pushed with decoys, contribute to overconsumption and potential health risks. Recognizing these systemic effects is crucial for making informed choices in a consumer-driven society.

The Decoy Effect in Digital Purchases: Beyond physical products, the Decoy Effect extends to digital purchases, such as app subscriptions or streaming services. The tiered pricing models, with options like basic, premium, and pro, can be influenced by the presence of a decoy. Consumers may be enticed to spend more on a higher-tier option due to the strategic placement of a slightly less attractive alternative.

Decoys and Artificial Intelligence: While AI software is not intentionally designed to manipulate consumers using the Decoy Effect, machine learning recommendations may inadvertently create scenarios of asymmetric dominance. Streaming services with AI-generated recommendations may influence user choices based on the perceived attractiveness of options.

Application in Personal Finance:

Pricing Strategies: The Decoy Effect is commonly employed by businesses in their pricing strategies. For instance, when choosing between two similar products, the introduction of a third, slightly less attractive option can sway consumers towards the more expensive but seemingly better value option.

Investment Choices: Investors may fall victim to the Decoy Effect when presented with investment options. A third investment choice, strategically placed to make one option appear more favorable, can influence decisions and lead to suboptimal portfolio selections.

Budgeting and Spending: The Decoy Effect can impact budgeting decisions by subtly encouraging spending on non-essential items. Retailers may introduce a slightly more expensive product as a decoy, making the original option appear more budget-friendly.

The Psychology Behind the Decoy Effect:

To comprehend the strength of the Decoy Effect, we delve into the concept of “asymmetric domination.” The target, competitor, and decoy form a triad, where the decoy is strategically designed to be inferior to both target and competitor in specific properties (A and B). This psychological phenomenon operates at a subconscious level, steering individuals towards choices without their full awareness.

Subconscious Influence and Behavioral Nudges: The Decoy Effect is a behavioral nudge, subtly steering individuals towards specific choices without imposing restrictions. This nudge capitalizes on the invisibility of its influence, as individuals often believe they are making independent choices. Research demonstrates that factors outside our awareness can significantly influence decision-making, creating a powerful tool for marketers and businesses.

Justification and Loss Aversion: Decoys provide a ready-made justification for our choices. When individuals make decisions, their goal is to justify the outcome rather than necessarily pick the correct option. The Decoy Effect strengthens this tendency, offering a rationale for choosing the target option and reinforcing a sense of comfort in the decision-making process.

Simplifying Choices and Overcoming Choice Overload: Decoys simplify decision-making by alleviating the anxiety associated with choice overload. The paradox of choice suggests that a broad selection can make decisions more challenging. Decoys manipulate factors of interest, directing attention to specific features and guiding individuals towards a more streamlined decision-making process.

Capitalizing on Loss Aversion: Loss aversion, the tendency to dislike losing more than enjoying gains, plays a crucial role in the Decoy Effect. Decoys manipulate the reference point, focusing on the disadvantages of the competitor option and emphasizing the perceived disadvantages. This psychological strategy increases the likelihood of individuals choosing the target option.

How to Avoid the Decoy Effect?

To illustrate the real-world impact of the Decoy Effect, consider the subscription options for The Economist in a classic experiment by psychologist Dan Ariely. The addition of a decoy drastically shifted preferences, leading individuals to make choices that were not in their best interest. Awareness alone may not be sufficient to avoid the Decoy Effect, but adopting strategies such as clarifying preferences, buying only what is needed, and being cautious of sets of three can offer protection.

As we navigate the complex landscape of personal finance, it becomes imperative to safeguard ourselves against the subtle influence of decoys. Here are actionable steps to avoid falling victim to the Decoy Effect:

Define Your Preferences Ahead of Time: Take a proactive approach by clearly defining your preferences before facing a decision. Whether you’re purchasing a product, choosing a service, or making an investment, identify the key factors that matter to you. By understanding your priorities, you can resist the subtle nudges of decoys that may try to sway you towards a less optimal choice.

Buy Only What You Truly Need: The Decoy Effect doesn’t always lead to bad decisions; sometimes, opting for a larger or higher-quality product can be justified. However, it’s crucial to evaluate whether the additional expense aligns with your needs. Before making a purchase, ask yourself if the more expensive option genuinely satisfies your requirements better than a more cost-effective alternative.

Beware of Sets of Three: The Decoy Effect is most potent when there are three options in play – target, competitor, and decoy. Whether you’re shopping, comparing products, or even considering political candidates, be attentive to situations where choices are presented in groups of three. This awareness can serve as an early warning sign of potential decoy manipulation.

Don’t Rely Solely on Intuition: Individual thinking styles play a role in susceptibility to the Decoy Effect. If you tend to rely on intuitive reasoning, you might be more prone to the influence of decoys. While intuition is valuable, it’s essential to balance it with rational thinking. Question your decision-making process and consider employing strategies that align with a more thoughtful approach.

Consult with Financial Advisors: Seeking advice from financial professionals can provide valuable insights and help you navigate through choices without succumbing to the Decoy Effect. They can offer a neutral perspective and guide you towards decisions aligned with your financial goals.

Understanding the historical context of the Decoy Effect adds another layer to its significance. Coined by Joel Huber, John Payne, and Chris Puto, the concept challenged existing models of decision-making, demonstrating that the introduction of a third, seemingly inferior option could be significant. Find more on the spillover effects.

Examples Beyond Consumer Choices:

The Decoy Effect extends beyond consumer choices and can influence various aspects of life. In the realm of dating apps, the presence of a slightly less attractive decoy can affect our preferences. Moreover, in political races, the Decoy Effect may have played a role, as seen in the 2000 US presidential election.

Examples of the Decoy Effect in Different Arenas:

Dating Apps: In the realm of online dating, the Decoy Effect can shape our preferences. Research, including studies by Dan Ariely, suggests that individuals may show increased interest in someone when presented alongside a similar-looking but slightly less attractive decoy. The presence of this decoy can alter our perceptions and influence our choices in the dating landscape.

Political Races: The Decoy Effect’s impact on political races is intriguing. Contrary to the common belief that a third-party candidate may split votes evenly, psychologists argue that the Decoy Effect could have played a significant role in the 2000 US presidential election. The presence of a third-party candidate may have influenced voters to shift towards a candidate more closely resembling the decoy.

Why is the Decoy Effect Important?

The Decoy Effect holds significant importance in various aspects of decision-making, consumer behavior, and strategic marketing. Here are several reasons why the Decoy Effect is considered crucial:

Influence on Consumer Choices: The Decoy Effect plays a pivotal role in shaping consumer decisions. By strategically introducing a less attractive option (the decoy) alongside two alternatives, businesses can influence customers to choose a specific product or service. This can lead to increased sales and revenue for companies.

Understanding Behavioral Nudges: The Decoy Effect is a prime example of a behavioral nudge – a subtle intervention that guides individuals toward a particular choice without imposing restrictions. Understanding how nudges operate, especially in the context of the Decoy Effect, provides insights into the psychological mechanisms that influence decision-making.

Impact on Pricing Strategies: Businesses often use the Decoy Effect to influence pricing perceptions. By presenting three options with a strategically positioned decoy, companies can drive consumers toward a target option, making it seem more attractive in terms of value for money. This tactic is commonly employed in industries ranging from entertainment to subscription services.

Systemic Effects on Spending Habits: The Decoy Effect contributes to systemic effects on spending habits, leading individuals to make choices that may not align with their actual preferences or needs. Over time, this can result in cumulative financial implications, impacting both personal budgets and societal spending patterns.

Application in Various Industries: The Decoy Effect is versatile and applicable across diverse industries. From consumer goods to digital services and even political campaigns, the concept can be leveraged to sway opinions and preferences. Recognizing its influence is crucial for both consumers and businesses seeking to make informed decisions.

Insights into Human Decision-Making Biases: The Decoy Effect provides valuable insights into the biases inherent in human decision-making processes. It sheds light on how individuals may be swayed by seemingly irrelevant options and factors, showcasing the complexity of choices and the role of cognitive biases in shaping preferences.

Strategic Marketing Tool: Marketers and advertisers can harness the power of the Decoy Effect as a strategic tool. Understanding how to position products or services with decoys allows businesses to create compelling offerings, influence customer perceptions, and ultimately drive desired outcomes in the market.

Research in Behavioral Economics: The Decoy Effect has become a focal point in behavioral economics research. Studying its mechanisms contributes to a deeper understanding of how individuals make decisions and the factors that influence their choices. This research has broader implications for economic theories and models.

Awareness for Consumers: For consumers, awareness of the Decoy Effect is empowering. Recognizing when decoys are being used in decision-making scenarios enables individuals to make more deliberate and informed choices. It encourages a critical evaluation of options, reducing the likelihood of being swayed by manipulative tactics.

Ethical Considerations: The ethical considerations surrounding the use of the Decoy Effect highlight the need for transparency in marketing and decision-making processes. As consumers become more informed, there is an increasing demand for ethical business practices, prompting companies to consider the long-term impact on customer trust and brand reputation.

In summary, the Decoy Effect is important because it provides valuable insights into the intricacies of decision-making, influences consumer behavior, and serves as a strategic tool in various industries. Understanding and navigating the implications of the Decoy Effect contribute to more informed choices and ethical business practices.

Conclusion:

In the intricate dance of decision-making, the Decoy Effect emerges as a formidable force that shapes our choices and, consequently, our financial outcomes. Recognizing the subtle influence of decoys, understanding the psychology behind it, and adopting strategies to avoid falling into the trap are crucial steps towards making informed and rational decisions in a world filled with options and influences.

Decoys, whether in the form of pricing strategies, product offerings, or digital subscriptions, are pervasive in our daily lives. From the movie theater popcorn scenario to the choices we make on dating apps or at the ballot box, the Decoy Effect is a silent persuader that nudges us toward specific decisions.

The marriage market functions as a public platform where parents advertise their children to find them a suitable spouse, and individuals gather to explore potential matches. This market operates similarly to a labor market, as both involve assortative matching and impact income inequality.

Additionally, marriage brings economic benefits such as tax breaks, social security benefits, access to credit, and shared expenses. Economists view the marriage market as a means for individuals to make choices regarding human capital investment and the allocation of marital surplus.

The analysis of marriage markets relies on the understanding that marriage generates a surplus, leading to the determination of intrahousehold resource allocation. Understanding the economics of the marriage market is crucial in comprehending the broader dynamics of family and relationships.

Understanding The Marriage Market

Understanding the marriage market involves analyzing the economics behind it. Similar to a labor market, positive assortative matching and the impact of education on income inequality play a significant role. Additionally, there are financial benefits to marriage such as tax breaks, social security benefits, and shared costs.

The marriage market applies economic theory to the process of matching individuals and how it influences other choices.

Definition And Purpose Of A Marriage Market

A marriage market can be defined as a public place where parents list advertisements for their children in the hopes of finding a suitable marital partner for them. It is a space where individuals gather to read these listings, with the intention of finding a compatible match for themselves or their loved ones. The purpose of a marriage market is to facilitate the process of finding a spouse and establishing a lifelong partnership. Similar to other markets, the marriage market operates on the principles of supply and demand, where individuals seek to find the best possible match based on various factors such as compatibility, social status, and personal preferences.

Similarities Between The Marriage Market And Labor Market

Just like the labor market, the marriage market exhibits certain similarities when it comes to the dynamics and mechanisms at play. One key similarity is the concept of positive assortative matching, which refers to the tendency for individuals to seek partners who are similar to them in terms of education, socioeconomic background, and other relevant characteristics.

The impact of positive assortative matching in both markets is significant. In the labor market, it can reinforce patterns of income inequality, with individuals having higher education levels and skills finding themselves matched with higher-paying jobs, while those with lower education levels may be matched with lower-paying jobs.

Similarly, in the marriage market, positive assortative matching can also contribute to issues of inequality. When individuals with similar levels of education and socioeconomic status pair up, it can reinforce income inequality both within households and between households. This can lead to a perpetuation of advantages or disadvantages based on factors like education and social capital.

Understanding these similarities between the marriage market and labor market sheds light on the importance of examining the economic implications of partner matching and its role in shaping inequality within societies.

Credit: www.stlouisfed.org

The Economic Benefits Of Marriage

The marriage market operates similarly to the labor market, with positive assortative matching contributing to income inequality. The economic benefits of marriage include tax breaks, social security benefits, access to credit, insurance savings, and shared costs. The marriage market applies economic theory to analyze the process of matching individuals and its influence on other choices and investments.

Tax Breaks And Financial Advantages Of Being Married

Marriage not only brings emotional fulfillment and companionship, but it also comes with several economic benefits. One of the significant financial advantages of being married is the access to tax breaks and financial incentives. Couples who are married enjoy certain tax benefits that are not available to single individuals. For example, in the United States, married couples may choose to file their taxes jointly, which often results in lower tax rates and the ability to claim various deductions and credits. These tax breaks can lead to significant savings and provide married couples with more disposable income.

Social Security Benefits And Insurance Savings

Another economic benefit of marriage is the access to Social Security benefits and insurance savings. Married individuals may be eligible to receive spousal benefits from Social Security, which can provide additional income during retirement. Additionally, being married often allows couples to combine their health insurance coverage, resulting in potential cost savings. With joint insurance policies, couples can enjoy reduced premiums and share medical expenses, making healthcare more affordable for both partners.

Access To Shared Benefits And Resources

A key advantage of marriage is the access to shared benefits and resources. When two people get married, they often merge their financial assets and resources. This pooling of resources can lead to increased financial security and stability. Married couples can share expenses such as housing, utilities, and transportation, reducing the financial burden on each individual. Furthermore, being married can make it easier to access certain benefits and resources that may not be available to single individuals, such as joint bank accounts, mortgage loans, and other financial services.

Retirement Account Contributions And Cost-sharing

Marriage also facilitates retirement account contributions and cost-sharing. When both partners are working, they have the opportunity to contribute to retirement accounts such as 401(k)s or IRAs. This enables them to save for retirement more effectively, as they can take advantage of higher contribution limits and potential employer matching contributions. Additionally, being married allows couples to divide the cost of living expenses and financial obligations. Sharing the financial burden can help to alleviate individual financial stress and may lead to greater financial well-being for both partners.

Socioeconomic Patterns Of Marriage And Divorce

The institution of marriage is not only a personal relationship but also influenced by various socioeconomic factors. Understanding the influence of the economy on marriage rates and the effect of economic factors on divorce rates can provide valuable insights into the dynamics of the marriage market.

The Influence Of The Economy On Marriage Rates

The state of the economy plays a significant role in determining marriage rates. During periods of economic growth and stability, individuals are more likely to get married. A thriving economy provides job security, higher incomes, and increased opportunities for individuals to establish a stable foundation for a marriage. On the other hand, economic downturns and recessions often lead to a decline in marriage rates as individuals may delay getting married due to financial uncertainties. This is particularly evident in countries experiencing economic crises or high unemployment rates.

How Economic Factors Affect Divorce Rates

Economic factors also have a notable impact on divorce rates. Financial instability and stress can strain a marriage, increasing the likelihood of divorce. For example, research has shown a positive correlation between unemployment rates and divorce rates. When individuals face job loss or financial hardships, it can lead to marital conflicts and ultimately, divorce. Additionally, couples with economic inequalities or disparities in earning potential often experience tensions that can contribute to marital dissatisfaction and breakups.

Income Inequality And Its Impact On Marital Choices

Income inequality is another socioeconomic factor that influences marital choices. People tend to seek partners with similar socioeconomic backgrounds and financial resources. In societies with high income inequality, individuals may face difficulties finding suitable matches, leading to delayed or fewer marriages. Additionally, income inequality can impact marriage stability, with higher levels of inequality associated with higher divorce rates. Couples facing financial disparities may face challenges in balancing power dynamics and maintaining harmonious relationships.

Overall, understanding the socioeconomic patterns of marriage and divorce provides valuable insights into how economic factors influence the dynamics of the marriage market. Economic conditions shape marriage rates, while financial stability, income inequality, and other economic factors affect the likelihood of divorce. By analyzing these patterns, policymakers and individuals can gain a better understanding of the intricate relationship between economics and marriage choices.

Analyzing The Marriage Market Through Economic Theory

Analyzing the marriage market through economic theory unveils the intricacies of how men and women are matched through marriage, impacting choices and allocation of resources. The application of economic theory to marriage reveals the similarities between labor and marriage markets, influencing income inequality and other socioeconomic patterns.

Application Of Economic Theory To The Marriage Market Analysis

When analyzing the marriage market through economic theory, we can gain valuable insights into the dynamics and behavior of individuals in this unique market. Economic theory provides a framework for understanding how individuals make decisions regarding marriage, and how these decisions can be influenced by factors such as supply and demand, preferences, and constraints.

By applying economic principles to the marriage market analysis, we can better understand the factors that affect the matching process between men and women and the outcomes that result from these matches.

How The Marriage Market Affects Human Capital Investment

The marriage market has a profound impact on human capital investment decisions. Human capital refers to the knowledge, skills, and abilities that individuals accumulate through education, training, and experience.

In the context of the marriage market, individuals often make decisions about their human capital investment based on the potential returns they can expect in the marriage market. For example, individuals may choose to invest in higher education or vocational training to increase their chances of attracting a more desirable marital partner.

Furthermore, individuals may also consider the potential impact of their human capital investment on their marital prospects. They may choose to pursue careers or occupations that are viewed as desirable in the marriage market, as this can increase their chances of finding a compatible partner.

Allocation Of Marital Surplus And Choices Of Individuals, Ensuring Each

The concept of marital surplus refers to the benefits that individuals derive from being in a marriage. This surplus can be thought of as the difference between the utility individuals experience in marriage compared to being single.

In the marriage market, individuals make choices that align with their preferences and maximize their own marital surplus. These choices can include decisions about whether to enter into a marriage, whom to marry, and how to allocate resources within the marriage.

For example, individuals may consider factors such as compatibility, financial stability, and personal values when selecting a partner, as these can impact the allocation of resources and the overall marital surplus. Additionally, individuals may also make choices about how to allocate their time and effort within the marriage to maintain and enhance the marital surplus.

Frequently Asked Questions

How Does The Marriage Market Work?

A marriage market is a public place where parents advertise their children to find a marital spouse. People gather there to read the listings and hope to find a match. It is similar to a labor market, where partners with similar educational backgrounds are matched.

Marriage also has economic benefits such as tax breaks and shared costs. The marriage market applies economic theory to analyze how men and women are matched through marriage.

How Is The Economy Affecting Marriages?

The economy is impacting marriages by causing financial stress and strain. Couples may face job loss, decreased income, and increased financial responsibilities, leading to conflicts and strains on the relationship.

How Is A Marriage Market Similar To A Labor Market?

A marriage market is similar to a labor market because both involve assortative matching and have implications for inequality. In the marriage market, partners with similar education are often matched, affecting income inequality. Similarly, in the labor market, individuals with similar skills and qualifications are matched, impacting income distribution.

What Are The Economic Benefits Of Marriage?

Marriage offers several economic benefits. Couples enjoy tax breaks, social security benefits, insurance savings, and easier access to credit. They can also contribute to individual retirement accounts and share costs, resulting in financial stability and savings.

Conclusion

To understand the workings of the marriage market, we must recognize its similarity to the labor market. Positive assortative matching, where partners with similar education levels are paired, has a significant impact on income inequality. Moreover, marriage offers economic benefits such as tax breaks, social security benefits, and insurance savings.

However, it’s important to note that each situation is unique, and financial advantages are just one aspect of marriage. By applying economic theory to the analysis of marriage, we gain insights into how individuals are matched and how this process influences other choices.