Success Fee: The Key to Motivating and Rewarding Success

In today’s competitive business environment, motivating employees and rewarding their success is vital to maintaining high levels of productivity and achieving company goals. One effective way to drive performance and recognize achievements is through the implementation of a success fee program.

What is a Success Fee?

A success fee is a performance-based compensation system that rewards employees or teams for achieving specific targets or milestones. It acts as an additional incentive on top of the regular salary and benefits package, motivating individuals to go above and beyond their regular duties and perform at their best.

The success fee can be tied to various measurable outcomes, such as meeting sales targets, increasing customer satisfaction, completing projects ahead of schedule, or even reducing operational costs. It provides a clear link between performance and rewards, creating a win-win situation for both the employees and the company.

Benefits of Implementing a Success Fee Program

Implementing a success fee program offers numerous benefits that can significantly impact an organization’s overall success:

Motivation: Success fees provide employees with a tangible reward for their efforts, boosting motivation and commitment to achieving targets.

Improved Performance: When employees have a clear incentive to perform at their best, they are more likely to go the extra mile and exceed expectations, leading to improved overall performance.

Goal Alignment: Success fees can be directly linked to specific goals and objectives, ensuring that employees’ efforts are aligned with the company’s strategic direction.

Increased Productivity: With the promise of a success fee, employees are motivated to work more efficiently and effectively, ultimately increasing productivity levels.

Retention and Loyalty: Offering a success fee not only motivates employees to stay and perform well but also fosters loyalty towards the organization.

Competitive Advantage: A well-designed success fee program can attract top talent, giving the company a competitive edge in the job market.

Implementing a Successful Success Fee Program

While implementing a success fee program can be highly effective, it requires careful planning and consideration. Here are some key steps to ensure its successful implementation:

1. Set Clear And Achievable Goals

Identify specific and measurable goals that align with the company’s overall objectives. These goals should be challenging but attainable, providing employees with a sense of accomplishment when they achieve them.

Goal Areas

Examples

Sales

Achieving monthly revenue targets

Customer Service

Improving customer satisfaction ratings

Operations

Reducing production costs by 10%

2. Determine The Success Fee Structure

Decide on the structure of the success fee program, such as the percentage of the bonus or the formula used to calculate it. Ensure that the structure provides an appropriate balance between motivation and financial feasibility for the company.

3. Communicate The Program Clearly

Ensure that employees fully understand the success fee program, its goals, and the criteria for earning the bonus. Transparent communication will prevent confusion and set realistic expectations.

4. Track And Measure Progress

Regularly monitor and evaluate employees’ progress towards the defined goals. Tracking their performance not only keeps them engaged but also allows for timely recognition and rewards.

5. Celebrate And Recognize Success

When employees achieve their targets and milestones, acknowledge their success publicly. Celebrate their accomplishments and reward them promptly to reinforce the positive behavior and motivate others.

In Conclusion

A success fee program can be a powerful tool for motivating and rewarding success within an organization. By providing employees with a direct link between their performance and financial rewards, companies can drive performance, improve productivity, and foster employee loyalty.

When implementing a success fee program, it is essential to set clear goals, define appropriate structures, communicate transparently, and consistently track employees’ progress. With careful planning and implementation, success fees can become a key driver of success and a win-win strategy for both employees and the company.

Frequently Asked Questions For Success Fee

How Does A Success Fee Work?

A success fee is a payment made based on the successful outcome of a specific event or goal. It is typically a percentage of the total value of the achievement.

What Are The Advantages Of A Success Fee?

A success fee provides an incentive for achieving desired results. It aligns interests between parties and allows for shared risk and reward based on performance.

Are Success Fees Common In Business Transactions?

Yes, success fees are commonly used in various industries such as mergers and acquisitions, sales and marketing, and legal and financial consulting. They motivate parties to work towards achieving specific objectives.

How Can A Success Fee Improve Business Outcomes?

By linking payment to successful results, a success fee can enhance motivation and performance. It encourages individuals or teams to strive for excellence and ensures that effort and resources are directed towards achieving specific goals.

Cash back debit cards work by offering a percentage of your purchases back to you as a reward. This means that every time you make a purchase with the card, you’ll receive a small percentage of the amount spent credited back to your account.

Cash back debit cards are a popular choice for those who want to earn rewards on everyday purchases without accruing credit card debt. They work similarly to cash back credit cards, but instead of earning rewards in the form of points or miles, you receive cash back directly into your bank account.

This can be a great way to save money on your regular spending and maximize your budget. We’ll delve deeper into the workings of cash back debit cards and the benefits they offer to consumers.

What Are Cash Back Debit Cards?

What are Cash Back Debit Cards?

Cash back debit cards are a type of debit card that rewards users with cash back for making purchases, similar to credit card rewards. When you make a purchase with a cash back debit card, you can earn a percentage of the amount spent back as cash rewards, which are typically deposited into your bank account.

How Do Cash Back Debit Cards Differ From Regular Debit Cards?

Unlike regular debit cards that do not offer any rewards, cash back debit cards provide a way for users to earn money back on their spending. With a regular debit card, the transactions are solely for purchases, whereas with a cash back debit card, users can earn a percentage of the amount spent as cash rewards.

Benefits Of Using Cash Back Debit Cards

1. Earn Rewards: Cash back debit cards allow users to earn cash rewards on everyday purchases, providing an incentive for using the card for transactions.

2. Savings: By earning cash back on purchases, users can save money and maximize their spending.

3. No Debt: Since cash back debit cards are linked to a user’s bank account, there is no risk of racking up credit card debt.

4. Financial Control: Using a cash back debit card encourages responsible budgeting and spending habits, as users can earn rewards without the risk of accruing interest or fees.

How Cash Back Debit Cards Work

Cash back debit cards offer a convenient way to earn rewards while making everyday purchases. If you’re not familiar with how they work, let’s break it down for you. With a cash back debit card, you can earn a percentage back on your transactions, which can add up to significant savings over time. In this article, we’ll delve into the details of how you can earn and redeem these cash back rewards.

Earning Cash Back Rewards

When it comes to earning cash back rewards with a debit card, the process is simple. For every eligible purchase you make using your cash back debit card, you’ll earn a certain percentage of cash back. The exact percentage may vary depending on the card issuer and the type of transaction. Typically, rewards ranging from 1% to 5% are common in the industry.

To earn cash back rewards, all you need to do is use your debit card as you would for any regular purchase. Whether it’s buying groceries, filling up your gas tank, or even paying bills, every eligible transaction has the potential to earn you cash back. Remember to keep an eye out for any specific promotions or limited-time offers that may boost your earnings even further.

Redeeming Cash Back Rewards

Now that you’ve accumulated some cash back rewards, it’s time to put them to use. Redeeming your cash back rewards with a cash back debit card is typically a straightforward process. Many card issuers offer various options to redeem your rewards, such as applying them as statement credits, depositing them into your bank account, or even using them to offset future purchases.

To redeem your cash back rewards, simply follow the instructions provided by your card issuer. This may involve logging into your online banking account or contacting customer support. Once you’ve selected your preferred redemption method, your cash back rewards will be applied accordingly. It’s important to note that different cards may have specific redemption thresholds or expiration dates, so it’s essential to familiarize yourself with the terms and conditions.

Factors To Consider Before Choosing A Cash Back Debit Card

A cash back debit card can be an excellent way to earn rewards on your everyday spending, but there are several factors to consider before choosing the right one for you. From the cash back percentage to additional fees and requirements, understanding these factors can help you make an informed decision and maximize your rewards.

Cash Back Percentage And Categories

Before choosing a cash back debit card, it’s essential to consider the cash back percentage offered by the card. Some cards offer a flat cash back rate on all purchases, while others may have different cash back percentages based on spending categories. Understanding the cash back categories can help you determine if the card aligns with your spending habits and allows you to earn rewards on the purchases you make most frequently.

Additional Fees And Requirements

When selecting a cash back debit card, be sure to review any additional fees and requirements associated with the card. This may include monthly maintenance fees, minimum balance requirements, or specific qualifying criteria for earning cash back. Evaluating these factors can help you determine if the potential cash back rewards outweigh any additional costs or restrictions associated with the card.

Maximizing Cash Back Rewards

When it comes to maximizing cash back rewards with debit cards, there are several strategies and responsible usage tips that can help you make the most of this convenient financial tool.

Strategies For Maximizing Cash Back

Maximizing your cash back rewards with a debit card can be accomplished by understanding the specific rewards structure provided by your card issuer. Some common strategies include:

Earning higher rewards by using your debit card for everyday spending such as groceries, gas, and bills.

Taking advantage of special offers and promotions to earn additional cash back on specific purchases.

Using your debit card for online purchases through affiliated retailers to earn extra cash back rewards.

Optimizing cash back categories by leveraging multiple debit cards with complementary rewards programs.

Using Cash Back Debit Cards Responsibly

To use cash back debit cards responsibly and maximize your rewards, it’s important to:

Regularly review your debit card account to ensure your purchases align with your budget and financial goals.

Avoid unnecessary fees and charges by understanding your bank’s policies including applicable transaction fees and minimum balance requirements.

Refrain from overspending in pursuit of rewards, as interest charges on carried balances can outweigh the benefits of cash back.

Consider combining your cash back rewards with other financial goals, such as saving or debt repayment.

Frequently Asked Questions For How Cash Back Debit Cards Work

What Are The Disadvantages Of A Cash Back Card?

Cash back cards may come with high interest rates, annual fees, and spending limits. Additionally, rewards may fluctuate based on categories. Limited redemption options and potential overspending are also drawbacks.

Are Cashback Debit Cards Worth It?

Yes, cashback debit cards are worth it as they offer cash rewards for purchases. They can help you save money on everyday spending. Use them wisely to maximize benefits.

How Do Cashback Cards Work?

Cashback cards offer a percentage of the amount spent back to the cardholder. When you make a purchase, you receive a cash reward. This can be in the form of statement credit, direct deposit, or a check. The more you spend, the more cashback you can earn.

Conclusion

Cash back debit cards offer a simple and effective way to earn rewards on everyday spending. By choosing a debit card that offers cash back incentives, you can make the most of your money. With careful management, these cards can provide a significant benefit to your finances.

Explore your options and enjoy the benefits of cash back rewards.

In the world of finance and investment, there are various types of fraudulent schemes that people must be aware of. Two such schemes that often get confused are Ponzi schemes and pyramid schemes. While they share some similarities, they are fundamentally different in nature. In this article, we will explore the differences between Ponzi and pyramid schemes.

Credit: www.dehek.com

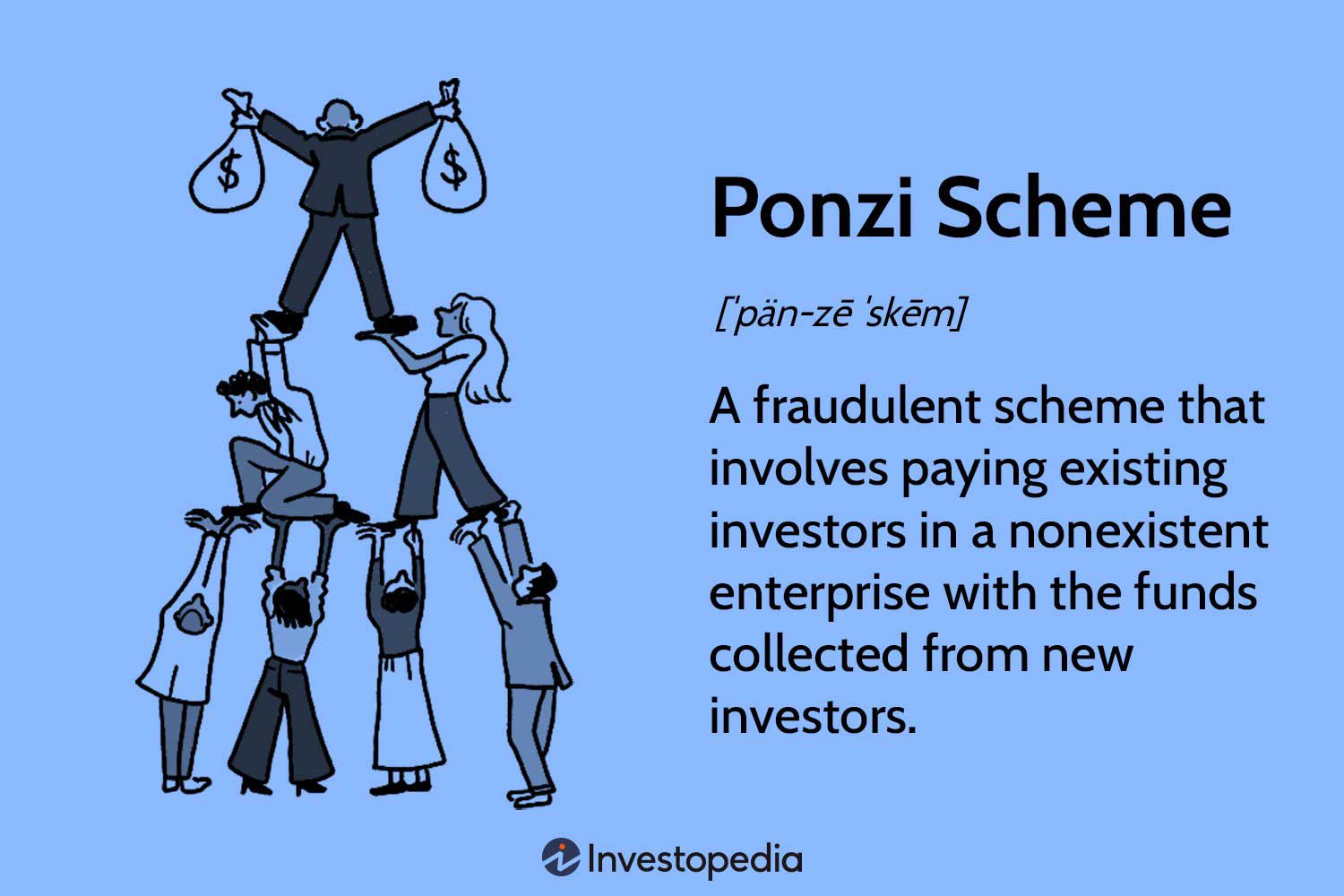

What Is a Ponzi Scheme?

A Ponzi scheme is a fraudulent investment operation where the operator, typically an individual or a company, promises high returns to attract investors. The operator pays returns to earlier investors using funds collected from new investors, rather than from legitimate profits. This creates a false impression of a profitable investment, encouraging more investors to join.

The key characteristic of a Ponzi scheme is that it relies on a constant stream of new investors to sustain itself. Eventually, the scheme collapses when it becomes impossible to recruit new members or when a large number of investors demand their money back at once.

Characteristics of Ponzi Schemes:

Offers unrealistically high returns on investment

Relies on a continuous influx of new investors

Uses funds from new investors to pay previous investors

Operates without a legitimate underlying business

Usually run by a single individual or a small group

What Is a Pyramid Scheme?

A pyramid scheme is a fraudulent business model that recruits members via a promise of payments or services for enrolling others into the scheme, rather than supplying investments or selling legitimate products or services. Members are expected to recruit new members and pay an entry fee, which is then distributed among the higher-ranking participants.

The hallmark of a pyramid scheme is the emphasis on recruitment. Its focus is primarily on bringing in new participants to keep the pyramid growing. As the number of members increases, the need for new recruits becomes unsustainable, leading to the collapse of the scheme.

Characteristics of Pyramid Schemes:

Emphasizes recruitment of new members

Participants pay an entry fee or purchase a product

Money flows up the pyramid to higher-ranking members

Little to no emphasis on selling legitimate products or services

Requires constant recruitment to sustain the scheme

Credit: fastercapital.com

The Key Differences

Although both Ponzi schemes and pyramid schemes are forms of financial fraud, they differ in several crucial aspects:

Ponzi Schemes

Pyramid Schemes

Operated by an individual or small group

Can involve multiple levels of participants

Investors are promised high returns

Members earn money by recruiting others

Money is taken by a single operator

Money flows up the pyramid structure

Relies on a constant influx of new investors

Requires constant recruitment to sustain the scheme

Legal Considerations

Both Ponzi and pyramid schemes are illegal in most countries. Law enforcement authorities actively work to dismantle such fraudulent operations and penalize the individuals involved. It’s important for potential investors and individuals to stay informed and educated about such schemes to protect themselves from becoming victims.

Conclusion

Ponzi schemes and pyramid schemes may appear similar on the surface, but they have distinct differences in their operation and structure. While Ponzi schemes rely on promising high returns to attract investors, pyramid schemes depend on recruiting new members to sustain the scheme. Understanding these differences is crucial for safeguarding yourself against financial fraud.

Delinquency refers to late or missed payments, while default occurs when a borrower fails to repay a loan as agreed. Missed or late payments are considered delinquency, while default happens when a borrower fails to repay their loan as agreed.

Delinquency is generally the initial stage of non-payment, while default is a more severe consequence that can result in serious consequences. Despite being related, delinquency and default are distinct terms in the financial industry. Understanding the differences between these two terms is essential for borrowers, lenders, and creditors alike.

It helps in evaluating the risk associated with lending money and managing the consequences of non-payment effectively. This article explores the variances between delinquency and default to provide readers a clear understanding of these crucial financial concepts.

Key Definitions

Differences Between Delinquency And Default

Delinquency refers to the failure of a borrower to make timely payments on a loan or debt. When a borrower becomes delinquent, they have failed to make a payment by the due date specified in the loan agreement.

Default, on the other hand, goes a step further than delinquency. It occurs when a borrower has failed to repay a loan or debt and has not made any payments for an extended period of time, typically defined by the specific loan agreement. A default is considered a more severe situation than delinquency and is often the result of prolonged non-payment.

Here’s a handy table that summarizes the key differences between delinquency and default:

Delinquency

Default

A borrower has missed a single payment.

A borrower has not made any payments for an extended period of time.

Failure to make timely payments.

Complete failure to repay a loan or debt.

Considered less severe than default.

Considered a more severe situation.

It’s important to note that delinquency and default can have serious consequences for borrowers. These can include damage to credit scores, higher interest rates on future loans, and even legal action taken by lenders to recover the debt.

In summary, while both delinquency and default involve a borrower’s failure to repay a loan or debt, they differ in terms of the duration and severity of non-payment. Delinquency refers to the failure to make timely payments, often marked by missing a single payment. Default, on the other hand, is a more severe situation where a borrower has not made any payments for an extended period of time.

Causes

Understanding the causes behind delinquency and default can shed light on the reasons why individuals or companies fail to meet their financial obligations. Delinquency refers to the failure to make timely payments, while default occurs when a borrower fails to repay a loan according to the agreed-upon terms. Let’s take a closer look at the causes of delinquency and default.

Delinquency Causes

Delinquency can arise due to a variety of factors, often interrelated. Some common causes of delinquency include:

Financial hardship: Unexpected expenses, job loss, or medical emergencies can strain finances, making it difficult to meet payment deadlines.

Lack of financial education: Individuals who lack knowledge of managing finances may struggle to budget effectively, leading to delinquency.

Unemployment: Loss of income due to unemployment can severely impact a person’s ability to make regular payments.

Excessive debt: If an individual or company has too much debt compared to their income or revenue, it can become challenging to meet all their financial obligations promptly.

Personal circumstances: Life events such as divorce, death in the family, or unexpected legal issues can disrupt financial stability, contributing to delinquency.

Default Causes

Default can have significant consequences and is typically caused by factors such as:

Lack of collateral: In some cases, loans require collateral as security. If the borrower fails to provide appropriate collateral or it loses value, default can occur.

Insufficient funds: When borrowers lack the financial means to repay the loan, default is likely to happen.

Loan mismanagement: Poor financial planning, overspending, or reckless behavior can lead to default when the borrower cannot meet payment obligations.

Interest rate hikes: If interest rates significantly increase, borrowers may struggle to afford the higher loan repayments, resulting in default.

Business failure: For companies, a significant change in market conditions, poor management, or unforeseen circumstances can lead to default on business loans.

Impacts

Delinquency refers to late payments on a loan or bill, whereas default occurs when the borrower fails to repay the debt. Delinquency is a temporary setback, while default leads to serious consequences like damage to credit scores and legal action.

Understanding the distinctions between the two can help individuals manage their financial obligations effectively.

Impacts Of Delinquency

Delinquency refers to the failure to pay a financial obligation on time. This can happen for various reasons, such as forgetfulness, financial difficulties, or simply negligence. However, delinquency comes with several negative impacts that individuals should be aware of:

1. Financial Consequences: When you become delinquent on a payment, you may incur late fees and penalties. These additional charges can further add to your financial burden and make it even harder to catch up on your payments.

2. Damage to Credit Score: Delinquency can have a detrimental effect on your credit score. Late payments are typically reported to credit bureaus, and this can lead to a decrease in your score. A lower credit score can make it more challenging to obtain credit in the future, and if you do get approved, you may face higher interest rates.

3. Limited Financial Opportunities: Delinquency can also restrict your access to future financial opportunities. Lenders and creditors may view you as a higher risk borrower and may be hesitant to extend credit to you. This can make it difficult to secure loans, mortgages, and even rental agreements.

4. Stress and Anxiety: Dealing with delinquency can take a toll on your mental health. The stress and anxiety of falling behind on payments and facing potential consequences can be overwhelming. It is important to address delinquency promptly to alleviate this emotional burden.

Impacts Of Default

Default occurs when a borrower fails to repay a loan or fulfill a contractual obligation entirely. Unlike delinquency, default is a more severe stage that can have serious consequences, both financially and legally. Here are some impacts of default:

1. Legal Actions: One of the significant impacts of default is the potential for legal actions. Creditors have the right to take legal action to recover the amount owed. This can lead to court proceedings, judgments, and even the seizure of assets in some cases.

2. Damage to Credit History: Default has a severe impact on your credit history and credit score. The default, along with any associated legal actions, is typically reported to credit bureaus and remains on your credit report for a significant period. This can make it extremely challenging to obtain credit in the future.

3. Collection Efforts: Defaulting on a loan or obligation often results in aggressive collection efforts by creditors or debt collectors. These efforts can include constant phone calls, letters, and even harassment. It can be incredibly stressful to deal with these persistent and sometimes hostile interactions.

4. Limited Financial Options: Default can severely limit your financial options. It can be difficult to secure new loans or credit lines, and even if you manage to get approved, the terms are likely to be unfavorable, with high-interest rates and strict repayment conditions.

5. Impact on Future Opportunities: Default can have long-term implications on your financial future. It can hinder your ability to rent a home, obtain insurance, or even land a job. Many employers run credit checks as part of their hiring process, and default can make you appear unreliable and irresponsible.

Understanding the differences between delinquency and default is crucial for anyone managing their financial obligations. Delinquency can have negative consequences, but default takes it to a whole new level, with severe financial, legal, and personal impacts. It is essential to stay on top of your payments and address any delinquencies promptly to avoid falling into default.

Financial Industry Perspective

In the financial industry, understanding the differences between delinquency and default is crucial for effective account management. When borrowers fail to make their scheduled payments, it can disrupt the cash flow and create potential risks for lenders. By differentiating between delinquency and default, financial institutions can apply appropriate strategies to handle each situation. Let’s take a closer look at how delinquent and defaulted accounts are managed within the financial industry.

Handling Delinquent Accounts

Delinquency refers to the status of an account when a borrower has missed one or more payments. Companies strive to prevent delinquency from escalating into default, as early intervention can help resolve payment issues and maintain a positive borrower-lender relationship. Here are a few key steps taken in handling delinquent accounts:

1. Early Notification: Upon recognizing a delinquent account, lenders promptly notify borrowers regarding the missed payment(s) through various communication channels such as email, phone call, or mailed letter.

2. Grace Periods and Late Fees: Depending on the terms of the loan agreement, borrowers may be given a grace period to catch up on missed payments. Late fees may also be charged to incentivize timely repayment.

3. Collections and Payment Arrangements: If the delinquency persists, lenders may initiate collections efforts, working closely with borrowers to establish feasible payment arrangements. This collaborative approach aims to mitigate financial hardships and prevent accounts from entering default.

Managing Defaulted Accounts

Default occurs when a borrower fails to make payments within a specified timeframe, typically after several instances of delinquency. When accounts reach the default stage, financial institutions need to take more assertive measures to protect their interests. The following actions are commonly employed in managing defaulted accounts:

Legal Proceedings: Lenders may engage in legal proceedings, including filing a lawsuit or obtaining a judgment, to recover the outstanding debt. These actions are taken to protect the lender’s rights and enforce repayment.

Asset Seizure: In situations where the borrower’s collateral secures the loan, lenders may exercise their rights to seize and liquidate the assets to recover the outstanding debt.

Credit Reporting: Defaulted accounts are typically reported to credit bureaus, adversely affecting the borrower’s credit score and making it challenging for them to obtain credit in the future.

By understanding the differences between delinquency and default, financial institutions can handle accounts appropriately to minimize financial losses and maintain a healthy lending environment. Early detection and proactive measures in handling delinquent accounts can prevent them from escalating into default, benefiting borrowers and lenders alike.

Prevention And Resolution

Prevention and resolution are crucial aspects when it comes to managing delinquency and default. Proactive measures can help prevent delinquency, while effective strategies can help resolve default situations. Understanding these differences and implementing appropriate actions is essential for maintaining financial stability.

Preventing Delinquency

Preventing delinquency is vital to avoid default situations. Here are some effective strategies to prevent delinquency:

Timely Payments: Ensure timely payments of bills and loans to avoid falling into delinquency.

Budget Management: Proper budgeting can help individuals stay on top of their financial obligations, reducing the chances of delinquency.

Regular Communication: Open and regular communication with creditors can help in finding alternative solutions in case of financial difficulties.

Resolving Default

Resolving default is essential to mitigate the impact of financial challenges. Here are some effective strategies to address default situations:

Negotiation: Engage in negotiations with creditors to come up with a feasible repayment plan.

Seeking Assistance: Seeking professional assistance from financial advisors or credit counseling agencies can provide insights and strategies to resolve default.

Restructuring Debts: Consider debt restructuring options to make repayments more manageable and sustainable.

Frequently Asked Questions For What Are The Differences Between Delinquency And Default?

Is A Delinquent Account As Bad As A Default?

A delinquent account and a default are both negative for your credit score. A delinquent account refers to a late payment, while a default means you have failed to repay a loan or debt. Both can hurt your creditworthiness and make it difficult to get credit in the future.

What Causes Delinquency And Default?

Delinquency and default are often caused by financial hardship, lack of income, improper money management, and unexpected expenses. These factors can lead individuals to struggle with loan payments and eventually default on their obligations.

What Is The Difference Between Delinquent And Delinquency?

Delinquent refers to a person who fails to fulfill obligations, while delinquency is the state of being delinquent.

Conclusion

To summarize, the differences between delinquency and default are significant in the realm of financial obligations. While delinquency refers to a late or missed payment, default signifies a complete failure to meet financial obligations. Both situations have serious consequences, including negative impacts on credit scores and potential legal action.

Understanding these differences is crucial for individuals and organizations navigating the complex world of debt and financial management. Take the necessary steps to stay informed and proactively manage financial obligations to avoid the detrimental effects of both delinquency and default.

When wholesale funding goes bad, it can lead to financial instability and liquidity issues for financial institutions. Wholesale funding refers to the borrowing of funds from external sources, such as other financial institutions, rather than relying on customer deposits.

When this funding source turns sour, it can create a domino effect on the institution’s ability to meet its financial obligations and can even lead to a broader systemic crisis. Understanding the implications of wholesale funding and its potential risks is crucial for financial institutions and regulators to maintain stability in the financial system.

We will delve into the potential causes, effects, and preventive measures related to the impact of wholesale funding gone bad. By gaining a comprehensive understanding of this topic, stakeholders can be better equipped to mitigate the associated risks and ensure a resilient financial environment.

The Risks Of Wholesale Funding

Lack Of Stable Deposit Base

Wholesale funding institutions heavily rely on volatile short-term capital, which lacks the stability of a traditional deposit base, making them susceptible to sudden changes in investor sentiment and liquidity

Vulnerability To Market Conditions

Wholesale funding is highly exposed to market conditions, leaving institutions vulnerable to interest rate fluctuations, credit market instability, and economic downturns without the security of a diverse deposit base to mitigate risks.

The Impact On Financial Institutions

Increased Liquidity Risk

When wholesale funding goes bad, it significantly increases liquidity risk for financial institutions. Relying heavily on wholesale funding exposes these institutions to the vulnerability of a sudden and severe funding shortfall, making it difficult to meet short-term financial obligations.

Potential Solvency Issues

Financial institutions facing wholesale funding problems may also experience potential solvency issues. An imbalance between assets and liabilities can arise, leading to inadequate capital to cover losses and maintain operational stability.

Regulatory Measures To Address Wholesale Funding Risks

Regulatory measures play a crucial role in managing risks associated with wholesale funding. Implementing relevant regulations can help mitigate potential threats and safeguard the stability of financial institutions. Let’s delve into the key regulatory measures to address wholesale funding risks.

Capital Adequacy Requirements

Capital adequacy requirements are fundamental regulatory measures designed to ensure that financial institutions maintain sufficient capital to cover risks arising from their operations. These requirements are aimed at promoting the safety and soundness of banks by establishing guidelines for the amount of capital that must be held in relation to their assets. Complying with capital adequacy standards is essential for mitigating the potential impact of wholesale funding challenges.

Liquidity Coverage Ratio (lcr)

Another significant regulatory measure is the Liquidity Coverage Ratio (LCR), which focuses on assessing a bank’s ability to withstand short-term liquidity disruptions. The LCR sets out the minimum amount of high-quality liquid assets that banks must hold to meet potential liquidity needs during stressful situations. Complying with the LCR ensures that financial institutions are better prepared to manage liquidity risks associated with wholesale funding.

Mitigating Wholesale Funding Risks

Diversifying Funding Sources

“`

Wholesale funding can pose significant risks for financial institutions; therefore, it is crucial to mitigate these risks. Diversifying funding sources is one effective way to reduce reliance on a single source of wholesale funding. By diversifying funding sources, institutions can reduce the impact of potential funding disruptions from any one source.

“`html

Stress Testing And Scenario Analysis

“`

Conducting stress testing and scenario analysis is essential for evaluating the resilience of funding models. It helps institutions identify potential vulnerabilities and prepare appropriate mitigation strategies. This analysis allows for understanding the impact of various stressors on the wholesale funding structure, enabling institutions to proactively address any weaknesses.

By incorporating these strategies, institutions can bolster their resilience to wholesale funding risks and enhance their overall financial stability.

Frequently Asked Questions For When Wholesale Funding Goes Bad

How Does Wholesale Funding Work?

Wholesale funding involves obtaining funds from large financial institutions. Banks and other entities use this method to secure funds for lending and investment activities.

What Is Long Term Wholesale Funding?

Long term wholesale funding refers to acquiring funds from wholesale markets for a longer period. It helps institutions access a stable source of funding.

What Is Unsecured Wholesale Funding?

Unsecured wholesale funding is a type of financial support that doesn’t require collateral. It’s commonly used by businesses to obtain capital for their operations and growth. This funding can be quick and flexible, but typically comes with higher interest rates due to the lack of collateral.

Conclusion

It’s important for businesses to cautiously approach wholesale funding to mitigate the risks involved. Understanding the potential pitfalls and the impact on the financial stability of the organization is crucial. By implementing sound financial management practices, businesses can navigate through challenges and build long-term success.

Effective risk assessment and strategic decision-making are key in mitigating the negative impact of wholesale funding gone bad.

Chandelier Exit – A Must-Know Indicator for Traders

Welcome to our comprehensive guide on the Chandelier Exit indicator. If you’re an active trader, understanding and effectively utilizing various technical analysis indicators can significantly enhance your trading success. In this article, we will delve into what the Chandelier Exit indicator is, how it works, and how you can incorporate it into your trading strategy.

Credit: www.amazon.com

What is the Chandelier Exit Indicator?

The Chandelier Exit is a technical analysis indicator that helps traders identify potential price reversals in a trend-following market. Developed by Chuck LeBeau, the Chandelier Exit primarily serves as a stop-loss indicator, enabling traders to set trailing stops based on market volatility.

This indicator takes into account three essential components:

Recent high or low

Average True Range (ATR)

Chandelier Exit line

How Does the Chandelier Exit Work?

The Chandelier Exit is particularly useful in trending markets, where it helps traders stay in established trends while minimizing risk exposure. It calculates the stop-loss point by subtracting a multiple of the ATR from the highest high since the entry of the trade. The subsequent Chandelier Exit line is plotted above the price, indicating a potential exit or reversal point.

Traders often set their stop-loss levels below the Chandelier Exit line when going long or above it when going short. As the market continues to trend, the Chandelier Exit adjusts accordingly, providing traders with an indicator of when to exit or reverse their positions.

Credit: www.youtube.com

Incorporating the Chandelier Exit into Your Trading Strategy

The Chandelier Exit can be used as a standalone indicator or in combination with other technical analysis tools. Here are a few ways you can incorporate it into your trading strategy:

1. Trend Following

As mentioned earlier, the Chandelier Exit is excellent for trend-following trades. When the price is above the Chandelier Exit line, it indicates a bullish trend, and traders can look for buying opportunities. Conversely, when the price is below the Chandelier Exit line, it suggests a bearish trend, and traders can consider shorting the market.

2. Trade Management

Traders can use the Chandelier Exit to manage their trades effectively. By trailing the Chandelier Exit line, traders can lock in profits as the market moves in their favor. As the price continues to rise in an uptrend or fall in a downtrend, the Chandelier Exit provides updated stop-loss levels, protecting profits and minimizing potential losses.

3. Confirmation With Other Indicators

Combining the Chandelier Exit with other technical analysis indicators can strengthen trading signals. Traders often use indicators like moving averages, oscillators, or trendlines to confirm Chandelier Exit signals before entering or exiting trades.

Conclusion

The Chandelier Exit indicator is a powerful tool that helps traders manage risk and maximize profits by identifying potential trend reversals. Whether you’re a beginner or an experienced trader, incorporating the Chandelier Exit into your trading strategy can significantly improve your decision-making process.

Remember, it’s always essential to backtest indicators and practice proper risk management techniques to ensure optimal results. Start exploring the Chandelier Exit indicator today and unlock its potential in your trading journey!